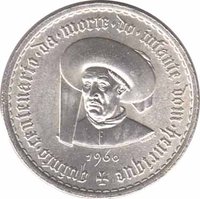

50 Escudos (Pedro Alvares Cabral) – Portugal

Circulating commemorative coins

Commemoration: 500th Anniversary of the Birth of Pedro Alvares Cabral

Series: System 1927-1968

Portugal

Obverse

Reverse

Description:

Bust with headdress in profile, encircled.

Inscription:

V CENTº NASCIMENTO DE PEDRO ALVARES CABRAL 1968

M.NORTE

M.NORTE

Translation:

Fifth Centenary of the Birth of Pedro Álvares Cabral 1968

M.Norte

M.Norte

Script: Latin

Language: Portuguese

Engraver: Marcelino Norte de Almeida

Edge

Reeded

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1968 | — | 1,000,000 | ||

| 1968 | — | 400 | Matte |

Historical background

In 1968, Portugal's currency situation was defined by the Escudo, which operated under a tightly controlled regime characteristic of the Estado Novo dictatorship led by António Salazar (and, from September of that year, his successor Marcelo Caetano). The economy was largely closed, protectionist, and focused on maintaining a balanced budget and a strong currency reserve. The escudo's value was fixed by the government and managed by the Bank of Portugal, with strict exchange controls limiting the flow of capital and access to foreign currency for both citizens and businesses. This stability, however, came at the cost of economic dynamism and international integration.

Internationally, the escudo was pegged to the U.S. dollar at a fixed rate of 28.75 Escudos to 1 USD, a parity maintained since 1949. This peg provided nominal stability but masked underlying economic pressures. A persistent trade deficit, low productivity, and the immense financial burden of fighting colonial wars in Africa (Angola, Mozambique, and Guinea-Bissau) since 1961 were draining the state's reserves. While not yet in crisis in 1968, the system was under growing strain, requiring continuous controls to defend the fixed parity and prevent capital flight.

Domestically, the currency regime reflected the regime's authoritarian nature. The government used monetary policy as a tool for political control, with regulations designed to funnel investment into state-prioritized sectors and restrict economic freedoms. For the average Portuguese citizen, this meant limited access to goods and services from abroad, difficulties in traveling or investing overseas, and an economy that was increasingly out of step with the rapid growth seen elsewhere in Western Europe. Thus, in 1968, the Portuguese escudo represented a fragile fortress—externally stable but internally pressured and symbolizing an isolated economy on the brink of future upheaval.

Internationally, the escudo was pegged to the U.S. dollar at a fixed rate of 28.75 Escudos to 1 USD, a parity maintained since 1949. This peg provided nominal stability but masked underlying economic pressures. A persistent trade deficit, low productivity, and the immense financial burden of fighting colonial wars in Africa (Angola, Mozambique, and Guinea-Bissau) since 1961 were draining the state's reserves. While not yet in crisis in 1968, the system was under growing strain, requiring continuous controls to defend the fixed parity and prevent capital flight.

Domestically, the currency regime reflected the regime's authoritarian nature. The government used monetary policy as a tool for political control, with regulations designed to funnel investment into state-prioritized sectors and restrict economic freedoms. For the average Portuguese citizen, this meant limited access to goods and services from abroad, difficulties in traveling or investing overseas, and an economy that was increasingly out of step with the rapid growth seen elsewhere in Western Europe. Thus, in 1968, the Portuguese escudo represented a fragile fortress—externally stable but internally pressured and symbolizing an isolated economy on the brink of future upheaval.

Series: System 1927-1968

🌱 Common