1 sentimo – Philippines

Add to wishlist

Philippines

Context

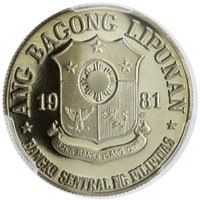

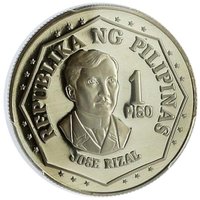

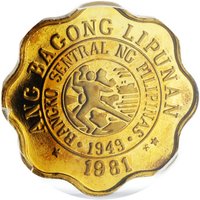

Years: 1979–1982

Issuer: Philippines

Issuing organization: Central Bank of the Philippines

Period:

(since 1946)

Currency:

(since 1967)

Demonetization: 2 January 1998

Total mintage: 97,750,573

Material

Weight: 1.22 g

Thickness: 1.9 mm

Shape: Square with rounded corners

Composition: Aluminium

Magnetic: No

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #

Numista: #7833

Value

Exchange value: 0.01 PHP

Obverse

Reverse

Edge

Plain

Categories

| Person> Military leader |

Mints

| Name | Mark |

|---|---|

| BSP Security Plant Complex | BSP |

| Franklin Mint | (FM) |

Mintings

Historical background

In 1979, the Philippines operated under a managed floating exchange rate system for the Philippine Peso (₱), a structure implemented in 1970 after moving away from a fixed parity with the US dollar. The Central Bank of the Philippines (now Bangko Sentral ng Pilipinas) actively intervened in the foreign exchange market to control volatility and guide the peso's value, which was officially pegged to a basket of currencies of its major trading partners. However, this period was marked by significant external pressures, with the peso experiencing steady depreciation due to a combination of a chronic trade deficit, rising global oil prices from the 1979 energy crisis, and high levels of external debt accumulated during the Marcos administration's infrastructure-driven development strategy.

The country's economic fundamentals were under strain. While the 1970s had seen initial growth, by the decade's end, the Philippines faced a widening current account deficit. The second oil shock drastically increased the import bill, draining foreign reserves, while exports like sugar, coconut products, and minerals faced volatile global prices. Furthermore, the government's heavy borrowing to finance large-scale projects and support state-owned enterprises led to a growing debt service burden. These factors created persistent downward pressure on the peso, forcing the Central Bank to frequently adjust its de facto peg and expend reserves to defend the currency, amidst a backdrop of high inflation that eroded domestic purchasing power.

Consequently, 1979 represented a precarious juncture, setting the stage for the deeper economic crises of the early 1980s. The managed float system, while offering some flexibility, could not insulate the peso from the structural weaknesses of the Philippine economy. The mounting imbalances and reliance on foreign debt eventually culminated in the 1983-1984 balance of payments crisis, triggered by the assassination of Benigno Aquino Jr., which led to a catastrophic loss of confidence, a massive devaluation, and the country's eventual declaration of a debt moratorium. Thus, the currency situation in 1979 was one of managed decline under growing stress, foreshadowing the severe financial turmoil to come.

The country's economic fundamentals were under strain. While the 1970s had seen initial growth, by the decade's end, the Philippines faced a widening current account deficit. The second oil shock drastically increased the import bill, draining foreign reserves, while exports like sugar, coconut products, and minerals faced volatile global prices. Furthermore, the government's heavy borrowing to finance large-scale projects and support state-owned enterprises led to a growing debt service burden. These factors created persistent downward pressure on the peso, forcing the Central Bank to frequently adjust its de facto peg and expend reserves to defend the currency, amidst a backdrop of high inflation that eroded domestic purchasing power.

Consequently, 1979 represented a precarious juncture, setting the stage for the deeper economic crises of the early 1980s. The managed float system, while offering some flexibility, could not insulate the peso from the structural weaknesses of the Philippine economy. The mounting imbalances and reliance on foreign debt eventually culminated in the 1983-1984 balance of payments crisis, triggered by the assassination of Benigno Aquino Jr., which led to a catastrophic loss of confidence, a massive devaluation, and the country's eventual declaration of a debt moratorium. Thus, the currency situation in 1979 was one of managed decline under growing stress, foreshadowing the severe financial turmoil to come.

Series: The New Society Series

🌱 Very Common