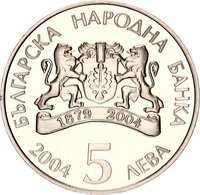

Obverse

Description:

The obverse shows the Bulgarian National Bank logo with '1879' and '2004' on its ribbon, encircled by 'BULGARIAN NATIONAL BANK', '10 LEVS', and '2004'.

Inscription:

БЪЛГАРСКА НАРОДНА БАНКА

2004 10 ЛЕВА

2004 10 ЛЕВА

Translation:

BULGARIAN NATIONAL BANK

2004 10 LEVA

2004 10 LEVA

Script: Cyrillic

Language: Bulgarian

Engraver: Evgeni Evtimov

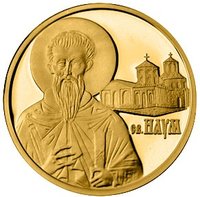

Reverse

Description:

The reverse depicts Saint Nicholas the Miracle Worker of Myra and Lycia, based on a Bulgarian icon, in partial gold finish, surrounded by the Cyrillic inscription of his name and title.

Inscription:

СВЕТИ НИКОЛАЙ МИРЛИКИЙСКИ ЧУДОТВОРЕЦ

Translation:

SAINT NICHOLAS OF MYRA THE WONDERWORKER

Script: Cyrillic

Language: Church Slavonic

Engraver: Evgeni Evtimov

Edge

Plain

Categories

| Person> Religious figure |

Mints

| Name | Mark |

|---|---|

| Bulgarian Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2004 | — | 8,000 | Proof |

Historical background

In 2004, Bulgaria was in a critical and stable phase of its post-communist monetary history, operating under a Currency Board Arrangement (CBA) established in July 1997. This strict regime was implemented following a severe financial and hyperinflation crisis, and it pegged the Bulgarian lev (BGN) firmly to the German Deutsche Mark, and subsequently to the euro after its introduction, at a rate of 1.95583 leva for one euro. The CBA mandated that every lev in circulation be fully backed by foreign reserves, severely restricting the central bank's ability to conduct independent monetary policy or act as a lender of last resort. This discipline had successfully restored monetary stability, tamed inflation, and built significant foreign exchange reserves.

The year 2004 was significant as Bulgaria was actively progressing toward its strategic goal of European Union accession, which it achieved on January 1, 2007. A key requirement for eventual Eurozone membership was participation in the EU's Exchange Rate Mechanism II (ERM II), which the currency board was seen as a de facto precursor to. The government, led by Prime Minister Simeon Saxe-Coburg-Gotha, maintained a firm commitment to the currency board, viewing it as the cornerstone of economic credibility. This stability, coupled with structural reforms, supported strong GDP growth and increasing foreign direct investment during this period.

However, the rigid system also presented challenges. The currency board limited tools for adjusting to economic shocks, placing the entire burden of adjustment on fiscal policy and domestic prices and wages. Furthermore, while the peg ensured stability, it meant Bulgaria had no control over its interest rates, which were effectively set by the European Central Bank. In 2004, the economy also faced pressures from a growing current account deficit, fueled by strong domestic demand and imports, which raised concerns about long-term sustainability under the fixed exchange rate. Nevertheless, the consensus in 2004 was that the benefits of the currency board in ensuring stability and guiding the path to the EU far outweighed these risks.

The year 2004 was significant as Bulgaria was actively progressing toward its strategic goal of European Union accession, which it achieved on January 1, 2007. A key requirement for eventual Eurozone membership was participation in the EU's Exchange Rate Mechanism II (ERM II), which the currency board was seen as a de facto precursor to. The government, led by Prime Minister Simeon Saxe-Coburg-Gotha, maintained a firm commitment to the currency board, viewing it as the cornerstone of economic credibility. This stability, coupled with structural reforms, supported strong GDP growth and increasing foreign direct investment during this period.

However, the rigid system also presented challenges. The currency board limited tools for adjusting to economic shocks, placing the entire burden of adjustment on fiscal policy and domestic prices and wages. Furthermore, while the peg ensured stability, it meant Bulgaria had no control over its interest rates, which were effectively set by the European Central Bank. In 2004, the economy also faced pressures from a growing current account deficit, fueled by strong domestic demand and imports, which raised concerns about long-term sustainability under the fixed exchange rate. Nevertheless, the consensus in 2004 was that the benefits of the currency board in ensuring stability and guiding the path to the EU far outweighed these risks.

Series: Bulgarian Iconography

💎 Extremely Rare