10 bolivianos – Bolivia

Add to wishlist

Non-circulating coins

Commemoration: Ibero-American Series I - Encounter of two Worlds

Series: Ibero-American

Bolivia

Obverse

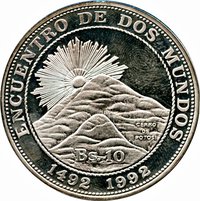

Description:

National arms within legend, arms encircling.

Inscription:

REPUBLICA DE BOLIVIA

1991

BOLIVIA

ESTADOS UNIDOS MEXICANOS

REPUBLICA DE NICARAGUA · AMERICA CENTRAL ·

1991

BOLIVIA

ESTADOS UNIDOS MEXICANOS

REPUBLICA DE NICARAGUA · AMERICA CENTRAL ·

Translation:

REPUBLIC OF BOLIVIA

1991

BOLIVIA

UNITED MEXICAN STATES

REPUBLIC OF NICARAGUA · CENTRAL AMERICA ·

1991

BOLIVIA

UNITED MEXICAN STATES

REPUBLIC OF NICARAGUA · CENTRAL AMERICA ·

Script: Latin

Language: Spanish

Reverse

Edge

Reeded

Categories

| Symbols> Coat of Arms |

| Geography> Mountain |

Mints

| Name | Mark |

|---|---|

| Royal Mint of Madrid | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1991 | — | 20,000 | Proof |

Historical background

In 1991, Bolivia was in the midst of a profound economic transformation following a period of hyperinflation and crisis in the 1980s. The cornerstone of this shift was the New Economic Policy (NEP) enacted in 1985, which centered on drastic stabilization, liberalization, and the adoption of a freely floating exchange rate. By 1991, the Bolivian peso had been replaced by the boliviano (at a rate of 1 boliviano = 1,000,000 old pesos), and the central bank had ceased its practice of financing public deficits through money creation. This disciplined fiscal and monetary approach, supported by the International Monetary Fund, had successfully tamed hyperinflation, bringing annual rates down from peaks over 20,000% to under 20% by the early 1990s.

The currency regime itself was characterized by a managed float, where the boliviano's value was primarily determined by market forces in the newly legalized parallel market, but with occasional central bank intervention to smooth out excessive volatility. This system represented a stark departure from the fixed and multiple exchange rates of the past, aiming to foster transparency and eliminate distortions. A critical supporting policy was the Capitalization Law of 1990, which encouraged foreign investment and dollar inflows, helping to stabilize the foreign exchange market and build international reserves.

Consequently, by 1991, the currency situation was one of fragile stability. The boliviano was not pegged and experienced modest fluctuations, but it benefited from increased confidence due to consistent anti-inflation policies and growing dollar liquidity from nascent natural gas exports and cocaine-related dollar inflows (a persistent, informal factor). The primary challenges were no longer hyperinflation but sustaining growth, managing dollarization (as many savings and contracts remained dollar-denominated), and addressing deep-seated poverty and social inequality—the lingering effects of the stabilization's initial recessionary impact.

The currency regime itself was characterized by a managed float, where the boliviano's value was primarily determined by market forces in the newly legalized parallel market, but with occasional central bank intervention to smooth out excessive volatility. This system represented a stark departure from the fixed and multiple exchange rates of the past, aiming to foster transparency and eliminate distortions. A critical supporting policy was the Capitalization Law of 1990, which encouraged foreign investment and dollar inflows, helping to stabilize the foreign exchange market and build international reserves.

Consequently, by 1991, the currency situation was one of fragile stability. The boliviano was not pegged and experienced modest fluctuations, but it benefited from increased confidence due to consistent anti-inflation policies and growing dollar liquidity from nascent natural gas exports and cocaine-related dollar inflows (a persistent, informal factor). The primary challenges were no longer hyperinflation but sustaining growth, managing dollarization (as many savings and contracts remained dollar-denominated), and addressing deep-seated poverty and social inequality—the lingering effects of the stabilization's initial recessionary impact.

Series: Ibero-American

⭐ Rare