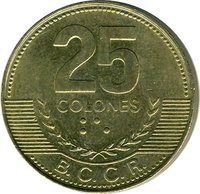

25 colones – Costa Rica

Add to wishlist

Costa Rica

Context

Year: 2005

Issuer: Costa Rica

Issuing organization: Central Bank of Costa Rica

Period:

(since 1948)

Currency:

(since 1896)

Total mintage: 30,000,000

Material

References

KM: #

Numista: #236581

Value

Exchange value: 25 CRC

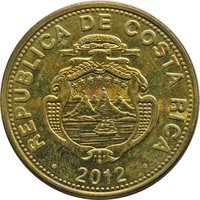

Obverse

Description:

Costa Rica's coat of arms features seven stars for its provinces, three volcanoes for its mountain ranges, two ships for its position between oceans, and a sunrise, with the date below.

Inscription:

REPUBLICA DE COSTA RICA

AMERICA CENTRAL

REPUBLICA DE COSTA RICA

2005

AMERICA CENTRAL

REPUBLICA DE COSTA RICA

2005

Translation:

REPUBLIC OF COSTA RICA

CENTRAL AMERICA

REPUBLIC OF COSTA RICA

2005

CENTRAL AMERICA

REPUBLIC OF COSTA RICA

2005

Script: Latin

Language: Spanish

Reverse

Edge

Plain

Categories

| Symbols> Coat of Arms |

| Symbol> Wreath |

Mints

| Name | Mark |

|---|---|

| Casa de Moneda de Chile | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2005 | — | 30,000,000 |

Historical background

In 2005, Costa Rica's currency situation was defined by a managed float regime for the colón (₡) against a basket of major currencies, though the US dollar remained the dominant reference. The Central Bank of Costa Rica (BCCR) actively intervened in the foreign exchange market to mitigate excessive volatility, but generally allowed the colón to depreciate gradually. This policy aimed to maintain export competitiveness—a critical concern for an economy reliant on agriculture, tourism, and electronics exports—while also trying to control inflationary pressures that a weakening currency could import.

The period was marked by significant dollarization of the financial system, a legacy of high inflation and instability from previous decades. A substantial portion of loans (over 50%) and deposits were denominated in US dollars, creating a widespread currency mismatch for many households and businesses earning in colones but borrowing in dollars. This created systemic vulnerability, as a sharp depreciation of the colón would drastically increase the real burden of dollar-denominated debt, posing risks to financial stability and consumer solvency.

Furthermore, 2005 fell within a contentious political debate about Central Bank independence and the direction of exchange rate policy. Pressure from some export sectors for a weaker colón conflicted with concerns over inflation and the dollarization dilemma. The year underscored the ongoing challenge for policymakers: balancing the competing needs of a small, open economy. These tensions would eventually contribute to a shift towards a more flexible exchange rate system in the following years, as Costa Rica grappled with integrating into the global economy while managing domestic financial risks.

The period was marked by significant dollarization of the financial system, a legacy of high inflation and instability from previous decades. A substantial portion of loans (over 50%) and deposits were denominated in US dollars, creating a widespread currency mismatch for many households and businesses earning in colones but borrowing in dollars. This created systemic vulnerability, as a sharp depreciation of the colón would drastically increase the real burden of dollar-denominated debt, posing risks to financial stability and consumer solvency.

Furthermore, 2005 fell within a contentious political debate about Central Bank independence and the direction of exchange rate policy. Pressure from some export sectors for a weaker colón conflicted with concerns over inflation and the dollarization dilemma. The year underscored the ongoing challenge for policymakers: balancing the competing needs of a small, open economy. These tensions would eventually contribute to a shift towards a more flexible exchange rate system in the following years, as Costa Rica grappled with integrating into the global economy while managing domestic financial risks.

🌱 Very Common