20 kroner (Norges Bank) – Norway

Add to wishlist

Circulating commemorative coins

Commemoration: Norges Bank Bicentenary

Norway

Context

Material

References

KM: #

Numista: #89253

Value

Exchange value: 20 NOK

Inflation-adjusted value: 27.20 NOK

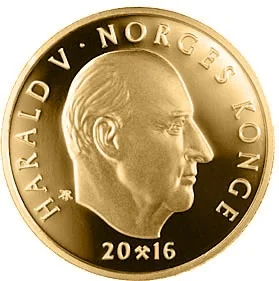

Obverse

Description:

Bust of King Harald V facing right, with engraver's initials behind it. Inscription surrounds the bust, and a mintmark divides the date below. Solid ring on the rim.

Inscription:

HARALD V · NORGES KONGE

IAR

20 ⚒ 16

IAR

20 ⚒ 16

Translation:

HARALD V · NORWAY'S KING

IAR

20 ⚒ 16

IAR

20 ⚒ 16

Script: Latin

Engraver: Ingrid Austlid Rise

Reverse

Description:

Norwegian inflation and deflation history. Value above. Designer initials left. Two-line inscription bottom right. Solid rim ring.

Inscription:

20 KR

KA

NORGES BANK

200 ÅR

KA

NORGES BANK

200 ÅR

Translation:

20 KR

KA

NORGES BANK

200 YEARS

KA

NORGES BANK

200 YEARS

Script: Latin

Engraver: Ingrid Austlid Rise

Designer: Kjersti M. Austdal

Edge

Plain

Mints

| Name | Mark |

|---|---|

| Norwegian Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2016 | — | 1,955,000 | ||

| 2016 | — | 3,450 | Proof |

Historical background

In 2016, Norway's currency situation was dominated by the prolonged downturn in global oil prices, which began in mid-2014. As a major petroleum exporter, Norway's economy and its currency, the krone (NOK), are highly sensitive to oil price movements. Throughout 2016, Brent crude traded at historically low levels, averaging around $45 per barrel, which significantly reduced national export revenues and government income. This sustained pressure led to a notably weak krone, which traded at multi-year lows against both the euro and the US dollar, benefiting non-oil exporters but increasing import costs and household expenses.

In response, Norges Bank, the country's central bank, maintained an expansionary monetary policy to cushion the economic slowdown. The key policy rate was cut twice in 2016, reaching a historic low of 0.5% by year's end. This rate-cutting cycle, which began in late 2014, aimed to stimulate domestic demand and counter rising unemployment, particularly in oil-related industries. However, the low rates also contributed to keeping the krone weak, as they reduced the currency's yield appeal for international investors.

Despite the oil sector slump, Norway's economic fundamentals remained robust compared to many other nations, supported by its massive sovereign wealth fund (the Government Pension Fund Global). The weak krone provided a substantial boost to other export-oriented sectors like tourism, seafood, and manufacturing, helping to diversify the economy. Consequently, while 2016 was a period of significant adjustment and currency weakness, it also highlighted the Norwegian economy's underlying resilience and its structured response to terms-of-trade shocks.

In response, Norges Bank, the country's central bank, maintained an expansionary monetary policy to cushion the economic slowdown. The key policy rate was cut twice in 2016, reaching a historic low of 0.5% by year's end. This rate-cutting cycle, which began in late 2014, aimed to stimulate domestic demand and counter rising unemployment, particularly in oil-related industries. However, the low rates also contributed to keeping the krone weak, as they reduced the currency's yield appeal for international investors.

Despite the oil sector slump, Norway's economic fundamentals remained robust compared to many other nations, supported by its massive sovereign wealth fund (the Government Pension Fund Global). The weak krone provided a substantial boost to other export-oriented sectors like tourism, seafood, and manufacturing, helping to diversify the economy. Consequently, while 2016 was a period of significant adjustment and currency weakness, it also highlighted the Norwegian economy's underlying resilience and its structured response to terms-of-trade shocks.

🌱 Common