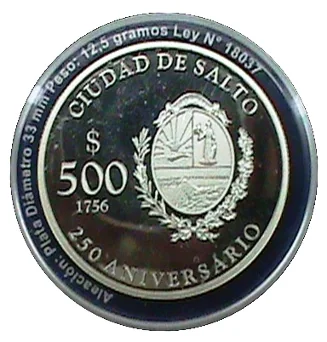

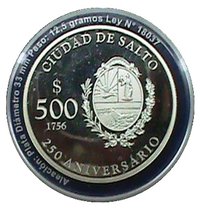

500 Pesos Uruguayos (Salto City) – Uruguay

Circulating commemorative coins

Commemoration: 250th Anniversary of Salto City

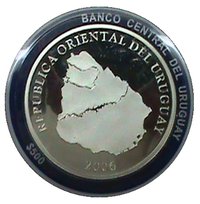

Uruguay

Context

Year: 2006

Issuer: Uruguay

Issuing organization: Central Bank of Uruguay

Period:

(since 1825)

Currency:

(since 1993)

Demonetization: 1 September 2019

Total mintage: 10,000

Material

References

KM: #Click to copy to clipboard133

Numista: #48097

Value

Exchange value: 500 UYU

Bullion value: $31.54

Obverse

Reverse

Edge

Reeded

Categories

| Map |

| Symbols> Coat of Arms |

| Symbol> Wreath |

Mints

| Name | Mark |

|---|---|

| Royal Dutch Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2006 | — | 10,000 | Proof |

Historical background

In 2006, Uruguay's currency situation was characterized by a managed float regime and a continued, though diminished, reliance on the US dollar. The Uruguayan peso (UYU) had been allowed to float freely since a major financial crisis in 2002, but the Central Bank of Uruguay (BCU) actively intervened in the foreign exchange market to mitigate excessive volatility and prevent a sharp appreciation that could harm export competitiveness. This period saw a general trend of peso appreciation against the US dollar, driven by strong capital inflows, a robust economic recovery, and high global prices for the country's key exports like beef, soy, and dairy.

This appreciation presented a policy dilemma. While it helped to keep inflation in check—a persistent historical challenge—by making imports cheaper, it also threatened the profitability of the export and import-competing sectors. The BCU's interventions, which included purchasing dollars to build international reserves, aimed to strike a balance. These reserves were crucial for bolstering economic stability and confidence, given the traumatic memory of the 2002 bank run and debt default. Furthermore, Uruguay's economy remained partially dollarized, with a significant portion of bank deposits and loans still denominated in US dollars, creating an ongoing vulnerability to exchange rate swings.

Overall, 2006 represented a year of consolidation and cautious management within Uruguay's post-crisis monetary framework. The economy was growing strongly, but authorities were carefully navigating the trade-offs between controlling inflation, maintaining export growth, and continuing the process of de-dollarization. The currency policy was fundamentally geared towards ensuring stability, rebuilding trust in the peso, and accumulating a buffer of foreign reserves to guard against future external shocks.

This appreciation presented a policy dilemma. While it helped to keep inflation in check—a persistent historical challenge—by making imports cheaper, it also threatened the profitability of the export and import-competing sectors. The BCU's interventions, which included purchasing dollars to build international reserves, aimed to strike a balance. These reserves were crucial for bolstering economic stability and confidence, given the traumatic memory of the 2002 bank run and debt default. Furthermore, Uruguay's economy remained partially dollarized, with a significant portion of bank deposits and loans still denominated in US dollars, creating an ongoing vulnerability to exchange rate swings.

Overall, 2006 represented a year of consolidation and cautious management within Uruguay's post-crisis monetary framework. The economy was growing strongly, but authorities were carefully navigating the trade-offs between controlling inflation, maintaining export growth, and continuing the process of de-dollarization. The currency policy was fundamentally geared towards ensuring stability, rebuilding trust in the peso, and accumulating a buffer of foreign reserves to guard against future external shocks.

💎 Very Rare