100 pounds – Egypt

Add to wishlist

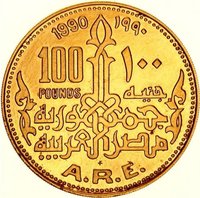

Egypt

Obverse

Inscription:

1989 ١٩٨٩

100 ١٠٠

POUNDS جنيه

جمهورية

مصر العربية

A.R.E.

100 ١٠٠

POUNDS جنيه

جمهورية

مصر العربية

A.R.E.

Translation:

1989 1989

100 100

POUNDS POUNDS

Arab Republic

of Egypt

A.R.E.

100 100

POUNDS POUNDS

Arab Republic

of Egypt

A.R.E.

Scripts: Arabic (kufic), Latin

Reverse

Description:

Bastet, the cat goddess.

Edge

Mints

| Name | Mark |

|---|---|

| Franklin Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1989 | — | 1,200 | Proof |

Historical background

In 1989, Egypt's currency situation was characterized by a complex and unsustainable multi-exchange rate system, a legacy of the 1970s Infitah (open-door) policy. The government maintained an official fixed rate for essential imports and debt servicing, while a parallel "free market" rate, significantly more depreciated, governed most other transactions. This duality, alongside a black market, created major distortions, encouraged corruption, and led to a critical shortage of foreign currency. The Egyptian pound was widely considered overvalued at the official rate, draining reserves and creating a persistent balance of payments crisis.

The root causes were deeply structural. Years of heavy subsidies, a large public sector, and inefficient state industries placed immense pressure on the national budget and import bill. Reliance on volatile sources of foreign exchange—like oil exports, Suez Canal tolls, tourism, and remittances—left the economy vulnerable to external shocks. By the late 1980s, falling oil prices and accumulated debt had brought the system to a breaking point, with foreign currency reserves covering only a few weeks of imports.

Consequently, 1989 marked a pivotal year of negotiation and impending change. The Egyptian government was engaged in intensive talks with the International Monetary Fund (IMF) and the World Bank to secure financial support and debt rescheduling. A core condition for any agreement was a commitment to a comprehensive Economic Reform and Structural Adjustment Program (ERSAP), which would necessitate the unification and devaluation of the Egyptian pound. Therefore, the currency situation in 1989 was one of precarious stasis, setting the stage for the dramatic reforms that would be implemented in the early 1990s.

The root causes were deeply structural. Years of heavy subsidies, a large public sector, and inefficient state industries placed immense pressure on the national budget and import bill. Reliance on volatile sources of foreign exchange—like oil exports, Suez Canal tolls, tourism, and remittances—left the economy vulnerable to external shocks. By the late 1980s, falling oil prices and accumulated debt had brought the system to a breaking point, with foreign currency reserves covering only a few weeks of imports.

Consequently, 1989 marked a pivotal year of negotiation and impending change. The Egyptian government was engaged in intensive talks with the International Monetary Fund (IMF) and the World Bank to secure financial support and debt rescheduling. A core condition for any agreement was a commitment to a comprehensive Economic Reform and Structural Adjustment Program (ERSAP), which would necessitate the unification and devaluation of the Egyptian pound. Therefore, the currency situation in 1989 was one of precarious stasis, setting the stage for the dramatic reforms that would be implemented in the early 1990s.

Series: Ancient Egyptian Treasures

✨ Legendary