1 Baht – Thailand

Circulating commemorative coins

Commemoration: 1970 Asian Games, Bangkok

Thailand

Context

Year: 1970

Thai Year: 2513

Issuer: Thailand

Ruler: Bhumibol Adulyadej

Currency:

(since 1897)

Demonetized: Yes

Total mintage: 9,000,000

Material

Diameter: 26.9 mm

Weight: 7.4 g

Thickness: 1.8 mm

Shape: Round

Composition: Copper-nickel

Technique: Milled

Alignment: Coin alignment

flip

References

Y: #Click to copy to clipboard91

Numista: #7739

Value

Exchange value: 1 THB = $0.03

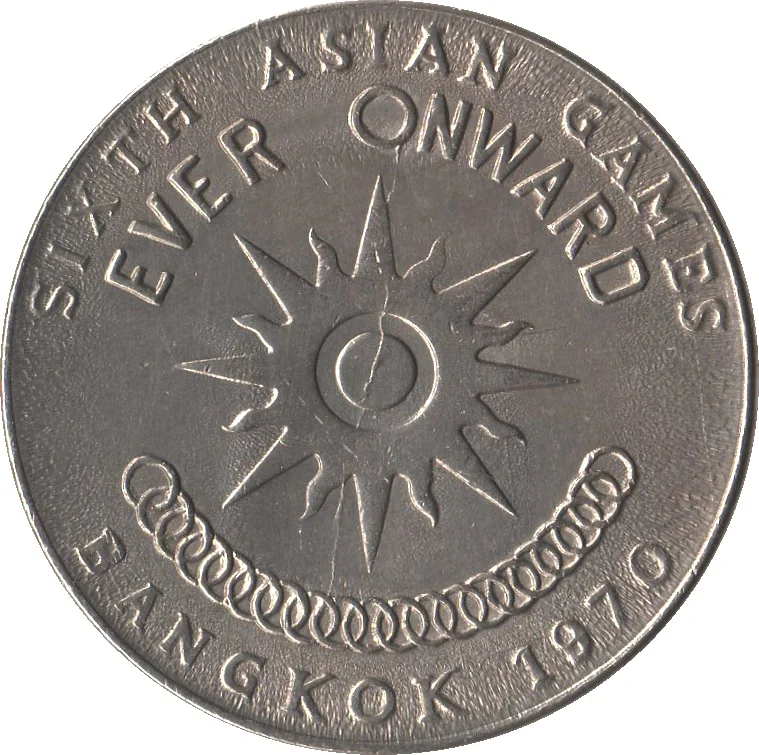

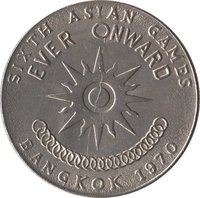

Obverse

Reverse

Description:

Asian Games symbol: a sun with 16 rays, motto above, 20 conjoined circles below, surrounded by inscriptions.

Inscription:

SIXTH ASIAN GAMES

EVER ONWARD

BANGKOK 1970

EVER ONWARD

BANGKOK 1970

Script: Latin

Edge

Reeded

Categories

| Sport> Asian Games |

| Symbol> Sun |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1970 | — | 9,000,000 |

Historical background

In 1970, Thailand's currency system was defined by the baht, which operated under a fixed exchange rate regime pegged to the U.S. dollar at approximately 20.8 baht per dollar. This peg, managed by the Bank of Thailand, provided crucial stability for an economy that was still largely agricultural but was in the early stages of a significant industrialization and export-oriented push. The fixed rate facilitated international trade and investment, which were central to the government's development plans under the US-aligned military leadership of Field Marshal Thanom Kittikachorn.

The period was one of relative monetary stability, supported by conservative fiscal policies and substantial foreign exchange reserves accumulated from key exports like rice, rubber, and tin, as well as from growing tourism revenues. Importantly, Thailand benefited economically from its strategic role during the Vietnam War, receiving significant U.S. military spending and aid, which further bolstered its balance of payments and reinforced the baht's peg. This external inflow helped offset trade deficits and provided the central bank with the reserves needed to confidently maintain the fixed parity.

However, this stability existed within a broader context of regional uncertainty and underlying pressures. The gold standard for international transactions had ended in 1968, and the global Bretton Woods system of fixed rates was showing severe strains, which would culminate in its collapse in 1971. While the Thai baht itself was not under immediate speculative attack in 1970, the impending international monetary crisis foreshadowed future challenges. The rigidity of the peg would eventually become a constraint, but for that year, it served as a cornerstone for Thailand's growing, yet still developing, post-war economy.

The period was one of relative monetary stability, supported by conservative fiscal policies and substantial foreign exchange reserves accumulated from key exports like rice, rubber, and tin, as well as from growing tourism revenues. Importantly, Thailand benefited economically from its strategic role during the Vietnam War, receiving significant U.S. military spending and aid, which further bolstered its balance of payments and reinforced the baht's peg. This external inflow helped offset trade deficits and provided the central bank with the reserves needed to confidently maintain the fixed parity.

However, this stability existed within a broader context of regional uncertainty and underlying pressures. The gold standard for international transactions had ended in 1968, and the global Bretton Woods system of fixed rates was showing severe strains, which would culminate in its collapse in 1971. While the Thai baht itself was not under immediate speculative attack in 1970, the impending international monetary crisis foreshadowed future challenges. The rigidity of the peg would eventually become a constraint, but for that year, it served as a cornerstone for Thailand's growing, yet still developing, post-war economy.

🌱 Common