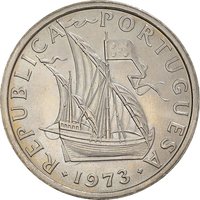

50 escudos (Os Lusíadas) – Portugal

Add to wishlist

Circulating commemorative coins

Commemoration: 400th Anniversary of "Os Lusiadas"

Series: System 1969-1980

Portugal

Obverse

Description:

Book in Quinas Cross, encircled.

Inscription:

REPVBLICA · PORTVGVESA

*50·ESCVDOS*

os lvsiadas

M.NORTE

*50·ESCVDOS*

os lvsiadas

M.NORTE

Engraver: Marcelino Norte de Almeida

Reverse

Description:

Victory and dates encircled.

Inscription:

IV CENTANARIO DA PVBLICACAO DE "OS LVSIADAS" *

1572//1972

1572//1972

Engraver: Marcelino Norte de Almeida

Edge

Reeded

Mints

| Name | Mark |

|---|---|

| Imprensa Nacional - Casa da Moeda | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1972 | — | 1,000,000 |

Historical background

In 1972, Portugal operated under the authoritarian Estado Novo regime and maintained a colonial empire, both of which fundamentally shaped its currency situation. The national currency was the escudo (PTE), which was part of a managed exchange rate system. It was pegged to the U.S. dollar at a fixed rate of $1 = 27.25 PTE, a parity established in 1949 and maintained through strict capital controls and the stewardship of the Banco de Portugal. This stability was a point of pride for the regime, projecting an image of economic order despite underlying structural weaknesses.

The economy was heavily protected, insular, and burdened by the immense financial and military costs of fighting colonial wars in Africa (Angola, Mozambique, and Guinea-Bissau). These wars consumed roughly 40% of the national budget, diverting resources from domestic investment and industrial modernization. While the escudo's official rate was stable, the pressures of wartime spending and a growing reliance on foreign borrowing created underlying inflationary pressures and a vulnerability in the balance of payments. The currency's artificial stability was, in many ways, sustained by isolation and control rather than robust economic health.

Internationally, Portugal was a founding member of the European Free Trade Association (EFTA) and had applied for a trade agreement with the European Economic Community (EEC). However, its political regime and colonial policies caused friction with other European nations. The escudo was not a freely convertible currency for most transactions, and its fixed parity would come under severe strain following the 1973 oil crisis. The rigid economic and currency model of 1972 was ultimately unsustainable, and it would be shattered by the Carnation Revolution of 1974, which would bring decolonization, economic turmoil, and significant currency devaluation in the years immediately following.

The economy was heavily protected, insular, and burdened by the immense financial and military costs of fighting colonial wars in Africa (Angola, Mozambique, and Guinea-Bissau). These wars consumed roughly 40% of the national budget, diverting resources from domestic investment and industrial modernization. While the escudo's official rate was stable, the pressures of wartime spending and a growing reliance on foreign borrowing created underlying inflationary pressures and a vulnerability in the balance of payments. The currency's artificial stability was, in many ways, sustained by isolation and control rather than robust economic health.

Internationally, Portugal was a founding member of the European Free Trade Association (EFTA) and had applied for a trade agreement with the European Economic Community (EEC). However, its political regime and colonial policies caused friction with other European nations. The escudo was not a freely convertible currency for most transactions, and its fixed parity would come under severe strain following the 1973 oil crisis. The rigid economic and currency model of 1972 was ultimately unsustainable, and it would be shattered by the Carnation Revolution of 1974, which would bring decolonization, economic turmoil, and significant currency devaluation in the years immediately following.

Series: System 1969-1980

🌱 Common