5 Taka – Bangladesh

Standard circulation coins

Commemoration: Jamuna Bridge

Bangladesh

Context

Years: 2005–2008

Issuer: Bangladesh

Issuing organization: Bangladesh Bank

Period:

(since 1971)

Currency:

(since 1972)

Material

Diameter: 26.8 mm

Weight: 8.17 g

Thickness: 2 mm

Shape: Dodecagonal

Composition: Stainless steel

Technique: Milled

References

KM: #Click to copy to clipboard26.1-26.3

Numista: #9355

Value

Exchange value: 5 BDT

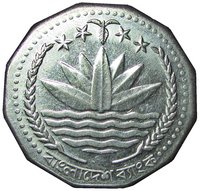

Obverse

Description:

Water lily (national emblem) flanked by rice sheaves. Above, three tea leaves separate four stars.

Inscription:

বাংলাদেশ ব্যাংক

Translation:

Bangladesh Bank

Language: Bengali

Reverse

Description:

Jamuna Bridge over water under cloudy skies. The bridge's Bangla name is above, with its date and value in figures and words in both English and Bangla.

Inscription:

যমুনা বহুমুখী সেতু

২০০৮

FIVE TAKA ৫ পাঁচ টাকা

২০০৮

FIVE TAKA ৫ পাঁচ টাকা

Translation:

Yamuna Multi-Purpose Bridge

2008

FIVE TAKA 5 Five Taka

2008

FIVE TAKA 5 Five Taka

Edge

Plain

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2005 | — | — | ||

| 2006 | — | — | ||

| 2008 | — | — |

Historical background

In 2005, Bangladesh's currency, the Taka (BDT), operated under a managed floating exchange rate system, a framework adopted in 2003 after moving away from a pegged regime. The Bangladesh Bank (the central bank) actively intervened in the foreign exchange market to curb excessive volatility, primarily targeting stability against the US Dollar. This period was characterized by a general trend of gradual depreciation of the Taka, driven by a persistent trade deficit and higher import payments compared to export earnings and remittance inflows. However, the depreciation was managed and relatively mild, as the central bank utilized its foreign exchange reserves to smooth out sharp fluctuations.

The macroeconomic context was one of cautious optimism. Remittances from Bangladeshis working abroad, a critical source of foreign currency, were showing strong and steady growth, providing a vital counterbalance to the trade gap. Furthermore, the ready-made garment (RMG) export sector was expanding robustly, bolstering export earnings. Despite these positive inflows, pressure on the Taka remained due to the high demand for dollars to finance imports of essential goods like petroleum, machinery, and food grains. Inflation was a growing concern, hovering around 7%, which limited the central bank's ability to use interest rate adjustments aggressively without risking further price increases.

Overall, the currency situation in 2005 was stable but under watchful management. The Bangladesh Bank successfully maintained orderly market conditions without a sharp devaluation, building a buffer of foreign exchange reserves that would prove crucial in the following years. The key challenges were structural: managing the balance of payments, controlling inflation, and fostering export diversification to reduce the underlying pressure on the Taka, all within a framework of gradual economic liberalization.

The macroeconomic context was one of cautious optimism. Remittances from Bangladeshis working abroad, a critical source of foreign currency, were showing strong and steady growth, providing a vital counterbalance to the trade gap. Furthermore, the ready-made garment (RMG) export sector was expanding robustly, bolstering export earnings. Despite these positive inflows, pressure on the Taka remained due to the high demand for dollars to finance imports of essential goods like petroleum, machinery, and food grains. Inflation was a growing concern, hovering around 7%, which limited the central bank's ability to use interest rate adjustments aggressively without risking further price increases.

Overall, the currency situation in 2005 was stable but under watchful management. The Bangladesh Bank successfully maintained orderly market conditions without a sharp devaluation, building a buffer of foreign exchange reserves that would prove crucial in the following years. The key challenges were structural: managing the balance of payments, controlling inflation, and fostering export diversification to reduce the underlying pressure on the Taka, all within a framework of gradual economic liberalization.

🌱 Common