1 pie – Bombay Presidency

Add to wishlist

India

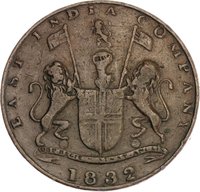

Obverse

Description:

East India Company coat of arms. The ribbon reads "Auspicio Regis Et Senatus Anglia," with the date below and value (Pie) above, all within a plain raised rim.

Inscription:

PIE

AUSP:REGIS & SENAT:ANG

1831

AUSP:REGIS & SENAT:ANG

1831

Translation:

By the Auspices of the King and the Senate of England

1831

1831

Language: Latin

Reverse

Edge

Plain

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1831 | — | — |

Historical background

In 1831, the Bombay Presidency was grappling with a complex and chaotic currency system, a legacy of its diverse political history and trade networks. The region was not yet under a uniform British coinage; instead, it operated with a multitude of circulating mediums. The most prominent were the silver rupee of the Mughal Empire and its local derivatives, alongside the gold hun (or pagoda) prevalent in the southern districts. Furthermore, a vast quantity of silver coins from other Indian princely states, Spanish and Mexican dollars (popular in international trade), and even old Portuguese coins circulated freely, creating a bewildering environment for commerce.

This multiplicity led to severe practical problems. Exchange rates between gold, silver, and copper coins fluctuated wildly by district and even by merchant, causing confusion, transaction delays, and rampant fraud. The British East India Company's own silver rupee, minted in Bombay, competed for authority amidst this medley. The absence of a standardised, trusted currency hampered revenue collection, complicated army payments, and stifled the growing commercial ambitions of the Presidency, particularly in its burgeoning port city of Bombay.

Consequently, 1831 fell within a period of intense administrative focus on currency reform. The Presidency authorities were actively working towards simplification and control, a process that would culminate in the Coinage Act of 1835. The key objective was to replace the myriad systems with a single, uniform silver standard based on the Company's rupee, thereby centralising monetary authority, stabilising the economy, and facilitating the integration of the Bombay Presidency into a broader imperial trading system. Thus, the situation in 1831 was one of transition, marked by disorder but moving decisively towards standardisation under Company rule.

This multiplicity led to severe practical problems. Exchange rates between gold, silver, and copper coins fluctuated wildly by district and even by merchant, causing confusion, transaction delays, and rampant fraud. The British East India Company's own silver rupee, minted in Bombay, competed for authority amidst this medley. The absence of a standardised, trusted currency hampered revenue collection, complicated army payments, and stifled the growing commercial ambitions of the Presidency, particularly in its burgeoning port city of Bombay.

Consequently, 1831 fell within a period of intense administrative focus on currency reform. The Presidency authorities were actively working towards simplification and control, a process that would culminate in the Coinage Act of 1835. The key objective was to replace the myriad systems with a single, uniform silver standard based on the Company's rupee, thereby centralising monetary authority, stabilising the economy, and facilitating the integration of the Bombay Presidency into a broader imperial trading system. Thus, the situation in 1831 was one of transition, marked by disorder but moving decisively towards standardisation under Company rule.

✨ Legendary