500 Piastres – Egypt

Egypt

Context

Year: 1922

Islamic (Hijri) Year: 1340

Issuer: Egypt

Ruler: Ahmed Fuad I

Currency:

(since 1916)

Demonetized: Yes

Total mintage: 1,800

Material

References

KM: #Click to copy to clipboard342

Numista: #62814

Value

Exchange value: 5 EGP

Bullion value: $6203.87

Obverse

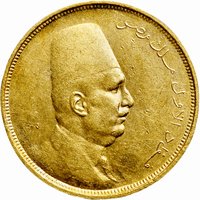

Description:

King Fuad I in civilian dress, bust right.

Inscription:

فؤاد الأول ملك مصر

Translation:

Fuad I, King of Egypt.

Script: Arabic (naskh)

Language: Arabic

Designer: Hamed Effendi Serri

Reverse

Description:

Denomination top, dates bottom.

Inscription:

٥٠٠ غرش

المملكة المصرية

١٩٢٣ ١٣٤٠

المملكة المصرية

١٩٢٣ ١٣٤٠

Translation:

500 Qirsh

The Egyptian Kingdom

1923 1340

The Egyptian Kingdom

1923 1340

Script: Arabic

Language: Arabic

Designer: Hamed Effendi Serri

Edge

Mints

| Name | Mark |

|---|---|

| Royal Mint (Tower Hill) | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1922 | — | 1,800 | ||

| 1922 | — | — | Proof |

Historical background

In 1922, Egypt's currency situation was a complex legacy of British colonial influence and the formal transition to nominal independence. The country operated under a Currency Board System, established in 1885, which tied the Egyptian pound (EE£) to the British pound sterling at a fixed parity of EE£1 = £1 0s 6d. This system required full gold backing for issued banknotes, ensuring stability but ceding monetary sovereignty. The National Bank of Egypt, a private institution with strong British ties, acted as the note-issuing authority, further embedding British financial control.

This monetary framework provided significant stability and facilitated international trade, but it was a symbol of Egypt's constrained sovereignty. While the country had been declared a sovereign kingdom in February 1922, ending the British protectorate, key reserves of power—including the protection of foreign interests and the Suez Canal—remained under British control. Consequently, the sterling peg and the British-dominated banking system persisted, meaning Egypt’s economy and currency remained yoked to British economic policy and the gold standard.

Thus, in 1922, Egypt possessed a stable and credible currency, but it was not a tool of national economic policy. The arrangement reflected the paradoxical reality of the early post-protectorate period: political independence was declared, yet economic and financial independence was deferred. The currency system would remain largely unchanged until the mid-20th century, when rising nationalism and changing global monetary conditions eventually led to the establishment of a central bank and a break from the sterling peg.

This monetary framework provided significant stability and facilitated international trade, but it was a symbol of Egypt's constrained sovereignty. While the country had been declared a sovereign kingdom in February 1922, ending the British protectorate, key reserves of power—including the protection of foreign interests and the Suez Canal—remained under British control. Consequently, the sterling peg and the British-dominated banking system persisted, meaning Egypt’s economy and currency remained yoked to British economic policy and the gold standard.

Thus, in 1922, Egypt possessed a stable and credible currency, but it was not a tool of national economic policy. The arrangement reflected the paradoxical reality of the early post-protectorate period: political independence was declared, yet economic and financial independence was deferred. The currency system would remain largely unchanged until the mid-20th century, when rising nationalism and changing global monetary conditions eventually led to the establishment of a central bank and a break from the sterling peg.

Series: King Fuad I (Civic Attire)

💎 Extremely Rare