50 vatu – Vanuatu

Add to wishlist

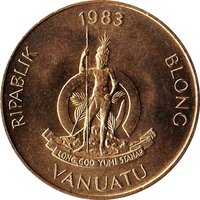

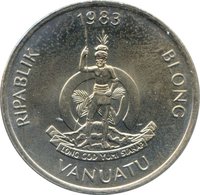

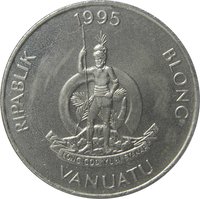

Vanuatu

Context

Material

Diameter: 33 mm

Weight: 15 g

Thickness: 2.25 mm

Shape: Round

Composition: Copper-nickel

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #

Numista: #7751

Value

Exchange value: 50 VUV

Obverse

Reverse

Description:

Yam tubers (Dioscorea), a key Vanuatu food crop, with surrounding stems.

Inscription:

50

VATU

VATU

Script: Latin

Edge

Milled

Categories

| Agriculture |

| Symbols> Coat of Arms |

Mints

| Name | Mark |

|---|---|

| Royal Australian Mint | — |

| Royal Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1983 | — | — | ||

| 1983 | — | — | BU | |

| 1983 | — | — | Proof | |

| 1990 | — | — | ||

| 1995 | — | — | ||

| 1999 | — | — | ||

| 2002 | — | — | ||

| 2009 | — | — |

Historical background

In 1983, the currency situation in Vanuatu was defined by its recent transition from a colonial condominium to an independent nation. Having gained independence from the joint British and French administration (the "Pandemonium") in 1980, the new government faced the immediate task of establishing a sovereign monetary identity. The nation moved swiftly to replace the circulating currencies—the Australian dollar and the New Hebrides franc—with a new national currency, the Vanuatu vatu (VUV), which was introduced in 1981. This was a critical symbolic and economic step in consolidating national sovereignty.

Economically, the early 1980s presented significant challenges for the fledgling vatu. The global recession, coupled with a devastating cyclone in 1985 and a decline in copra prices (a key export), put pressure on the currency and the broader economy. The Vanuatu government, under Prime Minister Walter Lini, pursued a policy of economic nationalism and non-alignment, which included a cautious approach to foreign investment and a focus on agricultural self-reliance. Consequently, the currency was not pegged to any major international currency but was managed with a degree of flexibility, though it remained within the sphere of influence of the Australian dollar due to strong trade and historical ties.

Furthermore, Vanuatu was actively developing its now well-known status as an international financial centre, with legislation for offshore banks and companies passed in the early 1970s and strengthened post-independence. This created a dual dynamic for the currency: a domestic economy facing post-colonial growing pains and external shocks, and a growing offshore financial sector that brought foreign exchange but also complexity. Thus, in 1983, the vatu was a young currency navigating the pressures of building a sustainable domestic economy while the country simultaneously courted a niche role in the global financial system.

Economically, the early 1980s presented significant challenges for the fledgling vatu. The global recession, coupled with a devastating cyclone in 1985 and a decline in copra prices (a key export), put pressure on the currency and the broader economy. The Vanuatu government, under Prime Minister Walter Lini, pursued a policy of economic nationalism and non-alignment, which included a cautious approach to foreign investment and a focus on agricultural self-reliance. Consequently, the currency was not pegged to any major international currency but was managed with a degree of flexibility, though it remained within the sphere of influence of the Australian dollar due to strong trade and historical ties.

Furthermore, Vanuatu was actively developing its now well-known status as an international financial centre, with legislation for offshore banks and companies passed in the early 1970s and strengthened post-independence. This created a dual dynamic for the currency: a domestic economy facing post-colonial growing pains and external shocks, and a growing offshore financial sector that brought foreign exchange but also complexity. Thus, in 1983, the vatu was a young currency navigating the pressures of building a sustainable domestic economy while the country simultaneously courted a niche role in the global financial system.

Series: 1983 Vanuatu circulation coins

🌱 Very Common