1 Peso – Cuba

Circulating commemorative coins

Commemoration: José Martí

Cuba

Obverse

Description:

Design from Cuba's coat of arms: sun over sea with key. Country name above, "Patria y Libertad" below. Face value under image, weight and fineness between value and motto.

Inscription:

REPUBLICA DE CUBA

1 PESO

26.7295 G. 900M.

PATRIA Y LIBERTAD

1 PESO

26.7295 G. 900M.

PATRIA Y LIBERTAD

Translation:

REPUBLIC OF CUBA

1 PESO

26.7295 G. .900 FINE.

HOMELAND AND LIBERTY

1 PESO

26.7295 G. .900 FINE.

HOMELAND AND LIBERTY

Script: Latin

Language: Spanish

Engraver: Esteban Valderrama Peña

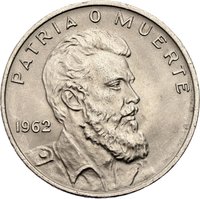

Reverse

Description:

Portrait of Cuban hero José Martí (1853-1895) with a sparkling star; circular legend above, dates on sides.

Inscription:

1853 • CENTENARIO DE MARTI • 1953

Translation:

1853 • CENTENARY OF MARTI • 1953

Script: Latin

Language: Spanish

Engraver: Esteban Valderrama Peña

Edge

Reeded

Categories

| Animal> Bird |

| Person> Politician |

Mints

| Name | Mark |

|---|---|

| United States Mint of Philadelphia | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1953 | — | 1,000,000 | ||

| 1953 | — | — | Proof |

Historical background

In 1953, Cuba's currency situation was characterized by stability and full integration into the U.S. dollar sphere, a legacy of the island's deep economic dependence on its northern neighbor. Since the early 20th century, the Cuban peso (CUP) had been pegged at a one-to-one parity with the U.S. dollar, a policy formalized in 1934. This fixed exchange rate, backed by substantial gold and dollar reserves, facilitated predictable trade and investment, primarily in the dominant sugar industry. U.S. dollars circulated freely alongside national currency, and Cuba's financial system was effectively an extension of Wall Street, with major banks and a significant portion of the economy under American control.

This monetary stability, however, existed within a context of profound social inequality and political corruption under the dictatorship of Fulgencio Batista. The economy was overwhelmingly oriented toward sugar exports to the United States, making it vulnerable to global price fluctuations. While the currency itself was strong, the benefits of this stable system were concentrated in the hands of a wealthy elite and foreign interests, with widespread poverty, unemployment, and landlessness afflicting much of the rural and urban working class. The financial facade of stability, therefore, masked the deep structural fractures in Cuban society.

The year 1953 itself was a pivotal turning point, not for a currency crisis, but for the political upheaval that would ultimately dismantle this entire economic order. On July 26th, Fidel Castro led the failed attack on the Moncada Barracks, an event that ignited the revolutionary movement. While the currency regime remained unchanged that year, the revolution's eventual success in 1959 would lead to the radical restructuring of Cuba's financial system, including the severing of the dollar peg, the nationalization of banks, and the creation of a state-controlled, isolated currency system—the direct antithesis of the dollar-dependent model of 1953.

This monetary stability, however, existed within a context of profound social inequality and political corruption under the dictatorship of Fulgencio Batista. The economy was overwhelmingly oriented toward sugar exports to the United States, making it vulnerable to global price fluctuations. While the currency itself was strong, the benefits of this stable system were concentrated in the hands of a wealthy elite and foreign interests, with widespread poverty, unemployment, and landlessness afflicting much of the rural and urban working class. The financial facade of stability, therefore, masked the deep structural fractures in Cuban society.

The year 1953 itself was a pivotal turning point, not for a currency crisis, but for the political upheaval that would ultimately dismantle this entire economic order. On July 26th, Fidel Castro led the failed attack on the Moncada Barracks, an event that ignited the revolutionary movement. While the currency regime remained unchanged that year, the revolution's eventual success in 1959 would lead to the radical restructuring of Cuba's financial system, including the severing of the dollar peg, the nationalization of banks, and the creation of a state-controlled, isolated currency system—the direct antithesis of the dollar-dependent model of 1953.

🌱 Common