50 centimos – Costa Rica

Add to wishlist

Costa Rica

Context

Years: 1965–1978

Issuer: Costa Rica

Issuing organization: Central Bank of Costa Rica

Period:

(since 1948)

Currency:

(since 1896)

Demonetized: Yes

Total mintage: 27,005,000

Material

References

KM: #

Numista: #2603

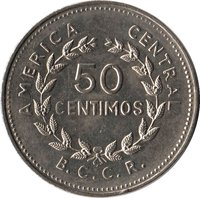

Value

Exchange value: 0.50 CRC

Obverse

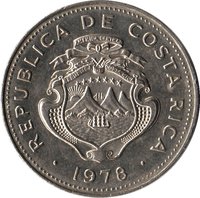

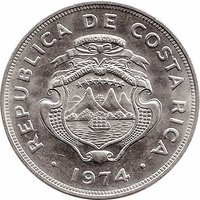

Description:

Costa Rica's coat of arms features seven stars for its provinces, three volcanoes for its mountain ranges, two ships for its position between oceans, and a sunrise.

Inscription:

REPUBLICA DE COSTA RICA

AMERICA CENTRAL

REPUBLICA DE COSTA RICA

1978

AMERICA CENTRAL

REPUBLICA DE COSTA RICA

1978

Translation:

REPUBLIC OF COSTA RICA

CENTRAL AMERICA

REPUBLIC OF COSTA RICA

1978

CENTRAL AMERICA

REPUBLIC OF COSTA RICA

1978

Script: Latin

Language: Spanish

Reverse

Edge

Categories

| Symbols> Coat of Arms |

| Geography> Mountain |

| Symbol> Wreath |

| Transportation> Watercraft |

Mints

| Name | Mark |

|---|---|

| Casa de Moneda de Guatemala | — |

| Royal Mint (Tower Hill) | — |

| Sherritt Mint | — |

| United States Mint of Philadelphia | — |

| VDM Metals / Vereinigte Deutsche Metallwerke | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1965 | — | 1,000,000 | ||

| 1968 | — | 2,000,000 | ||

| 1970 | — | 4,000,000 | ||

| 1972 | — | 4,000,000 | ||

| 1975 | — | — | ||

| 1976 | — | 6,000,000 | ||

| 1976 | — | 5,000 | Proof | |

| 1978 | — | 10,000,000 |

Historical background

In 1965, Costa Rica's currency situation was defined by a fixed exchange rate system, with the colón pegged to the U.S. dollar at a rate of 6.65 colones per dollar. This stability was managed by the Central Bank of Costa Rica (BCCR), established just over a decade prior in 1950, which held exclusive authority over currency issuance and foreign exchange policy. The peg provided a foundation for economic planning and international trade, but it also required careful management of foreign reserves to maintain the fixed parity, especially as the country's import-driven economy was vulnerable to external shocks.

The period was one of economic transition and moderate growth, following the transformative reforms of the 1940s. However, underlying pressures were evident. A persistent trade deficit, driven by imports of consumer goods, machinery, and petroleum, steadily eroded foreign exchange reserves. Furthermore, the government's fiscal policy, often running deficits to fund expanding public sector programs and infrastructure, contributed to inflationary pressures that the fixed rate struggled to fully contain. This created a subtle but growing tension between the official exchange rate and the currency's real purchasing power.

Consequently, while no major devaluation occurred in 1965 itself, the year existed within a period of mounting strain on the monetary system. The fixed rate, while nominally stable, was increasingly maintained through exchange and import controls rather than pure market confidence. These controls, alongside a growing black market for dollars, signaled the system's fragility. The pressures culminated just a few years later, leading to a significant devaluation in 1974 when the colón was adjusted to 8.57 per dollar, marking the end of the long-standing 6.65 parity and a new chapter of monetary adjustment.

The period was one of economic transition and moderate growth, following the transformative reforms of the 1940s. However, underlying pressures were evident. A persistent trade deficit, driven by imports of consumer goods, machinery, and petroleum, steadily eroded foreign exchange reserves. Furthermore, the government's fiscal policy, often running deficits to fund expanding public sector programs and infrastructure, contributed to inflationary pressures that the fixed rate struggled to fully contain. This created a subtle but growing tension between the official exchange rate and the currency's real purchasing power.

Consequently, while no major devaluation occurred in 1965 itself, the year existed within a period of mounting strain on the monetary system. The fixed rate, while nominally stable, was increasingly maintained through exchange and import controls rather than pure market confidence. These controls, alongside a growing black market for dollars, signaled the system's fragility. The pressures culminated just a few years later, leading to a significant devaluation in 1974 when the colón was adjusted to 8.57 per dollar, marking the end of the long-standing 6.65 parity and a new chapter of monetary adjustment.

🌱 Very Common