50 tenge (Kazakhstan Constitution adoption) – Kazakhstan

Add to wishlist

Non-circulating coins

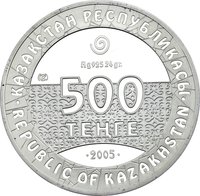

Commemoration: 10th Anniversary of adoption of Kazakhstan Constitution

Series: Events

Kazakhstan

Context

Material

Diameter: 31 mm

Weight: 11.17 g

Shape: Round

Composition: Nickel silver

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #

Numista: #6239

Value

Exchange value: 50 KZT

Obverse

Description:

National Coat of Arms with denomination.

Inscription:

••• ҚАЗАҚСТАН • 50 ТЕҢГЕ • ҰЛТТЫҚ БАНКІ •••

ҚҰБ

ҚҰБ

Translation:

KAZAKHSTAN • 50 TENGE • NATIONAL BANK • KUB

Language: Kazakh

Reverse

Description:

National Coat of Arms centered in sun rays, with the constitution and date below.

Inscription:

ҚАЗАҚСТАН КОНСТИТУЦИЯСЫНА

10 ЖЫЛ

• 2005 •

10 ЖЫЛ

• 2005 •

Translation:

10 Years of the Constitution of Kazakhstan

• 2005 •

• 2005 •

Language: Kazakh

Edge

Segmented reeding

Categories

| Symbols> Coat of Arms |

Mints

| Name | Mark |

|---|---|

| Kazakhstan Mint | (ҚҰБ) |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2005 | ҚҰБ | 50,000 |

Historical background

In 2005, Kazakhstan's currency situation was characterized by a period of remarkable stability and strength for the tenge, a stark contrast to the volatility of previous years. This stability was underpinned by a managed float exchange rate regime overseen by the National Bank of Kazakhstan (NBK). The primary driver was a sustained boom in global oil prices, which fueled massive foreign direct investment into the country's energy sector. This influx generated substantial dollar revenues, leading to significant foreign exchange reserves and a strong balance of payments, which the NBK actively managed to prevent excessive tenge appreciation that could harm non-oil exports.

The central bank's policy focused on maintaining a competitive and predictable exchange rate to support economic diversification and control inflation. It routinely intervened in the foreign exchange market, buying surplus US dollars to moderate the tenge's rise. This strategy successfully built reserves to record levels while keeping tenge/dollar movements within a narrow band. Consequently, annual inflation, though still a concern, was managed at a moderate level (approximately 7.5% in 2005), and the tenge experienced only a gradual nominal appreciation against the dollar throughout the year.

This stable environment was widely seen as a key achievement and a foundation for robust economic growth, which exceeded 9% in 2005. However, it also exposed underlying vulnerabilities. The economy's growing dependence on hydrocarbon revenues created a "Dutch Disease" dynamic, where the strong tenge made other sectors less competitive. Furthermore, the managed regime required continuous intervention, masking the true market pressure for appreciation and storing potential imbalances. The situation of 2005, therefore, represented a calm before future challenges, setting the stage for the difficult policy decisions that would follow during the 2007-2008 global financial crisis and the eventual shift to a free float in 2015.

The central bank's policy focused on maintaining a competitive and predictable exchange rate to support economic diversification and control inflation. It routinely intervened in the foreign exchange market, buying surplus US dollars to moderate the tenge's rise. This strategy successfully built reserves to record levels while keeping tenge/dollar movements within a narrow band. Consequently, annual inflation, though still a concern, was managed at a moderate level (approximately 7.5% in 2005), and the tenge experienced only a gradual nominal appreciation against the dollar throughout the year.

This stable environment was widely seen as a key achievement and a foundation for robust economic growth, which exceeded 9% in 2005. However, it also exposed underlying vulnerabilities. The economy's growing dependence on hydrocarbon revenues created a "Dutch Disease" dynamic, where the strong tenge made other sectors less competitive. Furthermore, the managed regime required continuous intervention, masking the true market pressure for appreciation and storing potential imbalances. The situation of 2005, therefore, represented a calm before future challenges, setting the stage for the difficult policy decisions that would follow during the 2007-2008 global financial crisis and the eventual shift to a free float in 2015.

Series: Events

🌟 Uncommon