50 colones – Costa Rica

Add to wishlist

Costa Rica

Context

Years: 2006–2017

Issuer: Costa Rica

Issuing organization: Central Bank of Costa Rica

Period:

(since 1948)

Currency:

(since 1896)

Demonetization: 1 July 2025

Total mintage: 101,000,000

Material

References

KM: #

Numista: #8486

Value

Exchange value: 50 CRC

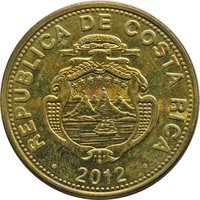

Obverse

Description:

Costa Rica's coat of arms features seven stars for its provinces, three volcanoes for its mountain ranges, two ships for its position between oceans, and a rising sun.

Inscription:

REPUBLICA DE COSTA RICA

AMERICA CENTRAL

REPUBLICA DE COSTA RICA

· 2012 ·

AMERICA CENTRAL

REPUBLICA DE COSTA RICA

· 2012 ·

Translation:

REPUBLIC OF COSTA RICA

CENTRAL AMERICA

REPUBLIC OF COSTA RICA

· 2012 ·

CENTRAL AMERICA

REPUBLIC OF COSTA RICA

· 2012 ·

Script: Latin

Language: Spanish

Reverse

Edge

Alternating segments of 4 smooth and 4 reeded parts (segmented)

Categories

| Symbol> Wreath |

| Transportation> Watercraft |

| Symbols> Coat of Arms |

| Geography> Mountain |

Mints

| Name | Mark |

|---|---|

| Casa de Moneda de Chile | — |

| Mint of Costa Rica | — |

| Royal Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2006 | — | 5,000,000 | ||

| 2010 | — | 36,000,000 | ||

| 2012 | — | 30,000,000 | ||

| 2015 | — | 20,000,000 | ||

| 2017 | — | 10,000,000 |

Historical background

In 2006, Costa Rica's currency situation was defined by a managed float regime for the colón (₡) within a crawling band, a system administered by the Central Bank of Costa Rica (BCCR). The colón was allowed to depreciate gradually against the US dollar at a pre-announced rate, intended to maintain export competitiveness while controlling inflationary pressures from imported goods. This system created a relatively stable but predictable depreciation, with the exchange rate hovering around ₡500 to the US dollar by the end of the year, a slow but steady decline from ₡440 in early 2005.

The period was marked by significant dollarization within the financial system, a legacy from high inflation episodes in the 1980s and 1990s. A substantial portion of loans (over 50%) and deposits were denominated in US dollars, particularly for large transactions like mortgages and car loans, exposing borrowers to exchange rate risk. This duality created a complex environment where the Central Bank's monetary policy was less effective, as many economic actors operated outside the colón system. Furthermore, strong capital inflows, including foreign direct investment and remittances, alongside a growing tourism sector, consistently placed upward pressure on the colón, challenging the BCCR's management of the crawling band.

Overall, the 2006 currency landscape reflected a transitional economy grappling with the contradictions of openness. The managed float aimed for stability, but high dollarization and persistent inflows highlighted underlying tensions. These factors fueled ongoing debate about the sustainability of the crawling band and intensified discussions—which would culminate in later years—about potentially moving towards a more flexible exchange rate system to better absorb external shocks and improve monetary policy autonomy.

The period was marked by significant dollarization within the financial system, a legacy from high inflation episodes in the 1980s and 1990s. A substantial portion of loans (over 50%) and deposits were denominated in US dollars, particularly for large transactions like mortgages and car loans, exposing borrowers to exchange rate risk. This duality created a complex environment where the Central Bank's monetary policy was less effective, as many economic actors operated outside the colón system. Furthermore, strong capital inflows, including foreign direct investment and remittances, alongside a growing tourism sector, consistently placed upward pressure on the colón, challenging the BCCR's management of the crawling band.

Overall, the 2006 currency landscape reflected a transitional economy grappling with the contradictions of openness. The managed float aimed for stability, but high dollarization and persistent inflows highlighted underlying tensions. These factors fueled ongoing debate about the sustainability of the crawling band and intensified discussions—which would culminate in later years—about potentially moving towards a more flexible exchange rate system to better absorb external shocks and improve monetary policy autonomy.

🌱 Very Common