50 cents (Accession of Elizabeth II) – Australia

Add to wishlist

Circulating commemorative coins

Commemoration: 25th Anniversary of the Accession of Elizabeth II

Series: Royal Related 50 Cent Coins

Australia

Context

Material

Diameter: 31.51 mm

Weight: 15.55 g

Thickness: 3 mm

Shape: Dodecagonal

Standard: Silver half ounce

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #

Numista: #5524

Value

Exchange value: 0.50 AUD

Inflation-adjusted value: 3.84 AUD

Obverse

Description:

Queen Elizabeth II facing right in the Girls of Great Britain and Ireland Tiara.

Inscription:

ELIZABETH II

AUSTRALIA 1977

AUSTRALIA 1977

Script: Latin

Designer: Arnold Machin

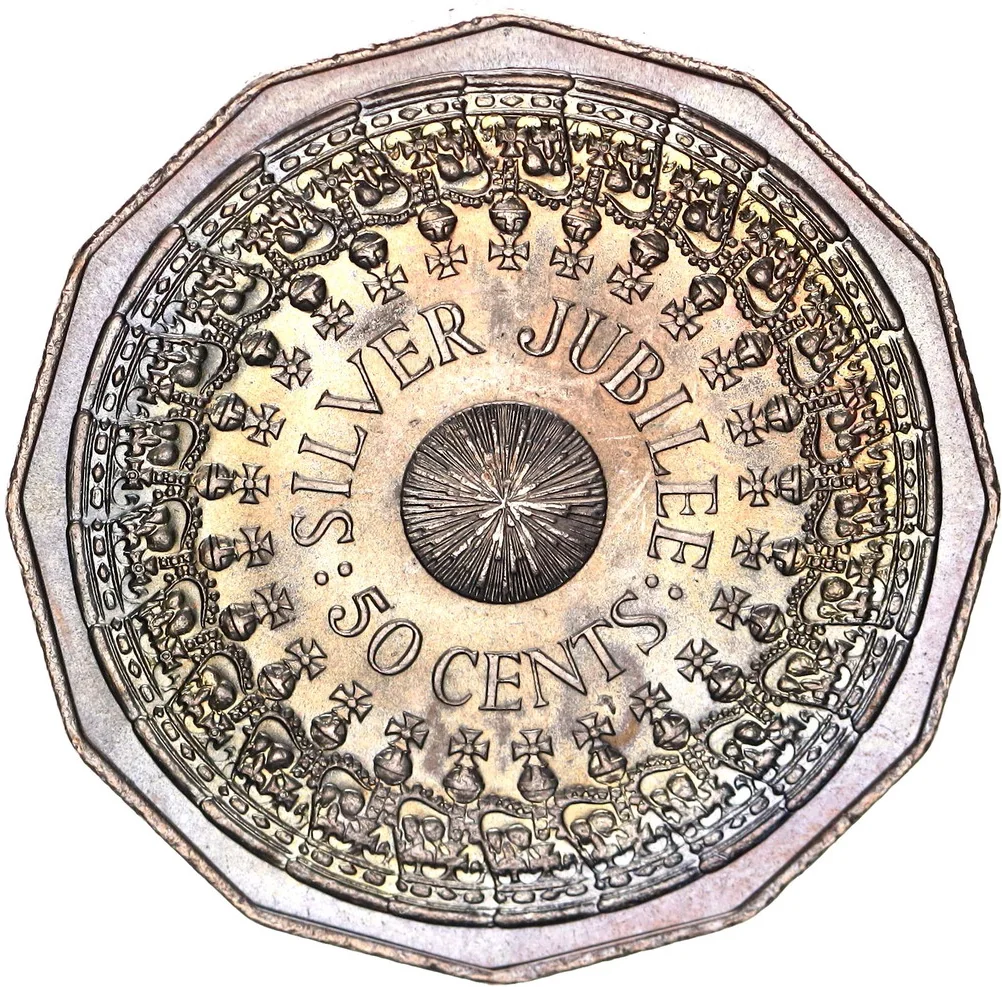

Reverse

Description:

Twenty-five overlapping crowns encircling a starburst with lettering and value.

Inscription:

:SILVER JUBILEE:

50 CENTS

50 CENTS

Script: Latin

Designer: Stuart Devlin

Edge

12 Sided Smooth

Categories

| Event> Coronation |

| Person> Monarch |

Mints

| Name | Mark |

|---|---|

| Royal Australian Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1977 | — | 128,010 | BU | |

| 1977 | — | 25,067,000 | ||

| 1977 | — | 55,006 | Proof |

Historical background

In 1977, Australia's currency situation was defined by its recent transition to a managed float and the lingering effects of the breakdown of the Bretton Woods system. Since September 1974, the Australian dollar had been pegged to a trade-weighted basket of currencies, a system designed to provide more stability than a peg to the US dollar alone. However, this period was one of significant economic strain, with high inflation (around 13% in 1975) and unemployment, which placed consistent downward pressure on the currency. The Reserve Bank of Australia was actively intervening to manage the value within set boundaries, a challenging task amidst global oil shocks and domestic wage-price spirals.

The year itself was a transitional calm before a significant policy shift. The Australian dollar remained within a relatively narrow band against its trade-weighted index, but underlying pressures were building. The election of the Fraser government in late 1975 had ushered in a more market-oriented approach, and there was growing debate about moving to a more flexible exchange rate to better absorb external shocks. While the formal move to a float was still six years away (in 1983), 1977 represented a period where the limitations of the managed basket peg were becoming increasingly apparent to policymakers and economists.

Consequently, the currency landscape in 1977 was one of controlled vulnerability. The peg provided a nominal anchor but required substantial foreign exchange reserves to defend, and it often conflicted with domestic monetary policy goals. The experience of this period, marked by the difficulty of maintaining a fixed parity in a world of volatile capital flows and high inflation, was crucial in building the intellectual and practical case for the financial deregulation and the free float that would follow in the 1980s.

The year itself was a transitional calm before a significant policy shift. The Australian dollar remained within a relatively narrow band against its trade-weighted index, but underlying pressures were building. The election of the Fraser government in late 1975 had ushered in a more market-oriented approach, and there was growing debate about moving to a more flexible exchange rate to better absorb external shocks. While the formal move to a float was still six years away (in 1983), 1977 represented a period where the limitations of the managed basket peg were becoming increasingly apparent to policymakers and economists.

Consequently, the currency landscape in 1977 was one of controlled vulnerability. The peg provided a nominal anchor but required substantial foreign exchange reserves to defend, and it often conflicted with domestic monetary policy goals. The experience of this period, marked by the difficulty of maintaining a fixed parity in a world of volatile capital flows and high inflation, was crucial in building the intellectual and practical case for the financial deregulation and the free float that would follow in the 1980s.

Series: Royal Related 50 Cent Coins

🌱 Very Common