20 kroner (First Sami Congress) – Norway

Add to wishlist

Circulating commemorative coins

Commemoration: 100th Anniversary of the First Sami Congress

Norway

Context

Material

References

KM: #

Numista: #107326

Value

Exchange value: 20 NOK

Inflation-adjusted value: 26.27 NOK

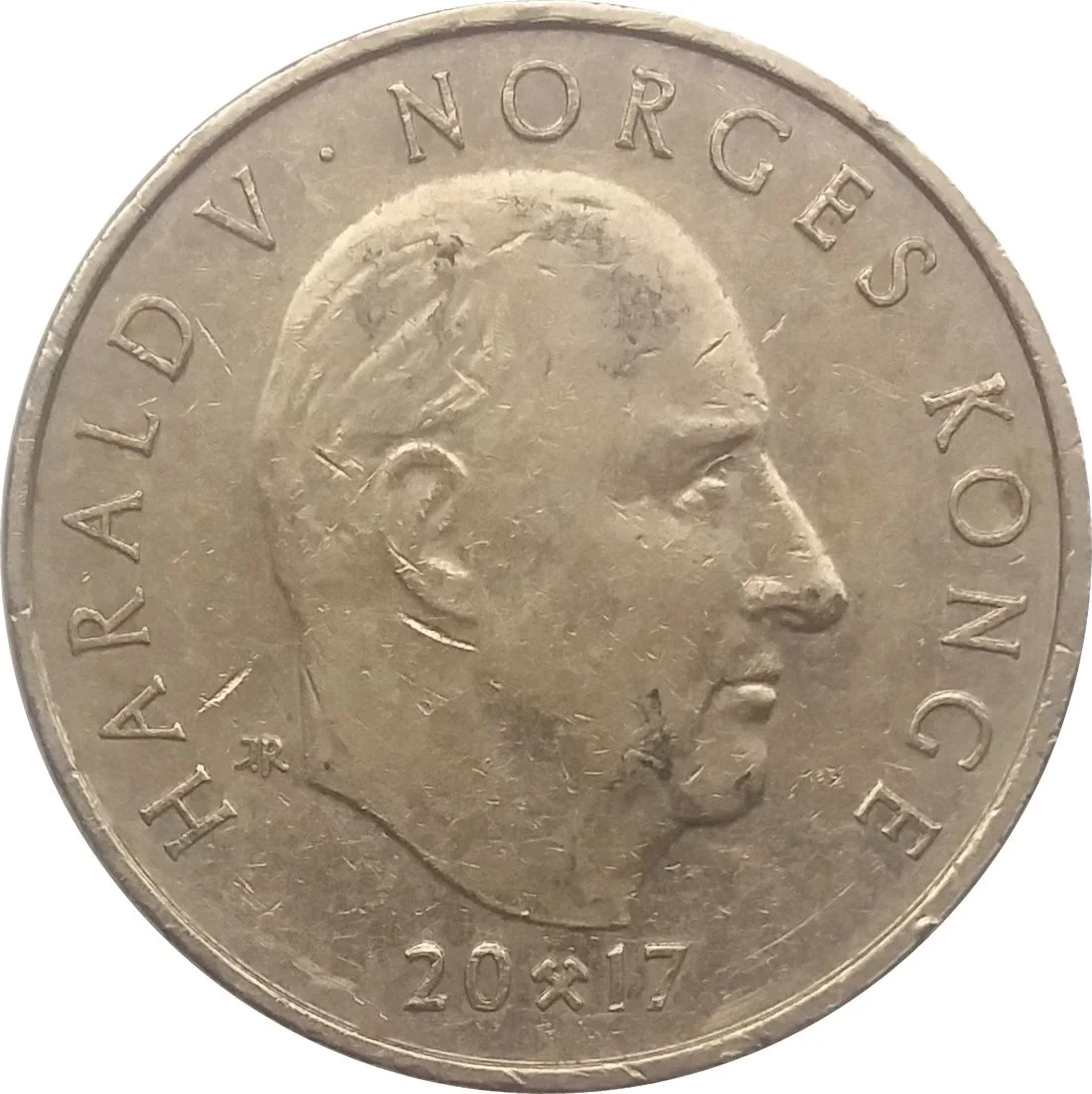

Obverse

Description:

Bust of King Harald V facing right, with engraver's initials behind it. Inscription surrounds the bust, and a mintmark divides the date below. Solid ring on the rim.

