1 Sovereign – United Kingdom

United Kingdom

Context

Years: 1838–1874

Issuer: United Kingdom

Ruler: Victoria

Currency:

(1158—1970)

Total mintage: 105,170,901

Material

References

KM: #Click to copy to clipboard736

Numista: #5760

Value

Bullion value: $1224.24

Obverse

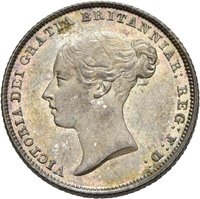

Description:

Young Victoria, uncrowned, left-facing portrait with surrounding legend.

Inscription:

VICTORIA DEI GRATIA

1871

1871

Translation:

Victoria by the Grace of God

Script: Latin

Language: Latin

Engraver: William Wyon

Reverse

Description:

Shield quartered in wreath, legend around, floral emblems below.

Inscription:

BRITANNIARUM REGINA FID: DEF:

Translation:

Queen of the Britains, Defender of the Faith

Script: Latin

Language: Latin

Engraver: Jean Baptiste Merlen

Edge

Reeded

Mints

| Name | Mark |

|---|---|

| Royal Mint (Tower Hill) | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1838 | — | 2,718,694 | ||

| 1838 | — | — | Proof | |

| 1839 | — | 503,695 | ||

| 1839 | — | — | Proof | |

| 1841 | — | 124,054 | ||

| 1842 | — | 4,865,375 | ||

| 1843 | — | — | ||

| 1844 | — | 3,000,445 | ||

| 1845 | — | 3,800,845 | ||

| 1846 | — | 3,802,947 | ||

| 1847 | — | 4,667,126 | ||

| 1848 | — | 2,246,701 | ||

| 1849 | — | 1,755,399 | ||

| 1850 | — | 1,402,039 | ||

| 1851 | — | 4,013,624 | ||

| 1852 | — | 8,053,435 | ||

| 1853 | — | — | Proof | |

| 1853 | — | — | ||

| 1854 | — | — | ||

| 1855 | — | — | ||

| 1856 | — | 4,806,160 | ||

| 1857 | — | 4,495,748 | ||

| 1858 | — | 803,234 | ||

| 1859 | — | — | ||

| 1860 | — | 2,555,958 | ||

| 1861 | — | 7,624,346 | ||

| 1862 | — | 7,836,413 | ||

| 1863 | — | — | ||

| 1864 | — | 8,656,353 | ||

| 1865 | — | 1,450,238 | ||

| 1866 | — | 4,047,228 | ||

| 1868 | — | 1,653,384 | ||

| 1869 | — | 6,441,322 | ||

| 1870 | — | 2,189,960 | ||

| 1871 | — | 8,767,250 | ||

| 1872 | — | — | ||

| 1873 | — | 2,368,215 | ||

| 1874 | — | 520,713 |

Historical background

In 1838, the United Kingdom was operating under a de facto gold standard, established following the landmark Resumption Act of 1819. This legislation had mandated a return to gold convertibility after the suspension during the Napoleonic Wars, a process completed in 1821. The official price was set at £3 17s 10½d per ounce of gold, meaning Bank of England notes were freely exchangeable for gold bullion upon demand. This system aimed to ensure monetary discipline and stability, but it existed alongside a complex mix of circulating media, including gold sovereigns, Bank of England notes (which were legal tender), and a plethora of private provincial banknotes of varying reliability.

The period was, however, one of intense monetary controversy. A powerful political and intellectual movement, the Currency School, argued that the existing system was inherently unstable. They believed that the over-issuance of banknotes by country banks, not fully backed by gold reserves, fuelled speculative booms and painful busts, like the crisis of 1825. Their proposed solution, which would culminate in the Bank Charter Act of 1844, was to rigidly tie the issuance of banknotes to the Bank of England's gold reserves, effectively creating a monopoly on note-issue for the central bank to prevent oversupply.

Opposing them, the Banking School contended that the Currency School's analysis was flawed. They argued that banknotes were merely a component of a broader credit system and that restricting their issue alone would not prevent crises, instead potentially exacerbating commercial credit shortages. For the ordinary person in 1838, the debate was abstract, but its implications were real: the stability of the money they used, the availability of credit for businesses, and the nation's overall economic health hung in the balance, setting the stage for the pivotal legislative battle of the following decade.

The period was, however, one of intense monetary controversy. A powerful political and intellectual movement, the Currency School, argued that the existing system was inherently unstable. They believed that the over-issuance of banknotes by country banks, not fully backed by gold reserves, fuelled speculative booms and painful busts, like the crisis of 1825. Their proposed solution, which would culminate in the Bank Charter Act of 1844, was to rigidly tie the issuance of banknotes to the Bank of England's gold reserves, effectively creating a monopoly on note-issue for the central bank to prevent oversupply.

Opposing them, the Banking School contended that the Currency School's analysis was flawed. They argued that banknotes were merely a component of a broader credit system and that restricting their issue alone would not prevent crises, instead potentially exacerbating commercial credit shortages. For the ordinary person in 1838, the debate was abstract, but its implications were real: the stability of the money they used, the availability of credit for businesses, and the nation's overall economic health hung in the balance, setting the stage for the pivotal legislative battle of the following decade.

🌱 Fairly Common