100 vatu – Vanuatu

Add to wishlist

Vanuatu

Context

Material

Diameter: 23.9 mm

Weight: 9.55 g

Thickness: 2.95 mm

Shape: Round

Composition: Nickel brass

Magnetic: No

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #

Numista: #3696

Value

Exchange value: 100 VUV

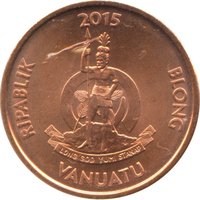

Obverse

Reverse

Edge

Reeded

Mints

| Name | Mark |

|---|---|

| Royal Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1988 | — | — | ||

| 1995 | — | — | ||

| 2002 | — | — | ||

| 2008 | — | — |

Historical background

In 1988, Vanuatu's currency situation was defined by its unique and stable dual-currency system, established following the nation's independence in 1980. The country utilized both the Vanuatu vatu (VUV) and the Australian dollar (AUD) as legal tender. This arrangement was a practical legacy of the Anglo-French condominium and provided economic stability, with the vatu pegged to a basket of currencies, heavily weighted towards the Australian dollar. This peg helped control inflation and foster confidence in the young nation's financial system, which was crucial for developing its tourism and offshore financial services sectors.

Economically, 1988 fell within a period of relative calm for the vatu, following a significant devaluation in 1987. That corrective devaluation, aimed at addressing a growing trade deficit and boosting the competitiveness of Vanuatu's agricultural exports like copra and cocoa, had successfully realigned the currency. By 1988, the economy was adjusting to this new parity, with the Central Bank of Vanuatu (established in 1981) managing the peg and foreign reserves. The dual system facilitated trade and investment from Australia, the country's largest partner, while the vatu served domestic transactions and symbolized monetary sovereignty.

However, the system was not without its complexities. The coexistence of two currencies required careful monetary management to prevent arbitrage and maintain public trust. Furthermore, Vanuatu's economy remained vulnerable to external shocks, particularly fluctuations in global commodity prices and tropical cyclones, which could rapidly impact foreign reserve levels. Thus, while 1988 represented a year of consolidated stability after the 1987 adjustment, the underlying challenge for authorities was to nurture economic diversification and resilience within the constraints of a small, open island economy dependent on its fixed exchange rate regime.

Economically, 1988 fell within a period of relative calm for the vatu, following a significant devaluation in 1987. That corrective devaluation, aimed at addressing a growing trade deficit and boosting the competitiveness of Vanuatu's agricultural exports like copra and cocoa, had successfully realigned the currency. By 1988, the economy was adjusting to this new parity, with the Central Bank of Vanuatu (established in 1981) managing the peg and foreign reserves. The dual system facilitated trade and investment from Australia, the country's largest partner, while the vatu served domestic transactions and symbolized monetary sovereignty.

However, the system was not without its complexities. The coexistence of two currencies required careful monetary management to prevent arbitrage and maintain public trust. Furthermore, Vanuatu's economy remained vulnerable to external shocks, particularly fluctuations in global commodity prices and tropical cyclones, which could rapidly impact foreign reserve levels. Thus, while 1988 represented a year of consolidated stability after the 1987 adjustment, the underlying challenge for authorities was to nurture economic diversification and resilience within the constraints of a small, open island economy dependent on its fixed exchange rate regime.

🌱 Very Common