1 escudo – Portugal

Add to wishlist

Portugal

Context

Years: 1981–1986

Issuer: Portugal

Period:

(since 1974)

Currency:

(1911—2001)

Demonetization: 28 February 2002

Total mintage: 256,568,775

Material

Diameter: 18 mm

Weight: 3 g

Thickness: 1.63 mm

Shape: Round

Composition: Nickel brass

Magnetic: No

Technique: Milled

Alignment: Coin alignment

flip

References

KM: #

Numista: #11952

Value

Exchange value: 1 PTE

Inflation-adjusted value: 12.81 PTE

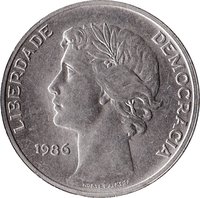

Obverse

Description:

Shield

Inscription:

REPUBLICA PORTUGUESA

1985

1985

Translation:

Portuguese Republic

1985

1985

Script: Latin

Language: Portuguese

Engraver: Marcelino Norte de Almeida

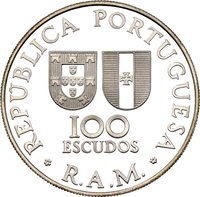

Reverse

Edge

Plain

Categories

| Symbols> Coat of Arms |

Mints

| Name | Mark |

|---|---|

| Imprensa Nacional - Casa da Moeda | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1981 | — | 30,164,739 | ||

| 1982 | — | 53,018,248 | ||

| 1983 | — | 53,165,700 | ||

| 1984 | — | 55,560,000 | ||

| 1985 | — | 56,630,000 | ||

| 1986 | — | 8,030,088 |

Historical background

In 1981, Portugal was navigating a turbulent economic transition following the 1974 Carnation Revolution, which had ended decades of dictatorship. The immediate post-revolutionary period was marked by political instability, nationalizations, and expansive fiscal policies, leading to high inflation, large public deficits, and a growing external debt. The country's currency, the Portuguese escudo (PTE), was under significant pressure, operating within a managed float but frequently requiring defensive interventions by the Banco de Portugal to maintain its value amidst capital flight and low foreign exchange reserves.

The currency situation was intrinsically linked to Portugal's broader economic challenges and its political aspirations. Having applied for membership in the European Economic Community (EEC) in 1977, the government was under domestic and international pressure to implement stabilization and liberalization programs. In 1978 and 1983, Portugal entered into agreements with the International Monetary Fund (IMF), which imposed strict austerity measures, including escudo devaluations, to restore competitiveness and curb the twin deficits. The 1981 period was thus a precarious prelude to a major escudo devaluation in 1983, as stopgap measures struggled to correct deep structural imbalances.

Consequently, the escudo in 1981 represented a weak and vulnerable currency, symbolizing an economy caught between its revolutionary past and a European future. The persistent economic crises of the early 1980s ultimately paved the way for profound reforms, setting the stage for Portugal's eventual EEC accession in 1986 and the later integration of the escudo into the European Exchange Rate Mechanism (ERM) in 1992, a stepping stone toward adopting the euro.

The currency situation was intrinsically linked to Portugal's broader economic challenges and its political aspirations. Having applied for membership in the European Economic Community (EEC) in 1977, the government was under domestic and international pressure to implement stabilization and liberalization programs. In 1978 and 1983, Portugal entered into agreements with the International Monetary Fund (IMF), which imposed strict austerity measures, including escudo devaluations, to restore competitiveness and curb the twin deficits. The 1981 period was thus a precarious prelude to a major escudo devaluation in 1983, as stopgap measures struggled to correct deep structural imbalances.

Consequently, the escudo in 1981 represented a weak and vulnerable currency, symbolizing an economy caught between its revolutionary past and a European future. The persistent economic crises of the early 1980s ultimately paved the way for profound reforms, setting the stage for Portugal's eventual EEC accession in 1986 and the later integration of the escudo into the European Exchange Rate Mechanism (ERM) in 1992, a stepping stone toward adopting the euro.

Series: System 1981-2001

🌱 Very Common