25 centimos – Costa Rica

Add to wishlist

Costa Rica

Context

Years: 1967–1978

Issuer: Costa Rica

Issuing organization: Central Bank of Costa Rica

Period:

(since 1948)

Currency:

(since 1896)

Demonetized: Yes

Total mintage: 38,005,000

Material

References

KM: #

Numista: #954

Value

Exchange value: 0.25 CRC

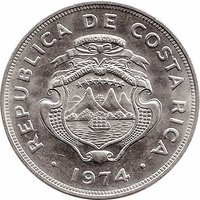

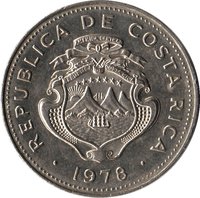

Obverse

Description:

Costa Rica's coat of arms features seven stars for its provinces, three volcanoes for its mountain ranges, two ships for its position between oceans, and a sunrise.

Inscription:

REPUBLICA DE COSTA RICA

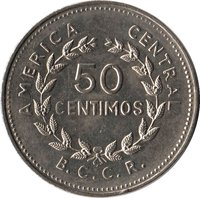

AMERICA CENTRAL

REPUBLICA DE COSTA RICA

• 1974 •

AMERICA CENTRAL

REPUBLICA DE COSTA RICA

• 1974 •

Translation:

REPUBLIC OF COSTA RICA

CENTRAL AMERICA

REPUBLIC OF COSTA RICA

• 1974 •

CENTRAL AMERICA

REPUBLIC OF COSTA RICA

• 1974 •

Script: Latin

Language: Spanish

Reverse

Edge

Plain with lettering.

Legend:

BCCR - BCCR - BCCR - BCCR -

Translation:

Victorious - Victorious - Victorious - Victorious -

Language: Arabic

Categories

| Symbols> Coat of Arms |

| Symbol> Wreath |

Mints

| Name | Mark |

|---|---|

| Casa de Moneda de Chile | — |

| Casa de Moneda de Guatemala | — |

| Royal Mint (Tower Hill) | — |

| United States Mint of Denver | — |

| VDM Metals / Vereinigte Deutsche Metallwerke | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1967 | — | 4,000,000 | ||

| 1970 | — | 4,000,000 | ||

| 1972 | — | 8,000,000 | ||

| 1974 | — | — | ||

| 1976 | — | 5,000 | Proof | |

| 1976 | — | 12,000,000 | ||

| 1978 | — | 10,000,000 |

Historical background

In 1967, Costa Rica's currency situation was characterized by a period of relative stability under a fixed exchange rate regime, but one that was underpinned by persistent economic pressures. The country operated with the colón, which was pegged to the U.S. dollar at a rate of 6.65 colones per dollar, a parity established in 1961. This fixed rate was maintained by the Central Bank of Costa Rica, created in 1950, which held sufficient international reserves to defend the peg and provide a sense of predictability for trade and investment during a time of significant export-led growth, primarily from coffee and bananas.

However, this stability was not without its challenges. The economy was susceptible to fluctuations in global commodity prices, and the government's expanding role in social programs and public infrastructure, while beneficial for development, began to strain public finances. A growing fiscal deficit, often financed by the Central Bank, created underlying inflationary pressures that were somewhat masked by the fixed exchange rate. This dynamic led to a gradual loss of competitiveness, as the colón's official value became increasingly overvalued relative to the country's economic fundamentals.

Consequently, 1967 fell within a calm before a significant monetary adjustment. The rigid peg and the mounting pressures would eventually prove unsustainable, leading Costa Rica to its first major devaluation in over a decade in 1974. Therefore, the currency situation in 1967 can be seen as one of managed equilibrium, where institutional mechanisms successfully maintained the external value of the colón in the short term, but could not indefinitely offset the structural economic imbalances that were building beneath the surface.

However, this stability was not without its challenges. The economy was susceptible to fluctuations in global commodity prices, and the government's expanding role in social programs and public infrastructure, while beneficial for development, began to strain public finances. A growing fiscal deficit, often financed by the Central Bank, created underlying inflationary pressures that were somewhat masked by the fixed exchange rate. This dynamic led to a gradual loss of competitiveness, as the colón's official value became increasingly overvalued relative to the country's economic fundamentals.

Consequently, 1967 fell within a calm before a significant monetary adjustment. The rigid peg and the mounting pressures would eventually prove unsustainable, leading Costa Rica to its first major devaluation in over a decade in 1974. Therefore, the currency situation in 1967 can be seen as one of managed equilibrium, where institutional mechanisms successfully maintained the external value of the colón in the short term, but could not indefinitely offset the structural economic imbalances that were building beneath the surface.

🌱 Very Common