½ satang – Thailand

Add to wishlist

Thailand

Context

Year: 1937

Thai Year:: 2480

Issuer: Thailand

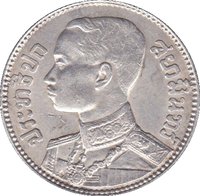

Ruler: Ananda Mahidol

Currency:

(since 1897)

Demonetized: Yes

Total mintage: 12,086,000

Material

Diameter: 19 mm

Weight: 1.8 g

Shape: Round with a round hole

Composition: Bronze

Magnetic: No

Technique: Milled

Alignment: Coin alignment

flip

References

Y: #

Numista: #12236

Value

Exchange value: 0.005 THB

Obverse

Reverse

Edge

Plain

Mints

| Name | Mark |

|---|---|

| Japan Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1937 | — | 12,086,000 |

Historical background

In 1937, Thailand (then known as Siam) operated under a unique and sophisticated managed currency system centered on the Baht, which was pegged to a fixed weight of pure silver. This system, however, was under significant strain. The global economic landscape was dominated by the Gold Standard, and the dramatic fall in the international price of silver during the Great Depression created serious imbalances. While the silver-pegged Baht made Thai exports cheap and competitive, it also led to a massive outflow of physical silver coins as they were melted down for their higher bullion value abroad, threatening the kingdom's monetary base.

Recognizing this vulnerability, King Rama VIII's government, under the financial leadership of Prince Wiwatthanachai Chaiyant, embarked on a decisive reform. In April 1937, the government announced the demonetization of old silver bullet coins and introduced a new, fiduciary currency. Crucially, the Baht was officially de-linked from silver and pegged instead to a basket of currencies, primarily the British Pound Sterling, at a rate of 11 Baht to 1 GBP. This shift from a metallic to a foreign exchange standard was a monumental policy change, moving Thailand into the modern era of central banking and managed exchange rates.

This reform successfully stabilized the currency, ended the silver hemorrhage, and provided the government with greater control over monetary policy on the eve of World War II. The new system, administered by the recently established Bank of Thailand (founded in 1942 but with its preparatory work underway), insulated the economy from volatile silver prices and aligned it more closely with its major trading partners. Thus, 1937 stands as a pivotal year marking Thailand's deliberate and strategic transition away from a centuries-old silver-based system to a managed paper currency integrated into the global financial order.

Recognizing this vulnerability, King Rama VIII's government, under the financial leadership of Prince Wiwatthanachai Chaiyant, embarked on a decisive reform. In April 1937, the government announced the demonetization of old silver bullet coins and introduced a new, fiduciary currency. Crucially, the Baht was officially de-linked from silver and pegged instead to a basket of currencies, primarily the British Pound Sterling, at a rate of 11 Baht to 1 GBP. This shift from a metallic to a foreign exchange standard was a monumental policy change, moving Thailand into the modern era of central banking and managed exchange rates.

This reform successfully stabilized the currency, ended the silver hemorrhage, and provided the government with greater control over monetary policy on the eve of World War II. The new system, administered by the recently established Bank of Thailand (founded in 1942 but with its preparatory work underway), insulated the economy from volatile silver prices and aligned it more closely with its major trading partners. Thus, 1937 stands as a pivotal year marking Thailand's deliberate and strategic transition away from a centuries-old silver-based system to a managed paper currency integrated into the global financial order.

Series: Unalom - Chakra series

🌱 Fairly Common