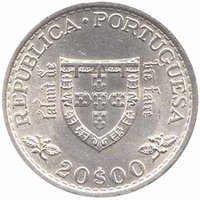

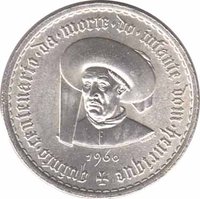

5 escudos (Infante D. Henrique) – Portugal

Add to wishlist

Circulating commemorative coins

Commemoration: V Centenary of the death of Infante D. Henrique

Series: System 1927-1968

Portugal

Obverse

Description:

A bust of Prince Henry the Navigator facing left, wearing a hat, encircled by the Gothic French motto "Talant de bien faire" (The will of well-doing), later adopted by the Portuguese Navy in his honor.

Inscription:

REPÚBLICA•PORTUGUESA

5$00

5$00

Translation:

Portuguese Republic

5$00

5$00

Script: Latin

Language: Portuguese

Engraver: Marcelino Norte de Almeida

Reverse

Description:

The Portuguese shield: five ⚄-shaped shields in a cross, encircled by seven castle towers and rich in legend.

Inscription:

QUINTO•CENTENARIO•DA•MORTE•DO•INFANTE•DOM•HENRIQUE ✠

1960

1960

Script: Latin

Engraver: Marcelino Norte de Almeida

Edge

Reeded

Mints

| Name | Mark |

|---|---|

| Imprensa Nacional - Casa da Moeda | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1960 | — | 800,000 | ||

| 1960 | — | — | Matte |

Historical background

In 1960, Portugal's currency situation was defined by the escudo, which had been the nation's sole legal tender since 1911, replacing the real. The system was strictly controlled under the authoritarian Estado Novo regime of António de Salazar, which prioritized stability, protectionism, and self-sufficiency through a complex framework of exchange controls. Portugal operated a fixed exchange rate regime, pegging the escudo to the U.S. dollar and, by extension through the Bretton Woods system, to gold. This peg was maintained at approximately 28.75 escudos to the dollar, a rate intended to project monetary discipline and shield the domestic economy from external volatility.

Internally, the currency regime was highly restrictive. The Banco de Portugal, closely aligned with government policy, enforced strict capital controls and multiple exchange rates for different types of transactions. This meant the escudo's value for importing essential goods differed from its value for tourism or capital movements. These measures aimed to conserve foreign reserves, protect Portugal's fledgling industries, and support its costly colonial wars in Africa, which began in 1961 and placed increasing strain on public finances. The economy remained relatively insulated, with limited convertibility ensuring that the official escudo rate was largely symbolic for international business.

Consequently, a significant black market for foreign currency flourished, particularly in major cities and tourist areas, where the escudo traded at a substantial discount compared to the official rate. This duality reflected the growing pressures on an inward-looking economy that was beginning to see the first waves of tourism and European integration, yet was still burdened by colonial commitments and rigid state control. The currency situation of 1960 thus represented a fragile equilibrium—outwardly stable but underpinned by controls that masked underlying economic tensions and isolation from Western Europe's accelerating growth.

Internally, the currency regime was highly restrictive. The Banco de Portugal, closely aligned with government policy, enforced strict capital controls and multiple exchange rates for different types of transactions. This meant the escudo's value for importing essential goods differed from its value for tourism or capital movements. These measures aimed to conserve foreign reserves, protect Portugal's fledgling industries, and support its costly colonial wars in Africa, which began in 1961 and placed increasing strain on public finances. The economy remained relatively insulated, with limited convertibility ensuring that the official escudo rate was largely symbolic for international business.

Consequently, a significant black market for foreign currency flourished, particularly in major cities and tourist areas, where the escudo traded at a substantial discount compared to the official rate. This duality reflected the growing pressures on an inward-looking economy that was beginning to see the first waves of tourism and European integration, yet was still burdened by colonial commitments and rigid state control. The currency situation of 1960 thus represented a fragile equilibrium—outwardly stable but underpinned by controls that masked underlying economic tensions and isolation from Western Europe's accelerating growth.

Series: System 1927-1968

🌱 Common