1 dollar – United States

Add to wishlist

Non-circulating coins

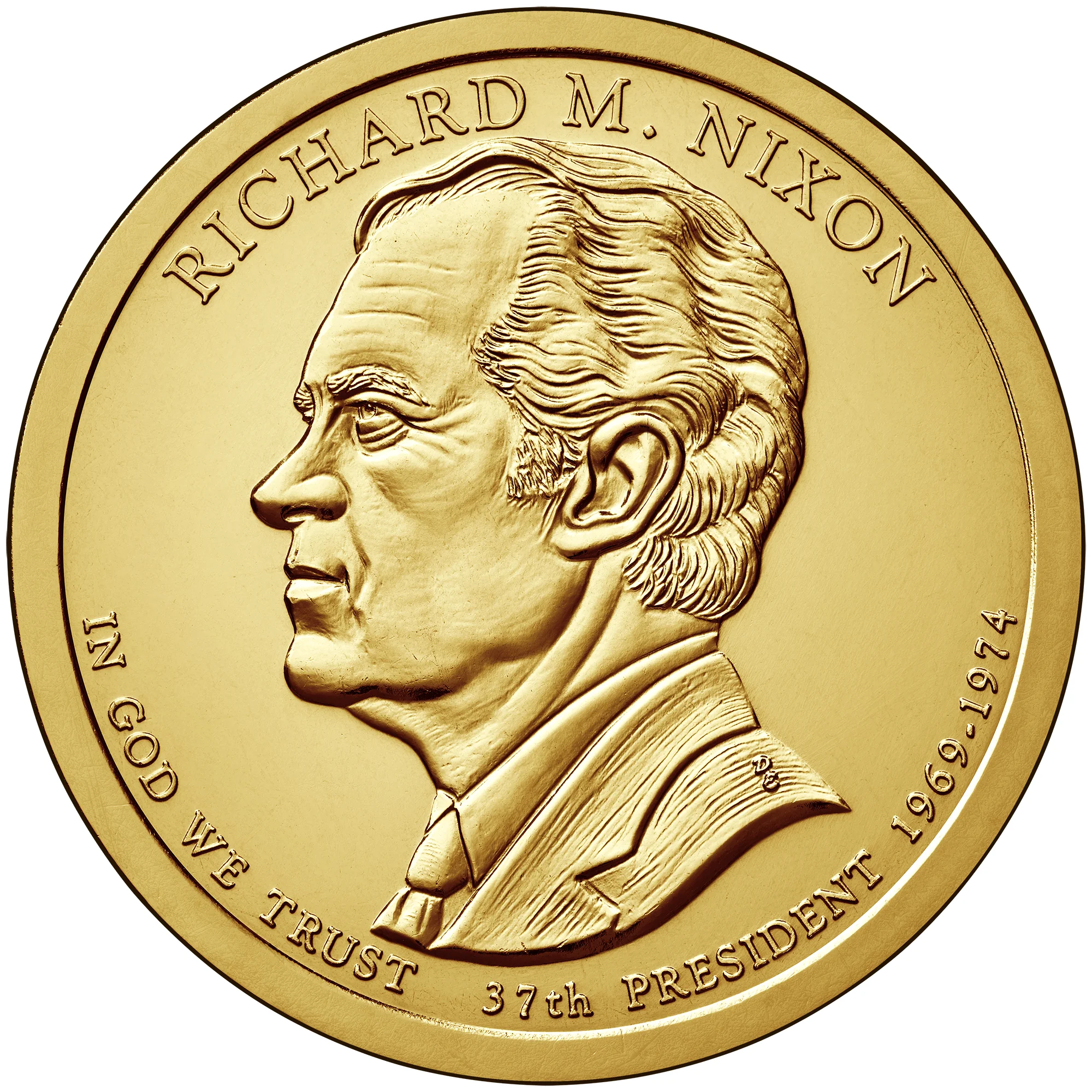

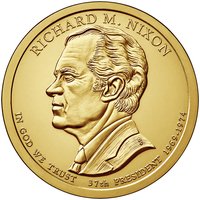

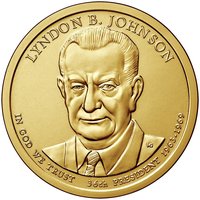

Commemoration: Richard M. Nixon - 37th President - 1969-1974

Series: Presidential $1 Coin Program

United States

Context

Year: 2016

Issuer: United States

Period:

