20 rappen – Switzerland

Add to wishlist

Switzerland

Context

Years: 1881–1938

Issuer: Switzerland

Period:

(since 1848)

Currency:

(since 1850)

Demonetization: 1 January 2004

Total mintage: 57,755,000

Material

References

KM: #

Numista: #177

Value

Exchange value: 0.20 CHF

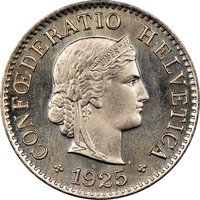

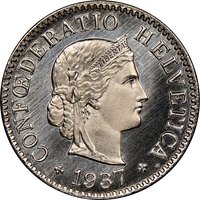

Obverse

Description:

Libertas facing right, with braided hair, ribbon, and tiara.

Inscription:

CONFŒDERATIO HELVETICA

LIBERTAS

⸭ 1896 ⸭

LIBERTAS

⸭ 1896 ⸭

Translation:

Confederation of Switzerland

Liberty

⸭ 1896 ⸭

Liberty

⸭ 1896 ⸭

Script: Latin

Language: Latin

Designer: Karl Schwenzer

Reverse

Description:

Alpine rose wreath tied with a ribbon.

Inscription:

20

B

B

Script: Latin

Designer: Carl Friedrich Voigt

Edge

Plain.

Mints

| Name | Mark |

|---|---|

| Bern | B |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1881 | B | 1,000,000 | ||

| 1883 | B | 2,500,000 | ||

| 1884 | B | 4,000,000 | ||

| 1885 | B | 3,000,000 | ||

| 1887 | B | 500,000 | ||

| 1891 | B | 1,000,000 | ||

| 1893 | B | 1,000,000 | ||

| 1894 | B | 1,000,000 | ||

| 1896 | B | 1,000,000 | ||

| 1897 | B | 500,000 | ||

| 1898 | B | 500,000 | ||

| 1899 | B | 500,000 | ||

| 1900 | B | 1,000,000 | ||

| 1901 | B | 1,000,000 | ||

| 1902 | B | 1,000,000 | ||

| 1903 | B | 1,000,000 | ||

| 1906 | B | 1,000,000 | ||

| 1907 | B | 1,000,000 | ||

| 1908 | B | 1,500,000 | ||

| 1909 | B | 2,000,000 | ||

| 1911 | B | 1,000,000 | ||

| 1912 | B | 2,000,000 | ||

| 1913 | B | 1,500,000 | ||

| 1919 | B | 1,500,000 | ||

| 1920 | B | 3,100,000 | ||

| 1921 | B | 2,500,000 | ||

| 1924 | B | 1,100,000 | ||

| 1925 | B | 1,500,000 | ||

| 1926 | B | 1,500,000 | ||

| 1927 | B | 500,000 | ||

| 1929 | B | 2,000,000 | ||

| 1930 | B | 2,000,000 | ||

| 1931 | B | 2,250,000 | ||

| 1932 | B | 2,000,000 | ||

| 1933 | B | 1,500,000 | ||

| 1934 | B | 2,000,000 | ||

| 1936 | B | 1,000,000 | ||

| 1938 | B | 2,805,000 |

Historical background

In 1881, Switzerland’s currency situation was one of transition and complexity, caught between cantonal sovereignty and the pressing need for national unification. Following the formation of the federal state in 1848, the Swiss franc was introduced as the national currency in 1850, replacing a chaotic system of over 8,000 different coins and notes issued by various cantons, cities, and private banks. However, full monetary integration was not yet achieved. While the federal government had exclusive rights to mint coins, banknote issuance remained decentralized and unregulated, leading to a proliferation of notes from dozens of private and cantonal banks of varying quality and reliability.

This fragmented note system created practical difficulties for commerce and travel, as the acceptance of private banknotes was inconsistent across cantonal borders. Furthermore, Switzerland was deeply embedded in the Latin Monetary Union (LMU), established in 1865 with France, Belgium, and Italy. This agreement standardized gold and silver coin specifications, making the currencies of member states legally interchangeable. While this facilitated international trade, it also tied Switzerland’s monetary policy to the union’s fortunes, exposing it to the inflationary risks of silver depreciation and the monetary policies of its larger partners, particularly France.

Therefore, the background in 1881 was defined by a dual challenge: internally, the need to consolidate and federalize banknote issuance to ensure financial stability and uniformity, and externally, the need to navigate the vulnerabilities of the LMU. These pressures would culminate just a few years later with the Federal Law on Banks and Banknotes of 1881, which, for the first time, imposed strict regulations on note-issuing banks—a crucial step toward the fully federalized monetary system established by the Swiss National Bank in 1907.

This fragmented note system created practical difficulties for commerce and travel, as the acceptance of private banknotes was inconsistent across cantonal borders. Furthermore, Switzerland was deeply embedded in the Latin Monetary Union (LMU), established in 1865 with France, Belgium, and Italy. This agreement standardized gold and silver coin specifications, making the currencies of member states legally interchangeable. While this facilitated international trade, it also tied Switzerland’s monetary policy to the union’s fortunes, exposing it to the inflationary risks of silver depreciation and the monetary policies of its larger partners, particularly France.

Therefore, the background in 1881 was defined by a dual challenge: internally, the need to consolidate and federalize banknote issuance to ensure financial stability and uniformity, and externally, the need to navigate the vulnerabilities of the LMU. These pressures would culminate just a few years later with the Federal Law on Banks and Banknotes of 1881, which, for the first time, imposed strict regulations on note-issuing banks—a crucial step toward the fully federalized monetary system established by the Swiss National Bank in 1907.

Series: Libertas series

🌱 Very Common