100 Livres – Lebanon

Lebanon

Context

Material

References

KM: #Click to copy to clipboard38a

Numista: #8329

Value

Exchange value: 100 LBP

Obverse

Description:

Arabic value, issuer, and date above a cedar tree.

Inscription:

مصرف لبنان

١٠٠

ليرة

٢٠٠٣

١٠٠

ليرة

٢٠٠٣

Translation:

Banque du Liban

100

Lira

2003

100

Lira

2003

Language: Arabic

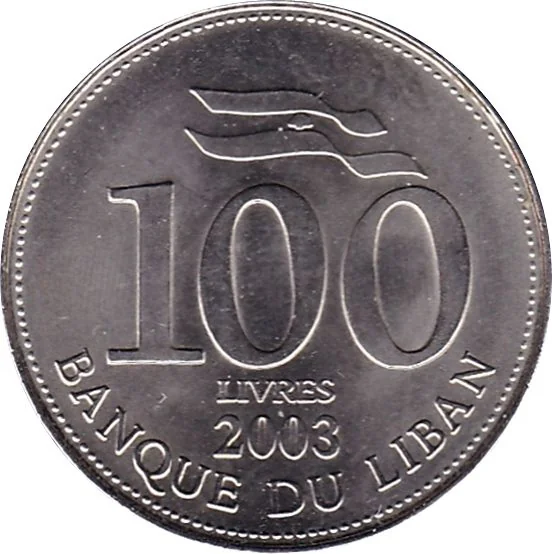

Reverse

Description:

Denomination, date, and issuer in Latin script beneath a stylized Lebanese flag.

Inscription:

100

LIVRES

2003

BANQUE DU LIBAN

LIVRES

2003

BANQUE DU LIBAN

Translation:

One Hundred

Pounds

2003

Bank of Lebanon

Pounds

2003

Bank of Lebanon

Language: French

Edge

Plain

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2003 | — | — |

Historical background

In 2003, Lebanon's currency situation was characterized by a fragile and artificial stability, underpinned by a longstanding fixed exchange rate peg. Since 1997, the Lebanese pound (LBP) had been officially pegged at 1,507.5 pounds to the US dollar, a policy maintained by the Banque du Liban (the central bank) through high-interest rates and substantial foreign currency reserves. This peg was a cornerstone of national economic policy following the civil war, intended to provide monetary stability and confidence. However, it masked underlying and growing vulnerabilities, including a massive public debt exceeding 180% of GDP, persistent budget deficits, and a stagnant economy burdened by corruption and inefficient state-owned enterprises.

The stability of the peg was increasingly dependent on continuous inflows of foreign capital, primarily through the central bank's financial engineering operations and diaspora remittances. These mechanisms were used to service the debt and defend the currency, creating a circular and unsustainable model. While the official rate held firm in 2003, economic stagnation and political uncertainty—exacerbated by the aftermath of the 2002 Paris II donor conference and the looming shadow of the 2005 assassination of former Prime Minister Rafic Hariri—began to erode confidence. A parallel foreign exchange market existed, and the spread between the official and market rates, though still narrow, was a telling indicator of mounting pressure on the national currency.

Consequently, 2003 represented the calm before the storm. The fundamental imbalances were widely recognized by economists and international institutions, who warned that the currency peg was unsustainable without deep fiscal reforms and economic growth. The government's inability to implement necessary austerity measures or stimulate the productive sector meant the country was effectively borrowing time. The entrenched stability of the pound in 2003 was therefore an increasingly expensive illusion, setting the stage for the severe financial crisis that would erupt more than a decade later, when the elaborate scheme to maintain the peg ultimately collapsed.

The stability of the peg was increasingly dependent on continuous inflows of foreign capital, primarily through the central bank's financial engineering operations and diaspora remittances. These mechanisms were used to service the debt and defend the currency, creating a circular and unsustainable model. While the official rate held firm in 2003, economic stagnation and political uncertainty—exacerbated by the aftermath of the 2002 Paris II donor conference and the looming shadow of the 2005 assassination of former Prime Minister Rafic Hariri—began to erode confidence. A parallel foreign exchange market existed, and the spread between the official and market rates, though still narrow, was a telling indicator of mounting pressure on the national currency.

Consequently, 2003 represented the calm before the storm. The fundamental imbalances were widely recognized by economists and international institutions, who warned that the currency peg was unsustainable without deep fiscal reforms and economic growth. The government's inability to implement necessary austerity measures or stimulate the productive sector meant the country was effectively borrowing time. The entrenched stability of the pound in 2003 was therefore an increasingly expensive illusion, setting the stage for the severe financial crisis that would erupt more than a decade later, when the elaborate scheme to maintain the peg ultimately collapsed.

🌱 Common