½ Balboa – Panama

Circulating commemorative coins

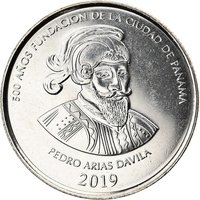

Commemoration: Monumental Historical Set of Panama Viejo.

Series: Panama Viejo

Panama

Context

Material

References

KM: #Click to copy to clipboard160

Numista: #127436

Value

Exchange value: ½ PAB

Obverse

Reverse

Edge

Reeded

Categories

| Symbols> Coat of Arms |

Mints

| Name | Mark |

|---|---|

| Royal Canadian Mint of Winnipeg | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2017 | — | 3,000,000 |

Historical background

Panama's currency situation in 2017 was defined by its unique and long-standing monetary framework, which remained a cornerstone of economic stability. Since 1904, the country has operated under a fully dollarized economy, using the US dollar as its official legal tender. This means the US dollar is used for all daily transactions, contracts, and financial accounts, while the Panamanian balboa exists only as coinage, pegged at a 1:1 ratio to the dollar. Consequently, Panama does not have a central bank to conduct independent monetary policy and cannot print its own paper currency, ceding control over interest rates and monetary supply to the United States Federal Reserve.

The primary benefit of this system, evident in 2017, was macroeconomic stability. Dollarization effectively eliminated exchange rate risk, kept inflation low and aligned with US levels, and fostered confidence for both foreign investment and international banking, a key sector of Panama's economy. This stability was particularly notable amidst regional economic volatility in other Latin American nations during that period. However, the system also presented significant constraints. Panama had no ability to use monetary policy as a tool to respond to domestic economic cycles, such as stimulating growth during a downturn. Furthermore, the country's banking sector had to maintain strict liquidity and reserve management without a lender of last resort.

In 2017, this dollarized system functioned as normal, underpinning an economy that was experiencing steady growth, largely driven by the expanded Panama Canal, which had opened its new locks in 2016. The key discussions around currency were not about change but about managing the framework's inherent trade-offs. Policymakers focused on maintaining fiscal discipline as the sole major tool for economic management, ensuring robust foreign currency reserves, and overseeing a strong and well-capitalized banking system to mitigate the risks associated with the lack of an independent central bank.

The primary benefit of this system, evident in 2017, was macroeconomic stability. Dollarization effectively eliminated exchange rate risk, kept inflation low and aligned with US levels, and fostered confidence for both foreign investment and international banking, a key sector of Panama's economy. This stability was particularly notable amidst regional economic volatility in other Latin American nations during that period. However, the system also presented significant constraints. Panama had no ability to use monetary policy as a tool to respond to domestic economic cycles, such as stimulating growth during a downturn. Furthermore, the country's banking sector had to maintain strict liquidity and reserve management without a lender of last resort.

In 2017, this dollarized system functioned as normal, underpinning an economy that was experiencing steady growth, largely driven by the expanded Panama Canal, which had opened its new locks in 2016. The key discussions around currency were not about change but about managing the framework's inherent trade-offs. Policymakers focused on maintaining fiscal discipline as the sole major tool for economic management, ensuring robust foreign currency reserves, and overseeing a strong and well-capitalized banking system to mitigate the risks associated with the lack of an independent central bank.

Series: Panama Viejo

🌱 Fairly Common