(since 1776)

Currency:

(since 1785)

Total mintage: 9,800,000

Material

References

KM: #

Numista: #83826

Value

Exchange value: 1 USD = $1.00

Inflation-adjusted value: 1.35 USD

Obverse

Description:

Portrait of Richard M. Nixon

Inscription:

RICHARD M. NIXON

DE

IN GOD WE TRUST 37th PRESIDENT 1969-1974

DE

IN GOD WE TRUST 37th PRESIDENT 1969-1974

Script: Latin

Engraver: Don Everhart

Reverse

Description:

Lady Liberty reimagined.

Inscription:

UNITED STATES OF AMERICA

$1

DE

$1

DE

Script: Latin

Engraver: Don Everhart

Edge

Engraved with date and motto.

Legend:

E PLURIBUS UNUM

2016

2016

Categories

| Person> Politician |

Mints

| Name | Mark |

|---|---|

| United States Mint of Denver | D |

| United States Mint of Philadelphia | P |

| United States Mint of San Francisco | S |

Historical background

In 2016, the United States currency situation was characterized by a period of relative strength and stability for the U.S. dollar, underpinned by a diverging monetary policy path from other major economies. The Federal Reserve, having ended its quantitative easing program in 2014, was in a tightening cycle, raising the federal funds rate in December 2015 for the first time in nearly a decade and signaling further gradual hikes. This contrasted sharply with the European Central Bank and the Bank of Japan, which were still employing aggressive stimulus measures, making dollar-denominated assets more attractive and pushing the dollar's value higher on foreign exchange markets.

Domestically, the economy was in a sustained, though modest, expansion with low unemployment and contained inflation, which gave the Fed confidence to continue normalizing policy. However, this strong dollar presented a significant headwind for large U.S. multinational corporations, as it made American exports more expensive and reduced the value of overseas earnings when converted back to dollars. This dynamic contributed to an earnings recession in the S&P 500 for much of 2015 and into early 2016, creating a tension between the Fed's domestic objectives and the global financial environment.

The year was also dominated by significant political uncertainty, which introduced volatility into currency markets. The unexpected outcome of the Brexit referendum in June 2016 caused a sharp, temporary flight to the safety of the U.S. dollar and Treasury bonds. Furthermore, the contentious U.S. presidential election campaign, culminating in Donald Trump's victory in November, created waves of volatility. Markets initially reacted with a "risk-off" sell-off, but the dollar quickly rallied on anticipation of pro-growth policies, tax cuts, and infrastructure spending, ending the year near 14-year highs on a trade-weighted basis as investors priced in faster growth and higher interest rates.

Domestically, the economy was in a sustained, though modest, expansion with low unemployment and contained inflation, which gave the Fed confidence to continue normalizing policy. However, this strong dollar presented a significant headwind for large U.S. multinational corporations, as it made American exports more expensive and reduced the value of overseas earnings when converted back to dollars. This dynamic contributed to an earnings recession in the S&P 500 for much of 2015 and into early 2016, creating a tension between the Fed's domestic objectives and the global financial environment.

The year was also dominated by significant political uncertainty, which introduced volatility into currency markets. The unexpected outcome of the Brexit referendum in June 2016 caused a sharp, temporary flight to the safety of the U.S. dollar and Treasury bonds. Furthermore, the contentious U.S. presidential election campaign, culminating in Donald Trump's victory in November, created waves of volatility. Markets initially reacted with a "risk-off" sell-off, but the dollar quickly rallied on anticipation of pro-growth policies, tax cuts, and infrastructure spending, ending the year near 14-year highs on a trade-weighted basis as investors priced in faster growth and higher interest rates.

Series: Presidential $1 Coin Program

🌱 Common