Inscription:

HARALD V · NORGES KONGE

IAR

20 ⚒ 17

IAR

20 ⚒ 17

Translation:

Harald V, Norway's King

IAR

20 17

IAR

20 17

Script: Latin

Engraver: Ingrid Austlid Rise

Reverse

Description:

Sami mythological symbols and ceremonial drum center. Left: value. Designer initials below symbols. Inscription bottom right. Solid rim ring.

Inscription:

KRONER 20

AJ

TRÅANTE 1917-2017

AJ

TRÅANTE 1917-2017

Translation:

Twenty Kroner

AJ

Trondheim 1917-2017

AJ

Trondheim 1917-2017

Script: Latin

Engraver: Ingrid Austlid Rise

Designer: Annelise Josefsen

Edge

Plain

Categories

| Mythology |

Mints

| Name | Mark |

|---|---|

| Norwegian Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2017 | — | 2,042,000 | ||

| 2017 | — | 2,450 | Proof |

Historical background

In 2017, Norway's currency situation was characterized by a period of relative stability and gradual strengthening for the Norwegian krone (NOK), though it remained historically weak compared to pre-2014 levels. The primary driver was a recovering oil market, with Brent crude prices climbing from an average of $45 per barrel in 2016 to over $54 in 2017. As a petroleum-based economy, this uplift improved the nation's trade balance and fiscal outlook, providing fundamental support for the krone. However, the currency's appreciation was tempered by the Norges Bank's persistently low interest rate, held at a record-low 0.5% for most of the year to support an economy still adjusting to the earlier oil price shock.

Monetary policy was a key focal point, with the central bank carefully navigating between supporting domestic demand and preventing excessive krone weakness that could fuel inflation. Governor Øystein Olsen signaled a shift away from the highly accommodative stance, indicating that the next rate move would likely be up, but emphasized that this was a distant prospect. This cautious "forward guidance" kept a lid on rapid krone gains, as international investors found little immediate yield incentive. Consequently, while the NOK gained against the euro and dollar during the year, its recovery was measured.

The broader economic context featured a resilient mainland (non-oil) economy and rising house prices, which added complexity to the central bank's decisions. Internationally, the krone was also influenced by global risk sentiment and political events, but the dominant narrative remained domestic: a patient central bank managing a cautious normalization path amid improving, but not yet robust, petroleum sector revenues. This resulted in a krone that ended 2017 stronger than it began, yet still undervalued by long-term standards, reflecting a balanced but fragile post-crisis recovery.

Monetary policy was a key focal point, with the central bank carefully navigating between supporting domestic demand and preventing excessive krone weakness that could fuel inflation. Governor Øystein Olsen signaled a shift away from the highly accommodative stance, indicating that the next rate move would likely be up, but emphasized that this was a distant prospect. This cautious "forward guidance" kept a lid on rapid krone gains, as international investors found little immediate yield incentive. Consequently, while the NOK gained against the euro and dollar during the year, its recovery was measured.

The broader economic context featured a resilient mainland (non-oil) economy and rising house prices, which added complexity to the central bank's decisions. Internationally, the krone was also influenced by global risk sentiment and political events, but the dominant narrative remained domestic: a patient central bank managing a cautious normalization path amid improving, but not yet robust, petroleum sector revenues. This resulted in a krone that ended 2017 stronger than it began, yet still undervalued by long-term standards, reflecting a balanced but fragile post-crisis recovery.

🌱 Common