200 escudos – Portugal

Add to wishlist

Non-circulating coins

Commemoration: First portuguese on Tanegeshima island

Portugal

Obverse

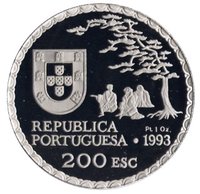

Description:

Portuguese ship near Japan, in Namban style. Latin name and Japanese island above; landing and coin date below, ringed in pearls.

Inscription:

REPUBLICA PORTUGUESA

200 ESCUDOS

200 ESCUDOS

Translation:

Portuguese Republic

200 Escudos

200 Escudos

Script: Latin

Language: Portuguese

Engraver: Eloísa Byrne

Reverse

Description:

Portuguese coat of arms left, Namban-style sea and compass right. Country name and value framed by a pearl circle.

Inscription:

種子島 * TANEGASHIMA

INCM * 1543•1993 * E.BYRNE

INCM * 1543•1993 * E.BYRNE

Translation:

Tanegashima

INCM * 1543•1993 * E.BYRNE

INCM * 1543•1993 * E.BYRNE

Script: Latin

Engraver: Eloísa Byrne

Edge

Reeded

Categories

| Map |

| Transportation> Watercraft |

Mints

| Name | Mark |

|---|---|

| Imprensa Nacional - Casa da Moeda | incm |

Historical background

In 1993, Portugal's currency situation was defined by its pivotal role within the European Monetary System (EMS) and the intense national effort to meet the strict convergence criteria for European Economic and Monetary Union (EMU). The Portuguese escudo (PTE) was a member of the EMS Exchange Rate Mechanism (ERM), which required it to maintain its value within a narrow band of fluctuation against other member currencies, most importantly the German Deutsche Mark. This commitment served as a key anchor for monetary policy, aimed at curbing Portugal's historically high inflation and fostering economic stability in the wake of the country's rapid modernization and integration into the European Community.

Domestically, this period was characterized by a challenging but determined policy of desinflação (disinflation). The Banco de Portugal, under this ERM discipline, pursued tight monetary policies to bring down inflation, which had been in double digits for much of the 1980s. Success was evident, as inflation fell to approximately 6.4% in 1993, down from over 13% just three years earlier. However, this came at a short-term economic cost, with the country experiencing a mild recession in 1993, highlighting the tension between achieving convergence targets and maintaining domestic growth.

The broader context was the Maastricht Treaty, which had been ratified in 1992 and set the roadmap for the single currency. Therefore, every monetary decision in 1993 was viewed through the lens of qualifying for the Euro. While the escudo faced pressures within the ERM during the 1992-93 crisis that forced several currencies to devalue or exit, Portugal successfully maintained its parity, demonstrating political and economic resolve. The year 1993 thus represented a critical consolidation phase, solidifying the escudo's stability and setting the stage for Portugal's eventual entry into the Eurozone at its inception in 1999.

Domestically, this period was characterized by a challenging but determined policy of desinflação (disinflation). The Banco de Portugal, under this ERM discipline, pursued tight monetary policies to bring down inflation, which had been in double digits for much of the 1980s. Success was evident, as inflation fell to approximately 6.4% in 1993, down from over 13% just three years earlier. However, this came at a short-term economic cost, with the country experiencing a mild recession in 1993, highlighting the tension between achieving convergence targets and maintaining domestic growth.

The broader context was the Maastricht Treaty, which had been ratified in 1992 and set the roadmap for the single currency. Therefore, every monetary decision in 1993 was viewed through the lens of qualifying for the Euro. While the escudo faced pressures within the ERM during the 1992-93 crisis that forced several currencies to devalue or exit, Portugal successfully maintained its parity, demonstrating political and economic resolve. The year 1993 thus represented a critical consolidation phase, solidifying the escudo's stability and setting the stage for Portugal's eventual entry into the Eurozone at its inception in 1999.

⭐ Somewhat Rare