½ Penny – Ireland

Ireland

Context

Material

Diameter: 27.6 mm

Weight: 7.64 g

Thickness: 1.5 mm

Shape: Round

Composition: Copper

Standard: Silver quarter ounce

Magnetic: No

Technique: Milled

Alignment: Coin alignment

flip

References

KM: #Click to copy to clipboard147

Numista: #8347

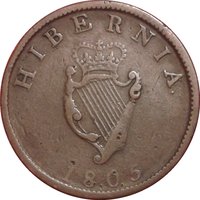

Obverse

Reverse

Edge

Engrailed with Center Slanted Reeding Left or Plain.

Mints

| Name | Mark |

|---|---|

| Soho Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1805 | — | — | ||

| 1805 | — | — | Proof |

Historical background

In 1805, Ireland operated under a complex and often unstable dual-currency system. The official currency was Irish pounds, shillings, and pence, which had a separate existence from British sterling, though the two were fixed at an exchange rate of 13 Irish pounds to 12 British pounds. This meant Irish currency was inherently discounted, creating persistent accounting complications and symbolic resentment, as it implied Irish economic subordination within the United Kingdom (established by the Acts of Union 1800).

The real circulating medium, however, was a chaotic mix of physical money. Alongside limited minted coin, a vast array of paper banknotes issued by numerous private and provincial banks was in wide circulation. These notes were promises to pay in specie (gold or silver), but their value was entirely dependent on the credibility of the issuing bank. This led to frequent fluctuations, localized shortages, and the risk of bank failures, which could render notes worthless. For everyday transactions, small change was so scarce that tokens issued by merchants and even counterfeit coins were commonly accepted out of necessity.

This fragile monetary environment existed against a backdrop of post-Union economic adjustment and the ongoing Napoleonic Wars. The wars strained British finances, leading to high taxes and inflation, pressures which were acutely felt in Ireland. The Bank of Ireland, established in 1783, acted as a quasi-central bank but lacked full control over the money supply. Consequently, in 1805, Ireland’s currency was not a unified symbol of sovereignty but a patchwork of instruments reflecting its politically integrated yet economically disjointed position within the wider British war economy.

The real circulating medium, however, was a chaotic mix of physical money. Alongside limited minted coin, a vast array of paper banknotes issued by numerous private and provincial banks was in wide circulation. These notes were promises to pay in specie (gold or silver), but their value was entirely dependent on the credibility of the issuing bank. This led to frequent fluctuations, localized shortages, and the risk of bank failures, which could render notes worthless. For everyday transactions, small change was so scarce that tokens issued by merchants and even counterfeit coins were commonly accepted out of necessity.

This fragile monetary environment existed against a backdrop of post-Union economic adjustment and the ongoing Napoleonic Wars. The wars strained British finances, leading to high taxes and inflation, pressures which were acutely felt in Ireland. The Bank of Ireland, established in 1783, acted as a quasi-central bank but lacked full control over the money supply. Consequently, in 1805, Ireland’s currency was not a unified symbol of sovereignty but a patchwork of instruments reflecting its politically integrated yet economically disjointed position within the wider British war economy.

🌱 Common