250 escudos – Portugal

Add to wishlist

Circulating commemorative coins

Commemoration: Carnation Revolution in 1974

Series: System 1981-2001

Portugal

Obverse

Description:

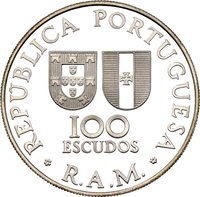

Crossed value in circle

Inscription:

250

ESCUDOS

REPUBLICA·PORTUGUESA·

ESCUDOS

REPUBLICA·PORTUGUESA·

Translation:

250

ESCUDOS

PORTUGUESE REPUBLIC

ESCUDOS

PORTUGUESE REPUBLIC

Script: Latin

Language: Portuguese

Reverse

Edge

Reeded

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1976 | — | 950,000 | ||

| 1976 | — | 10,000 | Proof |

Historical background

In 1976, Portugal's currency situation was deeply unstable, reflecting the nation's turbulent political and economic transition following the 1974 Carnation Revolution. The revolution had overthrown the authoritarian Estado Novo regime, but it also triggered a period of revolutionary upheaval, nationalizations, and a collapse in investor confidence. This resulted in high inflation, large fiscal and current account deficits, and a significant depletion of foreign exchange reserves. The Portuguese escudo, while still the official currency, was under severe pressure, with its value managed through a complex system of multiple exchange rates that attempted to control capital flows and prioritize essential imports.

Economically, the country was in crisis, grappling with the legacy of colonial wars and the sudden influx of retornados (returning colonists) from newly independent African territories. The government, now under a democratic constitution ratified in April 1976, faced the immense challenge of stabilizing the economy while maintaining socialist-inspired commitments to employment and public ownership. To address the external imbalances, Portugal relied heavily on foreign borrowing, particularly from the International Monetary Fund (IMF). A crucial stabilization loan from the IMF in 1977 would soon impose strict austerity conditions, forcing devaluations of the escudo and demanding reductions in the deficit, setting the stage for a painful economic adjustment.

Thus, the currency situation in 1976 was one of fragility and dependence. The escudo's value was artificially sustained by controls and was heading towards necessary devaluation as part of impending IMF agreements. The background was defined by the fundamental tension between the revolutionary political objectives of the new democracy and the harsh economic realities of inflation, debt, and external dependency, a conflict that would shape Portugal's economic policies for the remainder of the decade.

Economically, the country was in crisis, grappling with the legacy of colonial wars and the sudden influx of retornados (returning colonists) from newly independent African territories. The government, now under a democratic constitution ratified in April 1976, faced the immense challenge of stabilizing the economy while maintaining socialist-inspired commitments to employment and public ownership. To address the external imbalances, Portugal relied heavily on foreign borrowing, particularly from the International Monetary Fund (IMF). A crucial stabilization loan from the IMF in 1977 would soon impose strict austerity conditions, forcing devaluations of the escudo and demanding reductions in the deficit, setting the stage for a painful economic adjustment.

Thus, the currency situation in 1976 was one of fragility and dependence. The escudo's value was artificially sustained by controls and was heading towards necessary devaluation as part of impending IMF agreements. The background was defined by the fundamental tension between the revolutionary political objectives of the new democracy and the harsh economic realities of inflation, debt, and external dependency, a conflict that would shape Portugal's economic policies for the remainder of the decade.

Series: System 1981-2001

🌱 Common