20 escudos – Portugal

Add to wishlist

Portugal

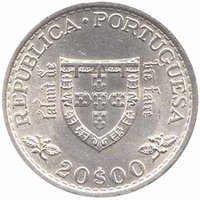

Obverse

Description:

A stylized Portuguese shield behind the denomination.

Inscription:

20 ESCUDOS

Script: Latin

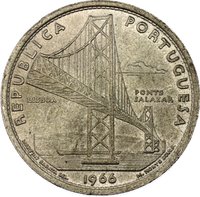

Reverse

Description:

Salazar Bridge, year at rim's base.

Inscription:

REPUBLICA PORTUGUESA

LISBOA PONTE SALAZAR

1966

MARTINS BARATA DEL.

M. NORTE SCULP.

LISBOA PONTE SALAZAR

1966

MARTINS BARATA DEL.

M. NORTE SCULP.

Translation:

PORTUGUESE REPUBLIC

LISBON SALAZAR BRIDGE

1966

MARTINS BARATA DEL.

M. NORTE SCULP.

LISBON SALAZAR BRIDGE

1966

MARTINS BARATA DEL.

M. NORTE SCULP.

Script: Latin

Language: Portuguese

Edge

Reeded

Categories

| Building> Bridge |

| Transportation> Watercraft |

Mints

| Name | Mark |

|---|---|

| Imprensa Nacional - Casa da Moeda | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1966 | — | 2,000,000 | ||

| 1966 | — | — | Matte |

Historical background

In 1966, Portugal's currency situation was defined by the Escudo, which had been the nation's currency since 1911, replacing the Real. The country operated under a fixed exchange rate regime, with the Escudo's value pegged to the U.S. Dollar as part of the Bretton Woods system. This peg provided a degree of international stability and predictability for trade, which was crucial for an economy still heavily reliant on colonial markets and agricultural exports. However, the regime also required strict capital controls and management by the Banco de Portugal to maintain the parity, limiting monetary policy flexibility.

Economically, the mid-1960s were a period of relative growth and modernization under the Estado Novo dictatorship, fueled by industrialization, tourism development, and remittances from emigrants. Despite this growth, underlying pressures were building. The cost of maintaining Portugal's colonial wars in Africa, which began in 1961, placed an increasing fiscal burden on the state, diverting resources and contributing to a rising national debt. Furthermore, the industrial push led to inflationary tendencies, which were difficult to manage under the rigid fixed exchange rate, creating occasional imbalances in the country's balance of payments.

Looking ahead, the stability of 1966 was precarious. The Bretton Woods system itself would begin to unravel in the early 1970s, leading to a major shift for the Escudo. More immediately, the relentless financial drain of the colonial conflicts would soon force a devaluation. In 1971, the Escudo was officially devalued against the Dollar, marking the beginning of a period of currency instability that would extend through the 1974 Carnation Revolution and beyond, as Portugal transitioned to democracy and grappled with the economic consequences of decolonization.

Economically, the mid-1960s were a period of relative growth and modernization under the Estado Novo dictatorship, fueled by industrialization, tourism development, and remittances from emigrants. Despite this growth, underlying pressures were building. The cost of maintaining Portugal's colonial wars in Africa, which began in 1961, placed an increasing fiscal burden on the state, diverting resources and contributing to a rising national debt. Furthermore, the industrial push led to inflationary tendencies, which were difficult to manage under the rigid fixed exchange rate, creating occasional imbalances in the country's balance of payments.

Looking ahead, the stability of 1966 was precarious. The Bretton Woods system itself would begin to unravel in the early 1970s, leading to a major shift for the Escudo. More immediately, the relentless financial drain of the colonial conflicts would soon force a devaluation. In 1971, the Escudo was officially devalued against the Dollar, marking the beginning of a period of currency instability that would extend through the 1974 Carnation Revolution and beyond, as Portugal transitioned to democracy and grappled with the economic consequences of decolonization.

Series: System 1927-1968

🌱 Very Common