100 pounds – Egypt

Add to wishlist

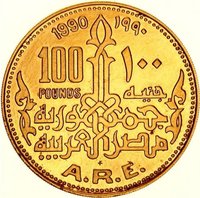

Egypt

Obverse

Reverse

Description:

Amon’s ram head.

Edge

Categories

| Animal |

Mints

| Name | Mark |

|---|---|

| Franklin Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1987 | — | 2,500 | Proof |

Historical background

In 1987, Egypt's currency situation was characterized by a severe and entrenched parallel market for foreign exchange, primarily the US dollar. The official exchange rate, fixed by the Central Bank of Egypt (CBE), was set at approximately EGP 0.70 to the dollar, a rate that was artificially strong and did not reflect economic realities. However, a vast and active black market operated where the Egyptian pound traded at a significant discount, often exceeding EGP 1.20 to the dollar. This wide disparity created a two-tier economy, incentivizing capital flight, discouraging vital remittances through official channels, and distorting trade and investment.

The root causes of this crisis were multifaceted, stemming from long-standing structural issues. Egypt faced a chronic balance of payments deficit, burdensome external debt, and low foreign currency reserves. Government policies, including extensive subsidies and a large public sector, fueled high inflation and budget deficits. Furthermore, the fixed official rate, maintained to control import costs and service foreign debt, was unsustainable. It created a scarcity of hard currency within the official banking system, forcing most businesses and individuals to resort to the black market to meet their foreign exchange needs, thereby perpetuating its dominance.

The government of President Hosni Mubarak, under pressure from the International Monetary Fund (IMF), had begun to acknowledge the necessity of reform. The year 1987 itself saw a pivotal step with the signing of a standby agreement with the IMF, which included commitments to unify the exchange rate and move toward a more flexible system. While a full devaluation and unification would not occur until the major economic reforms of 1991, the 1987 agreement marked the critical beginning of the end for the rigid dual-rate system, setting the stage for the painful but necessary economic liberalization to come.

The root causes of this crisis were multifaceted, stemming from long-standing structural issues. Egypt faced a chronic balance of payments deficit, burdensome external debt, and low foreign currency reserves. Government policies, including extensive subsidies and a large public sector, fueled high inflation and budget deficits. Furthermore, the fixed official rate, maintained to control import costs and service foreign debt, was unsustainable. It created a scarcity of hard currency within the official banking system, forcing most businesses and individuals to resort to the black market to meet their foreign exchange needs, thereby perpetuating its dominance.

The government of President Hosni Mubarak, under pressure from the International Monetary Fund (IMF), had begun to acknowledge the necessity of reform. The year 1987 itself saw a pivotal step with the signing of a standby agreement with the IMF, which included commitments to unify the exchange rate and move toward a more flexible system. While a full devaluation and unification would not occur until the major economic reforms of 1991, the 1987 agreement marked the critical beginning of the end for the rigid dual-rate system, setting the stage for the painful but necessary economic liberalization to come.

Series: Ancient Egyptian Treasures

✨ Legendary