1 dollar – Canada

Add to wishlist

Circulating commemorative coins

Commemoration: Visit of His Majesty King George VI and future Majesty Queen Elizabeth II to Ottawa

Canada

Context

Material

References

KM: #

Numista: #450

Value

Exchange value: 1 CAD

Bullion value: $46.10

Inflation-adjusted value: 21.00 CAD

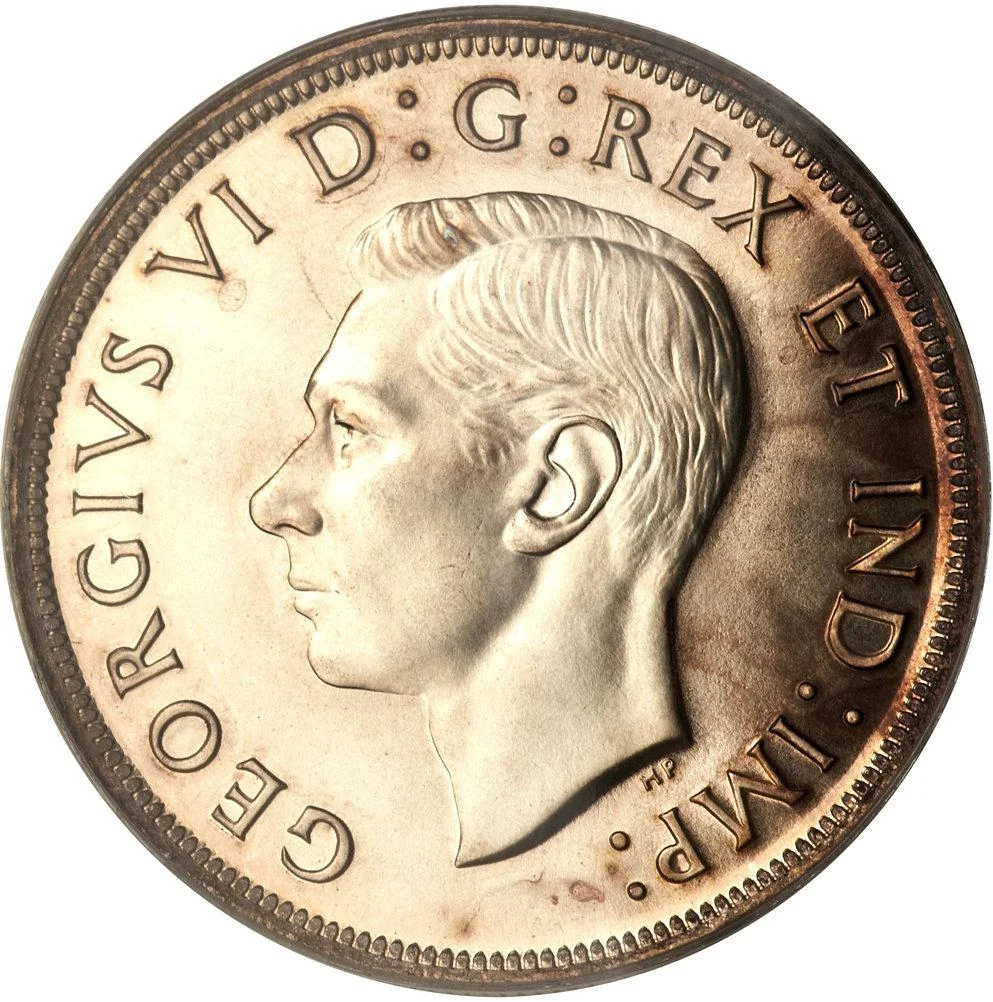

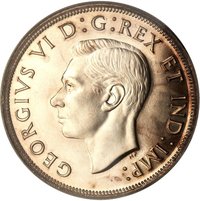

Obverse

Description:

King George VI left-facing portrait.

Inscription:

GEORGIVS VI D:G:REX ET IND:IMP

HP

HP

Translation:

George VI by the Grace of God, King and Emperor of India.

Script: Latin

Language: Latin

Engraver: Thomas Humphrey Paget

Reverse

Description:

The Canadian Parliament Buildings feature the Latin inscription "FIDE SVORVM REGNAT" ("he reigns by the faith of his people"), "CANADA," and the face value.

Inscription:

FIDE SVORVM REGNAT

CANADA

1939

1 DOLLAR

CANADA

1939

1 DOLLAR

Translation:

He reigns by the faith of his own

CANADA

1939

1 DOLLAR

CANADA

1939

1 DOLLAR

Script: Latin

Language: Latin

Engraver: Emanuel Otto Hahn

Edge

Milled

Categories

| Building> Governmental building |

Mints

| Name | Mark |

|---|---|

| Royal Canadian Mint of Ottawa | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1939 | — | 1,363,816 | ||

| 1939 | — | — | Proof |

Historical background

In 1939, Canada entered the Second World War with a monetary system still deeply shaped by the Great Depression. The country was on a de facto sterling exchange standard, with the Canadian dollar's value loosely pegged to both the British pound and the U.S. dollar, though its primary anchor had shifted towards the U.S. currency. This informal arrangement provided some stability but left the currency vulnerable to speculative flows and the economic policies of its larger trading partners. The Bank of Canada, established just four years earlier in 1935, held limited gold reserves and had not yet fully asserted its modern role as the central monetary authority.

The outbreak of war triggered an immediate financial crisis, as capital flight and a rush for U.S. dollars threatened Canada's exchange reserves. In response, the government swiftly implemented the Foreign Exchange Control Order on September 15, 1939, establishing a fixed exchange rate of $1.10 Canadian to $1.00 U.S. This created a controlled, "pegged" currency regime administered by a new agency, the Foreign Exchange Control Board (FECB). All foreign exchange transactions were now centralized, requiring approval to prevent capital flight, conserve U.S. dollars for vital war purchases, and ensure financial stability for the war effort.

This wartime control system marked a decisive shift from a relatively free-floating currency to a state-managed instrument of national policy. The FECB’s strict regulations effectively insulated the Canadian dollar from market pressures, allowing the government to direct resources and manage debt for wartime financing. This framework would define Canada's currency situation for the duration of the conflict, laying the groundwork for the more formal Bretton Woods system that would emerge in the post-war era.

The outbreak of war triggered an immediate financial crisis, as capital flight and a rush for U.S. dollars threatened Canada's exchange reserves. In response, the government swiftly implemented the Foreign Exchange Control Order on September 15, 1939, establishing a fixed exchange rate of $1.10 Canadian to $1.00 U.S. This created a controlled, "pegged" currency regime administered by a new agency, the Foreign Exchange Control Board (FECB). All foreign exchange transactions were now centralized, requiring approval to prevent capital flight, conserve U.S. dollars for vital war purchases, and ensure financial stability for the war effort.

This wartime control system marked a decisive shift from a relatively free-floating currency to a state-managed instrument of national policy. The FECB’s strict regulations effectively insulated the Canadian dollar from market pressures, allowing the government to direct resources and manage debt for wartime financing. This framework would define Canada's currency situation for the duration of the conflict, laying the groundwork for the more formal Bretton Woods system that would emerge in the post-war era.

🌱 Common