5 francs cfa – Western African States

Add to wishlist

Context

Year: 1960

Issuer: Western African States

Issuing organization: Central Bank of Western African States

Currency:

(since 1958)

Total mintage: 5,000,000

Material

References

KM: #

Numista: #11074

Value

Exchange value: 5 XOF

Obverse

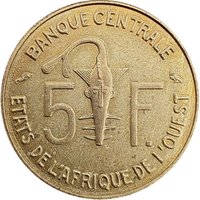

Description:

BCEAO emblem and value

Inscription:

5 F.

BANQUE CENTRALE

ETATS DE L'AFRIQUE DE L'OUEST

BANQUE CENTRALE

ETATS DE L'AFRIQUE DE L'OUEST

Translation:

5 FRANCS

CENTRAL BANK

OF THE WEST AFRICAN STATES

CENTRAL BANK

OF THE WEST AFRICAN STATES

Script: Latin

Language: French

Engravers: Gabriel Bernard, Lucien Bazor

Reverse

Description:

Swift antelope

Inscription:

G. B. L. BAZOR

1960

1960

Script: Latin

Engravers: Gabriel Bernard, Lucien Bazor

Edge

Plain

Mints

| Name | Mark |

|---|---|

| Monnaie de Paris | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1960 | — | 5,000,000 |

Historical background

In 1960, the currency situation across the newly independent states of Francophone West Africa was one of deep colonial continuity, managed through the CFA franc (Colonies Françaises d'Afrique). This currency, created by France in 1945, was fully guaranteed by the French Treasury and pegged at a fixed rate to the French franc. For the eight newly sovereign nations—including Senegal, Ivory Coast, and Mali—this arrangement provided immediate monetary stability and facilitated trade with France, but it also meant that their monetary policy was effectively set in Paris, with their foreign reserves pooled and held by France. This system was a double-edged sword, offering economic security while symbolizing a lingering economic dependence.

In contrast, the former British colonies, such as Nigeria and Ghana (which had gained independence in 1957), pursued different paths. They initially operated within the British West African pound, a currency board system that also tied their currency to sterling. However, by 1960, these nations were actively moving toward establishing their own central banks and national currencies as stronger symbols of sovereignty. Nigeria, for instance, would introduce the Nigerian pound in 1959 and establish its central bank in 1958, seeking greater control over its monetary policy and economic destiny separate from the sterling area.

Thus, the currency landscape of 1960 reflected the divergent colonial legacies and immediate post-independence strategies of the region. The Francophone states largely retained a centralized, externally guaranteed currency union (the West African CFA), prioritizing stability and maintained economic links. The Anglophone states were in a transitional phase, dismantling the colonial currency framework in favour of national monetary institutions. In both cases, the fundamental challenge was balancing the practical needs for stability and accessible foreign exchange with the political imperative for economic self-determination in the dawn of independence.

In contrast, the former British colonies, such as Nigeria and Ghana (which had gained independence in 1957), pursued different paths. They initially operated within the British West African pound, a currency board system that also tied their currency to sterling. However, by 1960, these nations were actively moving toward establishing their own central banks and national currencies as stronger symbols of sovereignty. Nigeria, for instance, would introduce the Nigerian pound in 1959 and establish its central bank in 1958, seeking greater control over its monetary policy and economic destiny separate from the sterling area.

Thus, the currency landscape of 1960 reflected the divergent colonial legacies and immediate post-independence strategies of the region. The Francophone states largely retained a centralized, externally guaranteed currency union (the West African CFA), prioritizing stability and maintained economic links. The Anglophone states were in a transitional phase, dismantling the colonial currency framework in favour of national monetary institutions. In both cases, the fundamental challenge was balancing the practical needs for stability and accessible foreign exchange with the political imperative for economic self-determination in the dawn of independence.

🌱 Common