10 córdobas (Ibero-American Series) – Nicaragua

Add to wishlist

Non-circulating coins

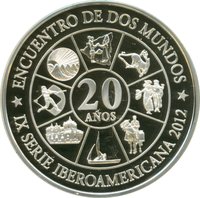

Commemoration: Ibero-American Series IX - 20th Anniversary

Series: Ibero-American

Nicaragua

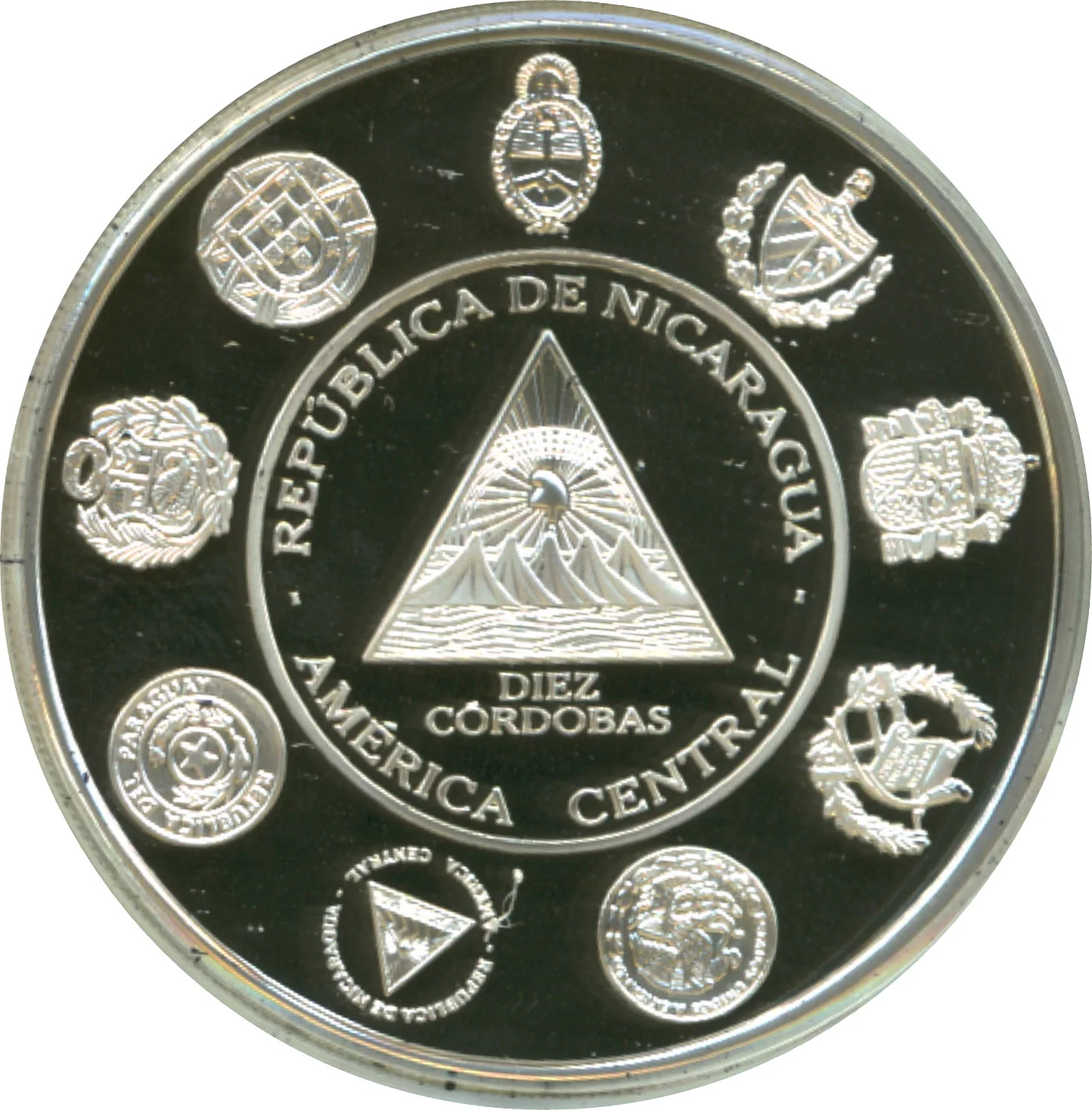

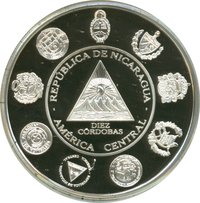

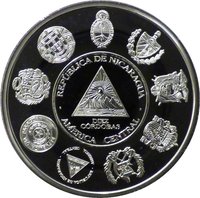

Obverse

Reverse

Edge

Reeded

Categories

| Transportation> Watercraft |

| Animal> Horse |

| Symbols> Coat of Arms |

| Currency> Coin depiction |

| Art> Dance |

| Building> Religious building |

| Geography> Mountain |

| Map |

| Sport> Baseball |

Mints

| Name | Mark |

|---|---|

| Royal Mint of Madrid | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2012 | — | 12,000 | Proof |

Historical background

In 2012, Nicaragua's currency situation was characterized by a managed dual-currency system with notable stability but underlying vulnerabilities. The country officially used both the Nicaraguan Córdoba (NIO) and the US Dollar, with the Córdoba being the legal tender for most daily transactions and formal accounting. The Central Bank of Nicaragua (BCN) maintained a crawling peg exchange rate regime, where the Córdoba was allowed to depreciate against the US dollar at a slow, pre-announced rate of approximately 5% per year. This policy, in place since 1991, aimed to provide predictability for trade and investment while controlling inflationary pressures.

The economy was heavily dollarized, with an estimated 70% of bank deposits and a significant portion of loans denominated in US dollars. This dollarization was a legacy of past hyperinflation and political instability, creating a persistent reliance on the US currency for savings and major transactions. While the crawling peg provided short-term stability, it required consistent foreign exchange reserves to defend, and the high level of dollarization posed a systemic risk. If the Córdoba were to devalue rapidly, borrowers with dollar-denominated loans but Córdoba income could face severe repayment difficulties, potentially triggering a banking crisis.

Overall, the system in 2012 was stable on the surface, supported by prudent fiscal management under the Ortega administration and continued remittance inflows. Inflation was relatively low, and the exchange rate corridor was maintained without major shocks. However, economists highlighted the structural fragility of the high dollarization and the economy's dependence on external factors like commodity prices, remittances, and foreign aid—particularly from Venezuela under the Petrocaribe agreement. This reliance meant that while the currency regime was orderly, Nicaragua's monetary stability remained exposed to external economic and political shifts.

The economy was heavily dollarized, with an estimated 70% of bank deposits and a significant portion of loans denominated in US dollars. This dollarization was a legacy of past hyperinflation and political instability, creating a persistent reliance on the US currency for savings and major transactions. While the crawling peg provided short-term stability, it required consistent foreign exchange reserves to defend, and the high level of dollarization posed a systemic risk. If the Córdoba were to devalue rapidly, borrowers with dollar-denominated loans but Córdoba income could face severe repayment difficulties, potentially triggering a banking crisis.

Overall, the system in 2012 was stable on the surface, supported by prudent fiscal management under the Ortega administration and continued remittance inflows. Inflation was relatively low, and the exchange rate corridor was maintained without major shocks. However, economists highlighted the structural fragility of the high dollarization and the economy's dependence on external factors like commodity prices, remittances, and foreign aid—particularly from Venezuela under the Petrocaribe agreement. This reliance meant that while the currency regime was orderly, Nicaragua's monetary stability remained exposed to external economic and political shifts.

Series: Ibero-American

✨ Legendary