1000 bolivars – Venezuela

Add to wishlist

Venezuela

Context

Year: 2005

Issuer: Venezuela

Period:

(since 1999)

Currency:

(1879—2007)

Demonetization: 31 December 2011

Total mintage: 9,000,000

Material

References

Y: #

Numista: #5482

Value

Exchange value: 1000 VEB

Obverse

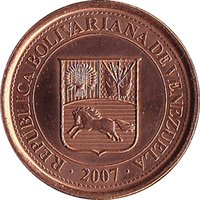

Reverse

Description:

Bust left, engraver's name below. Legend on outer rim.

Inscription:

• BOLÍVAR • LIBERTADOR

BARRE

BARRE

Translation:

Bolívar, Liberator. Barre

Script: Latin

Language: Spanish

Engraver: Désiré-Albert Barre

Categories

| Animal> Horse |

| Symbols> Coat of Arms |

| Person> Military leader |

| Person> Politician |

Mints

| Name | Mark |

|---|---|

| Casa de la Moneda de Venezuela | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2005 | — | 9,000,000 |

Historical background

In 2005, Venezuela's currency situation was characterized by relative stability and strong government control, a marked contrast to the severe hyperinflation and economic collapse that would follow in subsequent decades. The national currency, the bolívar, was officially pegged to the US dollar under a fixed exchange rate regime established by the government of President Hugo Chávez. The primary rate was 2,150 bolívares to the dollar, administered by the newly created CADIVI (Commission for the Administration of Currency Exchange), which required strict approval for citizens and businesses to access foreign currency for imports, travel, or debt payments.

This system was underpinned by a period of high global oil prices, with crude averaging around $50 per barrel that year. As a petrostate, Venezuela enjoyed substantial foreign currency inflows, which allowed the government to maintain the peg, finance expansive social programs (the "Misiones"), and heavily subsidize imports of food and consumer goods. The economy grew by a robust 10.3% in 2005, masking underlying structural weaknesses such as declining domestic production, rising inflation (officially 15.3%, though likely higher), and a growing reliance on imports funded by oil revenue.

However, the rigid exchange controls of 2005 sowed the seeds for future dysfunction. By creating a vast disparity between the strong official rate and a nascent black-market rate, a lucrative parallel currency market began to flourish. This incentivized corruption and capital flight, as those with access to cheap dollars could profit immensely. While the system appeared manageable during an oil boom, it created critical vulnerabilities, leaving the economy dangerously exposed to any future fall in oil revenue or increase in fiscal spending, setting the stage for the profound monetary crises that would erupt after Chávez's death in 2013.

This system was underpinned by a period of high global oil prices, with crude averaging around $50 per barrel that year. As a petrostate, Venezuela enjoyed substantial foreign currency inflows, which allowed the government to maintain the peg, finance expansive social programs (the "Misiones"), and heavily subsidize imports of food and consumer goods. The economy grew by a robust 10.3% in 2005, masking underlying structural weaknesses such as declining domestic production, rising inflation (officially 15.3%, though likely higher), and a growing reliance on imports funded by oil revenue.

However, the rigid exchange controls of 2005 sowed the seeds for future dysfunction. By creating a vast disparity between the strong official rate and a nascent black-market rate, a lucrative parallel currency market began to flourish. This incentivized corruption and capital flight, as those with access to cheap dollars could profit immensely. While the system appeared manageable during an oil boom, it created critical vulnerabilities, leaving the economy dangerously exposed to any future fall in oil revenue or increase in fiscal spending, setting the stage for the profound monetary crises that would erupt after Chávez's death in 2013.

🌱 Common