50 Centimes – Belgium

Belgium

Context

Material

References

KM: #Click to copy to clipboard87

Numista: #510

Value

Exchange value: 0.50 BEF

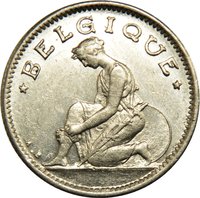

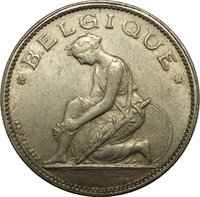

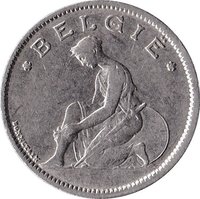

Obverse

Description:

Kneeling woman with French legend above, designer initials at left.

Inscription:

* BELGIQUE *

A.B

A.B

Translation:

BELGIUM

A.B

A.B

Script: Latin

Language: French

Engraver: Armand Bonnetain

Reverse

Description:

Caduceus divides value.

French text above, year below.

French text above, year below.

Inscription:

* BON POUR *

50 CES

* 1923 *

50 CES

* 1923 *

Translation:

Good for

50 Centimes

1923

50 Centimes

1923

Script: Latin

Language: French

Engraver: Armand Bonnetain

Edge

Reeded

Mints

| Name | Mark |

|---|---|

| Royal Mint of Belgium | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1922 | — | 6,180,000 | ||

| 1923 | — | 8,820,000 | ||

| 1927 | — | 7,000,000 | ||

| 1928 | — | 3,000,000 | ||

| 1929 | — | 1,000,000 | ||

| 1930 | — | 1,000,000 | ||

| 1932 | — | — | ||

| 1933 | — | 2,861,000 |

Historical background

In 1922, Belgium was grappling with the severe economic and monetary consequences of the First World War. The German occupation had financed itself by printing Belgian francs, leading to a massive expansion of the money supply and a collapse in the currency's value. By the war's end, the franc had lost over 80% of its pre-war purchasing power, and the government, burdened by reconstruction costs and debt, continued to run large deficits, further fueling inflation and undermining confidence.

The situation was a direct contest between two monetary philosophies. The Banque Nationale de Belgique, under Governor Fernand Hautain, advocated for a deflationary policy to restore the franc's pre-war gold parity, believing this was essential for national prestige and long-term stability. This "franc fort" policy, however, meant maintaining high interest rates and tight credit, which stifled economic growth and increased the real burden of public and private debt. Opposing this were industrialists and many politicians who pushed for devaluation or stabilization at a lower level to ease the pressure on exporters and debtors and to stimulate recovery.

Ultimately, 1922 proved to be a pivotal but unresolved year in this struggle. The government of Prime Minister Georges Theunis, while fiscally conservative, hesitated to impose the full austerity required for a return to pre-war parity. The franc remained unstable on foreign exchange markets, and social unrest grew due to the high cost of living. This period of uncertainty would persist until the mid-1920s, when a combination of foreign loans (notably from the United States) and a final, decisive devaluation in 1926 led to the stabilization of the Belgian franc at one-seventh of its pre-war gold value.

The situation was a direct contest between two monetary philosophies. The Banque Nationale de Belgique, under Governor Fernand Hautain, advocated for a deflationary policy to restore the franc's pre-war gold parity, believing this was essential for national prestige and long-term stability. This "franc fort" policy, however, meant maintaining high interest rates and tight credit, which stifled economic growth and increased the real burden of public and private debt. Opposing this were industrialists and many politicians who pushed for devaluation or stabilization at a lower level to ease the pressure on exporters and debtors and to stimulate recovery.

Ultimately, 1922 proved to be a pivotal but unresolved year in this struggle. The government of Prime Minister Georges Theunis, while fiscally conservative, hesitated to impose the full austerity required for a return to pre-war parity. The franc remained unstable on foreign exchange markets, and social unrest grew due to the high cost of living. This period of uncertainty would persist until the mid-1920s, when a combination of foreign loans (notably from the United States) and a final, decisive devaluation in 1926 led to the stabilization of the Belgian franc at one-seventh of its pre-war gold value.

🌱 Very Common