250 Escudos – Portugal

Portugal

Context

Year: 1988

Issuer: Portugal

Period:

(since 1974)

Currency:

(1911—2001)

Demonetized: Yes

Total mintage: 850,000

Material

Diameter: 37 mm

Weight: 23.1 g

Thickness: 2.6 mm

Shape: Round

Composition: Copper-nickel

Technique: Milled

Alignment: Coin alignment

flip

References

KM: #Click to copy to clipboard643

Numista: #8951

Value

Exchange value: 250 PTE

Inflation-adjusted value: 943.77 PTE

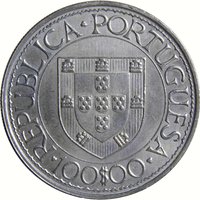

Obverse

Description:

Shield before floral pattern.

Inscription:

REPUBLICA PORTUGUESA

250 ESC.

250 ESC.

Translation:

Portuguese Republic

250 Escudos

250 Escudos

Script: Latin

Language: Portuguese

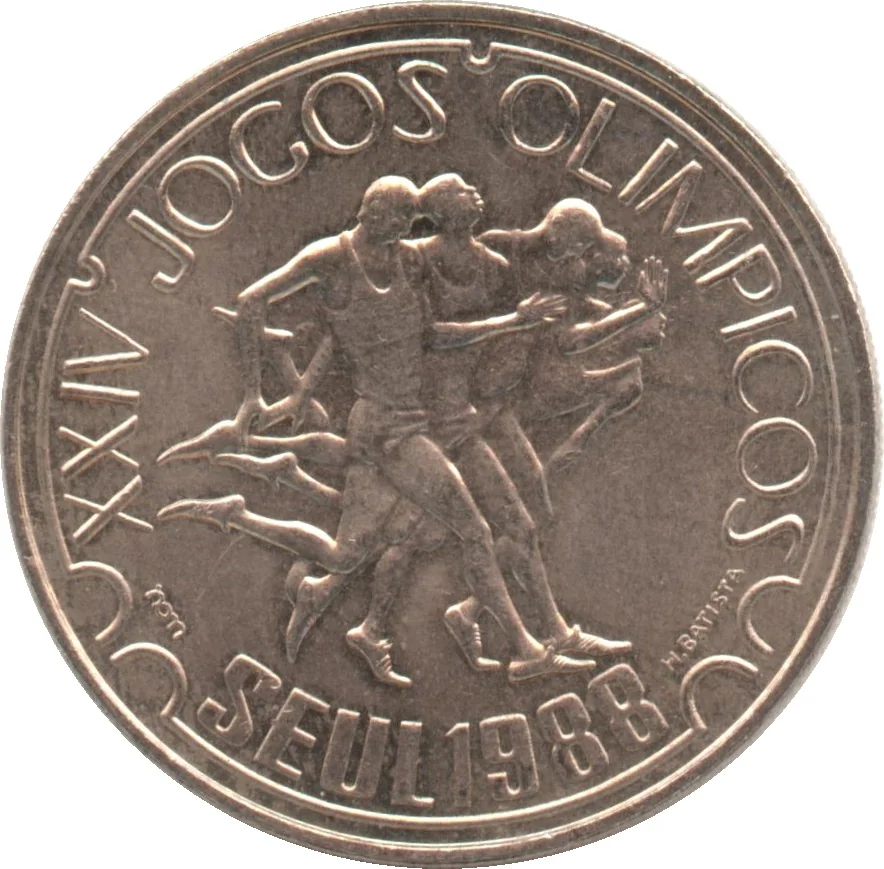

Engraver: Hélder Batista

Reverse

Edge

Reeded

Categories

| Symbols> Coat of Arms |

| Sport> Summer Olympic Games |

Mints

| Name | Mark |

|---|---|

| Imprensa Nacional - Casa da Moeda | INCM |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1988 | — | 850,000 |

Historical background

In 1988, Portugal's currency situation was defined by its ongoing integration into the European Monetary System (EMS) and the management of the escudo within that framework. Having joined the EMS in April 1992, Portugal operated within the Exchange Rate Mechanism (ERM), which required maintaining the escudo's value within agreed fluctuation bands against other member currencies, primarily the Deutsche Mark. This commitment served as a key anchor for monetary policy, aimed at curbing the high inflation that had plagued the country following the 1974 revolution, and signaled Portugal's serious intent to converge with core European economies.

Domestically, the Banco de Portugal pursued a tight monetary policy to support the escudo's parity and further disinflation. This period was characterized by high interest rates, which helped stabilize the currency but also posed challenges for economic growth and investment. The escudo was subject to periodic devaluations within the EMS (notably in 1986 and 1990) to correct for competitiveness gaps and inflation differentials with stronger-currency partners like Germany. These adjustments were strategic, allowing for necessary economic corrections while maintaining the overall discipline of the fixed-exchange-rate system.

The broader context was Portugal's preparation for deeper European integration, following its accession to the European Economic Community in 1986. The currency policy of 1988 was therefore not an isolated effort but a crucial phase in a longer-term strategy to achieve macroeconomic stability and qualify for future participation in a single European currency. The management of the escudo during this time was fundamentally about building credibility, controlling inflation, and aligning the national economy with the convergence criteria that would later be formalized in the Maastricht Treaty.

Domestically, the Banco de Portugal pursued a tight monetary policy to support the escudo's parity and further disinflation. This period was characterized by high interest rates, which helped stabilize the currency but also posed challenges for economic growth and investment. The escudo was subject to periodic devaluations within the EMS (notably in 1986 and 1990) to correct for competitiveness gaps and inflation differentials with stronger-currency partners like Germany. These adjustments were strategic, allowing for necessary economic corrections while maintaining the overall discipline of the fixed-exchange-rate system.

The broader context was Portugal's preparation for deeper European integration, following its accession to the European Economic Community in 1986. The currency policy of 1988 was therefore not an isolated effort but a crucial phase in a longer-term strategy to achieve macroeconomic stability and qualify for future participation in a single European currency. The management of the escudo during this time was fundamentally about building credibility, controlling inflation, and aligning the national economy with the convergence criteria that would later be formalized in the Maastricht Treaty.

Series: System 1981-2001

🌱 Very Common