1 Lats – Latvia

Non-circulating coins

Commemoration: Famous Latvians: Krišjānis Barons.

Latvia

Context

Material

Diameter: 38.61 mm

Weight: 31.47 g

Silver weight: 29.11 g

Shape: Round

Composition: 92.5% Silver

Standard: Silver ounce

Magnetic: No

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #Click to copy to clipboard79

Numista: #30560

Value

Exchange value: 1 LVL

Bullion value: $82.75

Inflation-adjusted value: 2.18 LVL

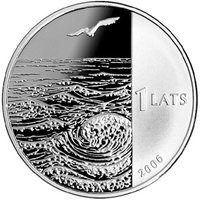

Obverse

Description:

The coin's obverse is vertically split (2:1). The right side centers "1 LATS" with 2006 arched below, while the left side depicts a starry sky.

Inscription:

1 LATS

2006

2006

Script: Latin

Engraver: Ligita Franckeviča

Designer: Arta Ozola - Jaunarāja

Reverse

Description:

The coin's reverse is vertically split (1:2 ratio). The right side shows Krisjanis Barons' portrait with the semicircular inscription "KAS VAR ZVAIGZNES SASKAITĪT…" and his facsimile signature. The left side depicts a starry sky.

Inscription:

KAS VAR ZVAIGZNES SASKAITĪT...

K Barons

K Barons

Translation:

Who could count the stars...

Script: Latin

Language: Latvian

Engraver: Ligita Franckeviča

Designer: Arta Ozola - Jaunarāja

Edge

Legend:

LATVIJAS REPUBLIKA ● LATVIJAS BANKA ●

Translation:

REPUBLIC OF LATVIA ● BANK OF LATVIA ●

Language: Latvian

Mints

| Name | Mark |

|---|---|

| Royal Dutch Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2006 | — | 5,000 | Proof |

Historical background

In 2006, Latvia was in a period of robust economic expansion, often referred to as the "Baltic Tiger" boom, with GDP growth exceeding 10%. This growth was fueled by massive foreign investment, easy credit, and a surge in domestic consumption. However, this prosperity came with significant underlying strains, primarily a rapidly growing current account deficit that exceeded 20% of GDP, one of the highest in the world. This deficit signaled that the nation was consuming far more than it produced, relying heavily on foreign capital inflows, which created vulnerability to a sudden shift in investor sentiment.

The currency situation was defined by Latvia's fixed exchange rate regime, established in 1994. The Latvian lats (LVL) was pegged to the Special Drawing Right (SDR), a basket of major currencies, but was effectively anchored to the euro as part of the country's official strategy to eventually join the Eurozone. This peg provided stability and was a cornerstone of monetary policy, but it also limited the central bank's options. With inflation rising sharply (reaching over 6% by year's end) due to the overheating economy, the Bank of Latvia could not use interest rate adjustments to cool demand, as higher rates would only attract more speculative capital inflows, exacerbating the imbalances.

Consequently, by late 2006, economists and international institutions like the IMF were issuing strong warnings about the sustainability of Latvia's economic trajectory. The fixed exchange rate, combined with high wage growth and rising prices, was leading to a severe loss of competitiveness. The situation was a classic precursor to a "hard landing," setting the stage for the profound crisis that would erupt in 2008 when the global financial freeze triggered the capital flight and deep recession that the 2006 imbalances had made inevitable.

The currency situation was defined by Latvia's fixed exchange rate regime, established in 1994. The Latvian lats (LVL) was pegged to the Special Drawing Right (SDR), a basket of major currencies, but was effectively anchored to the euro as part of the country's official strategy to eventually join the Eurozone. This peg provided stability and was a cornerstone of monetary policy, but it also limited the central bank's options. With inflation rising sharply (reaching over 6% by year's end) due to the overheating economy, the Bank of Latvia could not use interest rate adjustments to cool demand, as higher rates would only attract more speculative capital inflows, exacerbating the imbalances.

Consequently, by late 2006, economists and international institutions like the IMF were issuing strong warnings about the sustainability of Latvia's economic trajectory. The fixed exchange rate, combined with high wage growth and rising prices, was leading to a severe loss of competitiveness. The situation was a classic precursor to a "hard landing," setting the stage for the profound crisis that would erupt in 2008 when the global financial freeze triggered the capital flight and deep recession that the 2006 imbalances had made inevitable.

💎 Extremely Rare