½ Farthing – United Kingdom

United Kingdom

Context

Years: 1839–1856

Issuer: United Kingdom

Ruler: Victoria

Currency:

(1158—1970)

Demonetization: 31 December 1869

Total mintage: 17,566,500

Material

References

KM: #Click to copy to clipboard738

Numista: #8480

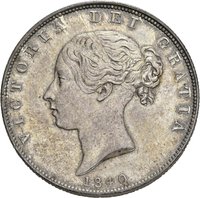

Obverse

Description:

Queen Victoria's first "Young Head" portrait, left-facing, with surrounding legend.

Inscription:

VICTORIA D:G: BRITANNIAR: REGINA F:D:

Translation:

Victoria by the Grace of God, Queen of the Britains, Defender of the Faith.

Script: Latin

Language: Latin

Engraver: William Wyon

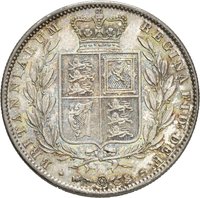

Reverse

Description:

Central crown above date, flanked by rose, thistle, and shamrock below. (1839 issues feature only a rose.)

Inscription:

HALF

FARTHING

1844

FARTHING

1844

Script: Latin

Edge

Plain

Mints

| Name | Mark |

|---|---|

| Royal Mint (Tower Hill) | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1839 | — | 2,042,800 | ||

| 1842 | — | — | ||

| 1843 | — | 3,440,600 | ||

| 1844 | — | 6,451,000 | ||

| 1847 | — | 3,010,500 | ||

| 1851 | — | — | ||

| 1852 | — | 989,100 | ||

| 1853 | — | 955,200 | ||

| 1853 | — | — | Proof | |

| 1854 | — | 677,300 | ||

| 1856 | — | — |

Historical background

In 1839, the United Kingdom was at a pivotal juncture in its monetary history, operating under a de facto gold standard that had been formally established by the 1816 Coinage Act. The system, known as the "specie standard," required the Bank of England to convert its notes into gold bullion or coin upon demand at the fixed rate of £3 17s 10½d per ounce. However, this commitment was under severe strain. A financial crisis in 1836-1837, combined with poor harvests and significant outflows of gold to finance foreign investments and trade deficits (particularly with China ahead of the Opium War), had depleted the Bank's bullion reserves. This created a climate of anxiety, as the Bank's ability to maintain convertibility—the bedrock of financial stability—was being questioned.

The core tension lay in the conflict between the "Currency School" and the "Banking School" of economic thought. The Currency School, led by figures like Lord Overstone, argued that note issuance must be strictly tied to gold reserves to prevent inflation and crises. They blamed the Bank for over-issuing notes, thereby causing the gold drain. Conversely, the Banking School believed the Bank's discretionary management of credit was essential for commerce and that notes merely responded to the needs of trade. In 1839, the pressure became acute; the Bank's gold reserve fell to a perilously low level, threatening a suspension of payments like the one during the Napoleonic Wars. To avert disaster, the Bank took the extraordinary step of secretly borrowing £2 million in gold from the Banque de France, a move underscoring the severity of the situation and the interconnectedness of European finance.

This crisis of 1839 directly set the stage for the landmark Bank Charter Act of 1844. The near-catastrophe strengthened the political hand of the Currency School, whose principles formed the Act's core. The 1844 legislation irrevocably pegged the pound to gold by strictly separating the Bank's issuing department from its banking functions and tying note issuance tightly to its gold reserve. Thus, the currency situation of 1839 was the final, turbulent prelude to the formal and rigid gold standard that would define British monetary policy for nearly a century, cementing the pound sterling's role as the anchor of the global financial system.

The core tension lay in the conflict between the "Currency School" and the "Banking School" of economic thought. The Currency School, led by figures like Lord Overstone, argued that note issuance must be strictly tied to gold reserves to prevent inflation and crises. They blamed the Bank for over-issuing notes, thereby causing the gold drain. Conversely, the Banking School believed the Bank's discretionary management of credit was essential for commerce and that notes merely responded to the needs of trade. In 1839, the pressure became acute; the Bank's gold reserve fell to a perilously low level, threatening a suspension of payments like the one during the Napoleonic Wars. To avert disaster, the Bank took the extraordinary step of secretly borrowing £2 million in gold from the Banque de France, a move underscoring the severity of the situation and the interconnectedness of European finance.

This crisis of 1839 directly set the stage for the landmark Bank Charter Act of 1844. The near-catastrophe strengthened the political hand of the Currency School, whose principles formed the Act's core. The 1844 legislation irrevocably pegged the pound to gold by strictly separating the Bank's issuing department from its banking functions and tying note issuance tightly to its gold reserve. Thus, the currency situation of 1839 was the final, turbulent prelude to the formal and rigid gold standard that would define British monetary policy for nearly a century, cementing the pound sterling's role as the anchor of the global financial system.

🌱 Common