2 colones – Costa Rica

Add to wishlist

Costa Rica

Context

Years: 1968–1978

Issuer: Costa Rica

Issuing organization: Central Bank of Costa Rica

Period:

(since 1948)

Currency:

(since 1896)

Demonetized: Yes

Total mintage: 15,000,000

Material

References

KM: #

Numista: #3978

Value

Exchange value: 2 CRC

Obverse

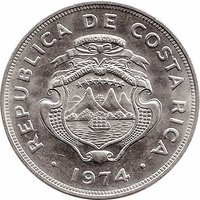

Description:

Costa Rica's coat of arms features seven stars for its provinces, three volcanoes for its mountain ranges, two ships for its position between the Atlantic and Pacific, and a sunrise.

Inscription:

REPUBLICA DE COSTA RICA

AMERICA CENTRAL

REPUBLICA DE COSTA RICA

. 1978 .

AMERICA CENTRAL

REPUBLICA DE COSTA RICA

. 1978 .

Translation:

REPUBLIC OF COSTA RICA

CENTRAL AMERICA

REPUBLIC OF COSTA RICA

. 1978 .

CENTRAL AMERICA

REPUBLIC OF COSTA RICA

. 1978 .

Script: Latin

Language: Spanish

Reverse

Edge

Categories

| Symbols> Coat of Arms |

| Symbol> Wreath |

Mints

| Name | Mark |

|---|---|

| Royal Mint (Tower Hill) | — |

| United States Mint of Philadelphia | — |

| VDM Metals / Vereinigte Deutsche Metallwerke | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1968 | — | 2,000,000 | ||

| 1970 | — | 1,000,000 | ||

| 1972 | — | 2,000,000 | ||

| 1978 | — | 10,000,000 |

Historical background

In 1968, Costa Rica's currency situation was characterized by a managed exchange rate system under the authority of the Central Bank of Costa Rica (BCCR), established in 1950. The country operated with a fixed but adjustable peg, primarily tying the colón to the US dollar. However, this system faced significant pressure due to persistent fiscal deficits and rising inflation. The government's expansionary spending, partly financed by central bank credit, led to a growing imbalance between the official exchange rate and economic fundamentals, creating a overvalued colón that hampered exports and encouraged capital flight.

This overvaluation fostered a thriving black market for US dollars, where the colón traded at a considerable discount compared to the official rate. This dual-market reality created distortions, disadvantaging official exporters like coffee and banana producers who received undervalued colón for their dollar earnings, while benefiting importers and those with access to preferential official rates. The situation reflected a classic currency crisis in the making, where the fixed rate became increasingly unsustainable without strict capital controls or a painful fiscal adjustment.

The tensions of 1968 culminated in a major devaluation the following year. In November 1969, the government, under President José Joaquín Trejos Fernández, was forced to abandon the longstanding peg of 6.65 colones per dollar and devalued the currency to 8.57 per dollar—a nearly 30% adjustment. While the decisive action occurred in 1969, the economic pressures and policy debates throughout 1968 directly set the stage for this pivotal monetary event, which aimed to restore balance of payments stability and align the currency with its true market value.

This overvaluation fostered a thriving black market for US dollars, where the colón traded at a considerable discount compared to the official rate. This dual-market reality created distortions, disadvantaging official exporters like coffee and banana producers who received undervalued colón for their dollar earnings, while benefiting importers and those with access to preferential official rates. The situation reflected a classic currency crisis in the making, where the fixed rate became increasingly unsustainable without strict capital controls or a painful fiscal adjustment.

The tensions of 1968 culminated in a major devaluation the following year. In November 1969, the government, under President José Joaquín Trejos Fernández, was forced to abandon the longstanding peg of 6.65 colones per dollar and devalued the currency to 8.57 per dollar—a nearly 30% adjustment. While the decisive action occurred in 1969, the economic pressures and policy debates throughout 1968 directly set the stage for this pivotal monetary event, which aimed to restore balance of payments stability and align the currency with its true market value.

🌱 Very Common