5 Francs – Belgian Congo

Context

Years: 1936–1937

Country: Rwanda and Urundi Belgian Congo

Issuer: Belgian Congo

Issuing organization: Bank of the Belgian Congo

Ruler: Leopold III

Currency:

(1908—1960)

Demonetization: 7 January 1952

Total mintage: 14,000,000

Material

Diameter: 33 mm

Weight: 13 g

Thickness: 2.03 mm

Shape: Round

Composition: Nickel brass

Magnetic: No

Technique: Milled

Alignment: Coin alignment

flip

References

KM: #Click to copy to clipboard24

Numista: #8016

Obverse

Description:

Lion left, star left of value, encircled legend.

Inscription:

BANQUE DU CONGO BELGE

5 Fr

BANK VAN BELGISCH CONGO

5 Fr

BANK VAN BELGISCH CONGO

Translation:

Belgian Congo Bank

5 Fr

Bank of Belgian Congo

5 Fr

Bank of Belgian Congo

Script: Latin

Engraver: Marcel Rau

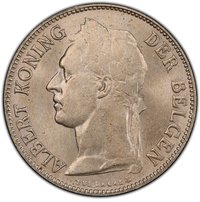

Reverse

Description:

King Leopold III, left profile.

Inscription:

1936

RAU

LEOPOLD III

RAU

LEOPOLD III

Script: Latin

Engraver: Marcel Rau

Edge

Plain

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1936 | — | 2,600,000 | ||

| 1937 | — | 11,400,000 |

Historical background

In 1936, the currency situation in the Belgian Congo was defined by its integration into the Belgian Franc Zone and the authority of the Banque du Congo Belge (BCB). Established in 1909, the BCB held the exclusive privilege of issuing the colony's currency, the Congolese franc, which was pegged at par with and fully convertible to the Belgian franc. This created a stable and predictable monetary environment, tightly controlled from Brussels and Leopoldville, which facilitated the extraction and export of the colony's vast natural resources—primarily copper, gold, and palm oil—by European concessionary companies.

The system was inherently dualistic, serving the modern export economy while largely excluding the indigenous population from its formal benefits. The majority of Congolese people engaged in subsistence agriculture or coerced labor and had little use for cash, except for paying the much-loathed head tax (impôt de capitation). This tax, payable only in Congolese francs, was a primary tool for forcing Africans into the wage-labor market to earn the currency needed to meet their colonial obligations, thereby supplying workers for mines and plantations.

The year 1936 fell within a period of relative stability for the currency itself, but the broader economic context was marked by the lingering effects of the Great Depression. While global commodity prices had begun to recover from their lowest points, the colony's economy was still oriented overwhelmingly toward external markets and Belgian profit. The monetary framework, therefore, was not designed for internal development but as a efficient conduit for colonial revenue, ensuring that the value generated in the Congo was securely anchored to and reinforced the financial system of the metropolitan power.

The system was inherently dualistic, serving the modern export economy while largely excluding the indigenous population from its formal benefits. The majority of Congolese people engaged in subsistence agriculture or coerced labor and had little use for cash, except for paying the much-loathed head tax (impôt de capitation). This tax, payable only in Congolese francs, was a primary tool for forcing Africans into the wage-labor market to earn the currency needed to meet their colonial obligations, thereby supplying workers for mines and plantations.

The year 1936 fell within a period of relative stability for the currency itself, but the broader economic context was marked by the lingering effects of the Great Depression. While global commodity prices had begun to recover from their lowest points, the colony's economy was still oriented overwhelmingly toward external markets and Belgian profit. The monetary framework, therefore, was not designed for internal development but as a efficient conduit for colonial revenue, ensuring that the value generated in the Congo was securely anchored to and reinforced the financial system of the metropolitan power.

🌱 Fairly Common