20 Kwacha – Malawi

Malawi

Context

Material

Diameter: 38.6 mm

Weight: 31.4 g

Silver weight: 29.05 g

Thickness: 3.36 mm

Shape: Round

Composition: 92.5% Silver

Standard: Silver ounce

Magnetic: No

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #Click to copy to clipboard35

Numista: #68445

Value

Exchange value: 20 MWK

Bullion value: $83.13

Obverse

Description:

Coat of Arms of Malawi, with date.

Inscription:

REPUBLIC OF MALAWI

UNITY AND FREEDOM

1996

UNITY AND FREEDOM

1996

Script: Latin

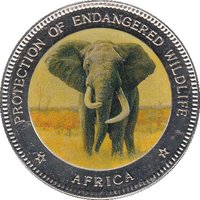

Reverse

Description:

African elephants with calves in water.

Inscription:

ENDANGERED WILDLIFE

20 KWACHA

20 KWACHA

Script: Latin

Edge

Reeded

Categories

| Animal> Elephant |

| Symbols> Coat of Arms |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1996 | — | 15,000 |

Historical background

In 1996, Malawi's currency situation was defined by a period of relative stability under a fixed exchange rate regime, but one that masked underlying economic vulnerabilities. The Malawian kwacha (MWK) was pegged to a basket of currencies, heavily weighted towards the US dollar, at an official rate of approximately 15.3 kwacha to one US dollar. This peg, managed by the Reserve Bank of Malawi (RBM), was maintained to provide predictability for trade and investment, a policy supported by the International Monetary Fund (IMF) as part of a structural adjustment programme.

However, this official stability existed alongside a thriving black market, where the kwacha traded at a significant discount, often around 30 to 40 percent weaker. This disparity highlighted the overvaluation of the official rate, which hurt export competitiveness for key commodities like tobacco, tea, and sugar. The fixed rate, combined with loose fiscal and monetary policies, led to a steady depletion of foreign exchange reserves, making it difficult for businesses to access hard currency for essential imports through official channels.

Consequently, 1996 represented the calm before a major monetary crisis. The pressures from the overvalued currency, dwindling reserves, and conditionalities from international donors created an unsustainable position. These mounting imbalances would ultimately force the government to abandon the peg just a few years later, leading to a substantial devaluation in 1998 as part of broader economic liberalisation measures demanded by the IMF and World Bank.

However, this official stability existed alongside a thriving black market, where the kwacha traded at a significant discount, often around 30 to 40 percent weaker. This disparity highlighted the overvaluation of the official rate, which hurt export competitiveness for key commodities like tobacco, tea, and sugar. The fixed rate, combined with loose fiscal and monetary policies, led to a steady depletion of foreign exchange reserves, making it difficult for businesses to access hard currency for essential imports through official channels.

Consequently, 1996 represented the calm before a major monetary crisis. The pressures from the overvalued currency, dwindling reserves, and conditionalities from international donors created an unsustainable position. These mounting imbalances would ultimately force the government to abandon the peg just a few years later, leading to a substantial devaluation in 1998 as part of broader economic liberalisation measures demanded by the IMF and World Bank.

Series: Endangered Wildlife

✨ Legendary