25 centésimos – Uruguay

Add to wishlist

Uruguay

Context

Year: 1960

Issuer: Uruguay

Issuing organization: Bank of Oriental Republic of Uruguay

Period:

(since 1825)

Currency:

(1863—1975)

Demonetized: Yes

Total mintage: 48,000,000

Material

Diameter: 17.9 mm

Weight: 3 g

Thickness: 1.64 mm

Shape: Round

Composition: Copper-nickel

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #

Numista: #5287

Value

Exchange value: 0.25 UYP

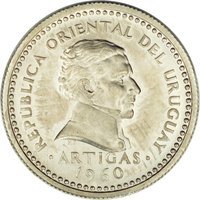

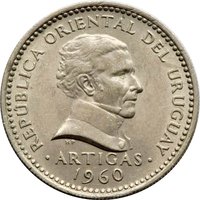

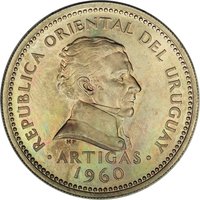

Obverse

Description:

Portrait of José Artigas facing right inside a beaded rim.

Inscription:

REPÚBLICA ORIENTAL DEL URUGUAY

HP

·ARTIGAS·

1960

HP

·ARTIGAS·

1960

Translation:

ORIENTAL REPUBLIC OF URUGUAY

HP

·ARTIGAS·

1960

HP

·ARTIGAS·

1960

Script: Latin

Language: Spanish

Engraver: Thomas Humphrey Paget

Reverse

Edge

Reeded

Categories

| Symbol> Sun |

| Person> Military leader |

| Person> Politician |

| Symbols> Coat of Arms |

| Symbol> Wreath |

Mints

| Name | Mark |

|---|---|

| Royal Mint (Tower Hill) | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1960 | — | 48,000,000 | ||

| 1960 | — | — | Proof |

Historical background

In 1960, Uruguay's currency situation was characterized by a complex and strained system of exchange controls and multiple exchange rates, a legacy of persistent economic challenges. The country was still grappling with the long-term decline of its traditional agricultural export model, which had been the foundation of its early 20th-century prosperity. To manage chronic balance of payments deficits and shield domestic industry, the government maintained a heavily regulated financial environment through the Banco de la República Oriental del Uruguay (BROU). The official peso rate was fixed, but a system of "financial" or "free" exchange rates existed alongside it, creating a significant gap that encouraged a black market for dollars.

This multi-tiered system was inherently unstable and distortionary. Essential imports and traditional exports like beef and wool were handled at a preferential official rate, while most other transactions fell under a less favorable financial rate. The disparity between these rates created inefficiencies, discouraged certain exports, and led to frequent speculative pressures. Furthermore, high inflation—a recurring issue—eroded the peso's real value, putting downward pressure on the fixed official parity and widening the gap with the free market rate.

Overall, the currency regime of 1960 reflected a defensive and interventionist economic policy aimed at controlling scarce foreign reserves and protecting the welfare state. While it provided short-term stability for certain sectors, it masked deeper structural problems, including fiscal deficits and industrial stagnation. This cumbersome system would prove increasingly difficult to sustain, foreshadowing the more severe monetary crises, devaluations, and eventual liberalization efforts that would mark the coming decades in Uruguay.

This multi-tiered system was inherently unstable and distortionary. Essential imports and traditional exports like beef and wool were handled at a preferential official rate, while most other transactions fell under a less favorable financial rate. The disparity between these rates created inefficiencies, discouraged certain exports, and led to frequent speculative pressures. Furthermore, high inflation—a recurring issue—eroded the peso's real value, putting downward pressure on the fixed official parity and widening the gap with the free market rate.

Overall, the currency regime of 1960 reflected a defensive and interventionist economic policy aimed at controlling scarce foreign reserves and protecting the welfare state. While it provided short-term stability for certain sectors, it masked deeper structural problems, including fiscal deficits and industrial stagnation. This cumbersome system would prove increasingly difficult to sustain, foreshadowing the more severe monetary crises, devaluations, and eventual liberalization efforts that would mark the coming decades in Uruguay.

Series: 1960 Uruguay circulation coins

🌱 Very Common