5 tambala – Malawi

Add to wishlist

Malawi

Context

Years: 1989–1994

Issuer: Malawi

Period:

(since 1966)

Ruler: Hastings Kamuzu Banda

Currency:

(since 1971)

Material

References

KM: #

Numista: #7904

Value

Exchange value: 0.05 MWK

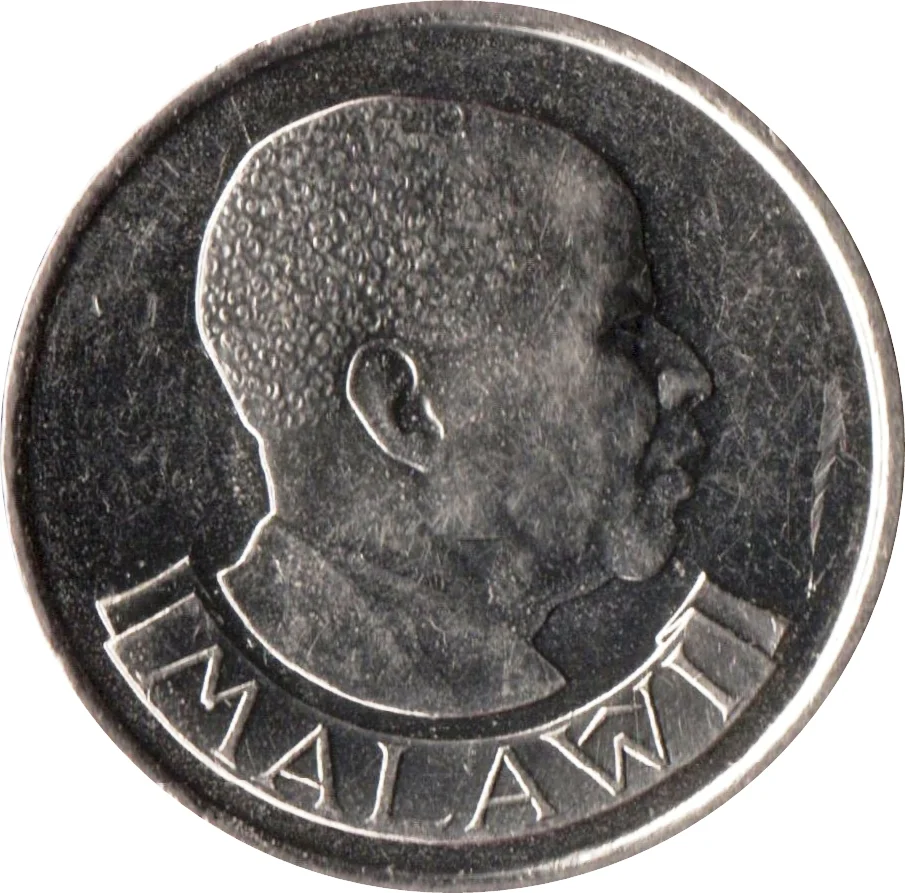

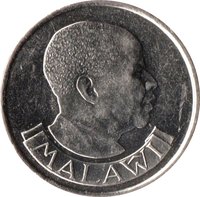

Obverse

Description:

Portrait of Hastings Kamuzu Banda.

Inscription:

MALAŴI

Translation:

MALAWI

Script: Latin

Language: Chichewa

Designer: Paul Vincze

Reverse

Description:

Heron in water, facing left.

Inscription:

1994

5

TAMBALA

P.V.

5

TAMBALA

P.V.

Script: Latin

Designer: Paul Vincze

Edge

Milled.

Categories

| Animal> Bird |

| Person> Politician |

Mints

| Name | Mark |

|---|---|

| Royal Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1989 | — | — | ||

| 1991 | — | — | ||

| 1994 | — | — |

Historical background

In 1989, Malawi's currency situation was characterized by a rigid and overvalued official exchange rate for the Malawian kwacha, maintained through strict exchange controls under the long-standing rule of President Hastings Kamuzu Banda. The country operated a complex multi-tier exchange rate system, with a primary official rate fixed by the Reserve Bank of Malawi and applied to essential imports like fuel, medicines, and agricultural inputs. However, this official rate did not reflect economic realities, creating a significant disparity with the parallel (black) market rate, where the kwacha traded at a substantial discount due to scarcity of foreign exchange and strong demand.

This overvaluation, coupled with a persistent current account deficit and heavy reliance on agricultural exports (notably tobacco, tea, and sugar), led to chronic foreign exchange shortages. The situation was exacerbated by deteriorating terms of trade, high external debt servicing costs, and inefficient state-owned enterprises. Consequently, legitimate businesses faced severe difficulties obtaining forex for necessary imports and equipment, stifling investment and growth. The thriving parallel market, while providing some liquidity, distorted the economy, encouraged corruption, and diverted resources away from formal channels.

The currency rigidity in 1989 was a symptom of broader macroeconomic imbalances and a highly controlled economic model. While providing short-term stability for a narrow range of government-prioritized transactions, the system imposed significant long-term costs by masking inefficiencies, discouraging exports, and creating a major bottleneck for the private sector. This unsustainable position set the stage for the structural adjustment programs and eventual devaluations and liberalization that would be reluctantly pursued in the early 1990s under pressure from the International Monetary Fund and World Bank.

This overvaluation, coupled with a persistent current account deficit and heavy reliance on agricultural exports (notably tobacco, tea, and sugar), led to chronic foreign exchange shortages. The situation was exacerbated by deteriorating terms of trade, high external debt servicing costs, and inefficient state-owned enterprises. Consequently, legitimate businesses faced severe difficulties obtaining forex for necessary imports and equipment, stifling investment and growth. The thriving parallel market, while providing some liquidity, distorted the economy, encouraged corruption, and diverted resources away from formal channels.

The currency rigidity in 1989 was a symptom of broader macroeconomic imbalances and a highly controlled economic model. While providing short-term stability for a narrow range of government-prioritized transactions, the system imposed significant long-term costs by masking inefficiencies, discouraging exports, and creating a major bottleneck for the private sector. This unsustainable position set the stage for the structural adjustment programs and eventual devaluations and liberalization that would be reluctantly pursued in the early 1990s under pressure from the International Monetary Fund and World Bank.

🌱 Common