20 drachmai – Greece

Add to wishlist

Greece

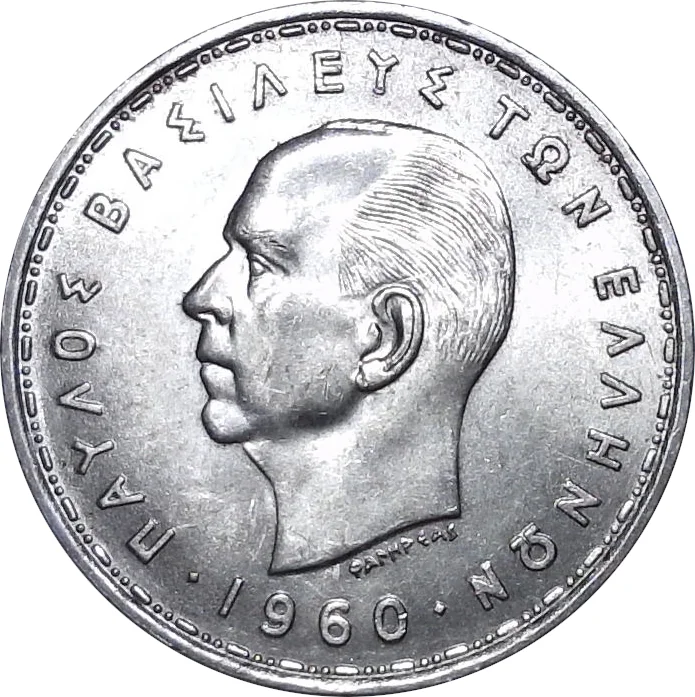

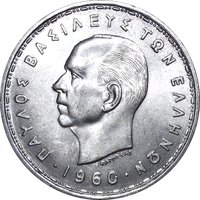

Obverse

Description:

Paul I bust left, date below.

Inscription:

ΠΑΥΛΟΣ ΒΑΣΙΛΕΥΣ ΤΩΝ ΕΛΛΗΝΩΝ

1960

1960

Translation:

PAUL KING OF THE HELLENES

1960

1960

Script: Greek

Language: Greek

Engraver: Vasos Falireas

Reverse

Description:

Moon goddess Selene on horseback, denomination left.

Inscription:

20

ΔΡΧ

ΔΡΧ

Translation:

Twenty drachmas

Script: Greek

Language: Greek

Engraver: Vasos Falireas

Edge

Inscripted with raised lettering and the date

Legend:

ΒΑΣΙΛΕΙΟΝ ΤΗΣ ΕΛΛΑΔΟΣ 1960

Translation:

KINGDOM OF GREECE 1960

Language: Greek

Mints

| Name | Mark |

|---|---|

| Royal Mint (Tower Hill) | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1960 | — | 20,000,000 | ||

| 1960 | — | — | Proof | |

| 1965 | — | — | ||

| 1965 | — | 4,987 | Proof |

Historical background

In 1960, Greece's currency situation was defined by its membership in the Bretton Woods system, with the drachma (GRD) pegged to the US dollar at a fixed rate of 30 drachmae to one dollar. This stability was underpinned by Greece's participation in the European Payments Union and its broader alignment with Western economic structures, following the recovery from the civil war. The period was one of relative monetary stability and economic growth, known as the "Greek economic miracle," driven by industrialization, tourism, and remittances from Greeks abroad, which bolstered the country's foreign exchange reserves.

However, this fixed parity masked underlying economic pressures. The drachma was widely considered overvalued, which hurt the competitiveness of Greek exports and contributed to a persistent trade deficit. The economy relied heavily on invisible earnings—shipping, tourism, and emigrant remittances—to balance its current account. Furthermore, the political landscape was tense, with significant social inequalities and a fragile government, setting the stage for future monetary challenges.

The stability of 1960 proved to be a calm before the storm. Within a few years, pressures would mount, leading to a significant devaluation in 1953 (a key pre-1960 adjustment) and again in 1967. The fixed exchange rate regime ultimately limited Greece's ability to independently manage monetary policy to address domestic inflation and growth, a tension that would characterize its economic trajectory long after the Bretton Woods system collapsed in the early 1970s.

However, this fixed parity masked underlying economic pressures. The drachma was widely considered overvalued, which hurt the competitiveness of Greek exports and contributed to a persistent trade deficit. The economy relied heavily on invisible earnings—shipping, tourism, and emigrant remittances—to balance its current account. Furthermore, the political landscape was tense, with significant social inequalities and a fragile government, setting the stage for future monetary challenges.

The stability of 1960 proved to be a calm before the storm. Within a few years, pressures would mount, leading to a significant devaluation in 1953 (a key pre-1960 adjustment) and again in 1967. The fixed exchange rate regime ultimately limited Greece's ability to independently manage monetary policy to address domestic inflation and growth, a tension that would characterize its economic trajectory long after the Bretton Woods system collapsed in the early 1970s.

🌱 Very Common