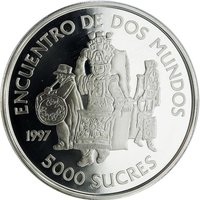

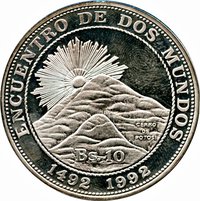

10 Bolivianos – Bolivia

Non-circulating coins

Commemoration: Ibero-American Series III - Dances and customs - Diablada

Series: Ibero-American

Bolivia

Obverse

Reverse

Edge

Reeded

Categories

| Art> Dance |

| Symbols> Coat of Arms |

Mints

| Name | Mark |

|---|---|

| Royal Mint of Madrid | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1997 | — | 6,000 | Proof |

Historical background

In 1997, Bolivia was operating under a framework of relative macroeconomic stability, a significant achievement following the hyperinflation and deep economic crises of the early-to-mid 1980s. The cornerstone of this stability was a fixed exchange rate regime, established in 1987, which pegged the Bolivian boliviano to the US dollar. This policy, known as the "Economic Stabilization Plan," was crucial for taming inflation, which had plummeted from an annual rate of over 20,000% in 1985 to a manageable single-digit figure by 1997. The fixed exchange rate provided predictability for trade and investment, anchoring the economy after years of turmoil.

However, this stability came with significant trade-offs and underlying vulnerabilities. The fixed peg limited the Central Bank of Bolivia's ability to conduct independent monetary policy and required substantial foreign currency reserves to maintain. By the mid-1990s, the system was facing pressure from a persistent current account deficit, partly due to declining prices for key exports like natural gas and minerals. Furthermore, the strength of the US dollar, to which the boliviano was tied, made Bolivian non-traditional exports less competitive regionally, stifling economic diversification and growth.

Consequently, 1997 was a year of transition and debate. The government of President Gonzalo Sánchez de Lozada, who had first implemented the shock therapy reforms in 1985, was contending with the limitations of the rigid exchange system. While the peg had successfully ended hyperinflation, it was increasingly seen as a constraint on competitiveness and responsive economic management. This period set the stage for the eventual shift in the early 2000s to a managed floating exchange rate regime, which sought to preserve stability while allowing for greater flexibility to absorb external shocks and promote export-led growth.

However, this stability came with significant trade-offs and underlying vulnerabilities. The fixed peg limited the Central Bank of Bolivia's ability to conduct independent monetary policy and required substantial foreign currency reserves to maintain. By the mid-1990s, the system was facing pressure from a persistent current account deficit, partly due to declining prices for key exports like natural gas and minerals. Furthermore, the strength of the US dollar, to which the boliviano was tied, made Bolivian non-traditional exports less competitive regionally, stifling economic diversification and growth.

Consequently, 1997 was a year of transition and debate. The government of President Gonzalo Sánchez de Lozada, who had first implemented the shock therapy reforms in 1985, was contending with the limitations of the rigid exchange system. While the peg had successfully ended hyperinflation, it was increasingly seen as a constraint on competitiveness and responsive economic management. This period set the stage for the eventual shift in the early 2000s to a managed floating exchange rate regime, which sought to preserve stability while allowing for greater flexibility to absorb external shocks and promote export-led growth.

Series: Ibero-American

💎 Very Rare